Assets to be acquired are still unclear, but deal could expand Ceva’s North American and Asian presence.

Ceva is acquiring the freight management business of France’s CMA CGM, potentially giving the Swiss firm a larger toehold in the U.S. and Asia freight markets.

The deal between the fifth largest contract logistics firm and the fourth largest containership owner by tonnage aims to thwart an unsolicited bid for Ceva (SIX: CEVA.Z.EB) from Denmark’s DSV (Nasdaq OMX: DSV.C.IX).

As part of the transaction for the logistics, CMA CGM issued a new tender offer to shareholders of Ceva, offering to buy the roughly 75% it does not already own at a price of 30 Swiss Franc ($30.05 US dollars), a 9% premium to the company’s share price as of its May initial public offering and the same as DSV’s offer price.

The potential tie-up with CMA CGM come as ocean carriers seek to provide end-to-end logistics services, rather than being merely a capacity provider. Maersk (Nasdaq OMX: MAERB) is taking a similar tack after its September announcement that it will be folding its Damco logistics business into it ocean freight unit.

CMA CGM chief executive Rodolphe Saade said last month the early stake in Ceva was “an important step in our strategy to complement our transport offering with logistics services.”

CMA CGM’s logistics business provides air, ocean and intermodal transportation services. A Ceva representative says the acquisition “will provide added scale in volumes, particularly for ocean freight.”

Terms of the acquisition were not yet agreed upon. according to the press release.

CMA CGM Logistics saw revenue of $650 million last year, accounting for 3% of CMA CGM’s total revenue. Operating margin for the logistics business are between 3% and 4%, similar to Ceva’s. released few details around the acquisition except that it would include personnel and warehouses.

CMA CGM logistics’ operating subsidiaries include California-based USL Cargo Services, which CMA CGM acquired in 2007. USL operates 174 warehouses across North America, chiefly leased from third parties. USL also operates 3.1 million square feet of warehouses across China and another 900,000 in other parts of Asia. It also has air facilities in China.

CMA CGM logistics also co-owns LCL Logistix, one of the top freight consolidators in India, handling some 100,000 twenty foot equivalent units (teu) in containers during 2015. Its other major operating subsidiary is ANL Container Line, which provides shipping services for the Australian market.

It was not immediately clear whether Ceva’s deal the acquisition would also include these subsidiaries. More details are expected to be release at Ceva’s mid-November earnings conference call.

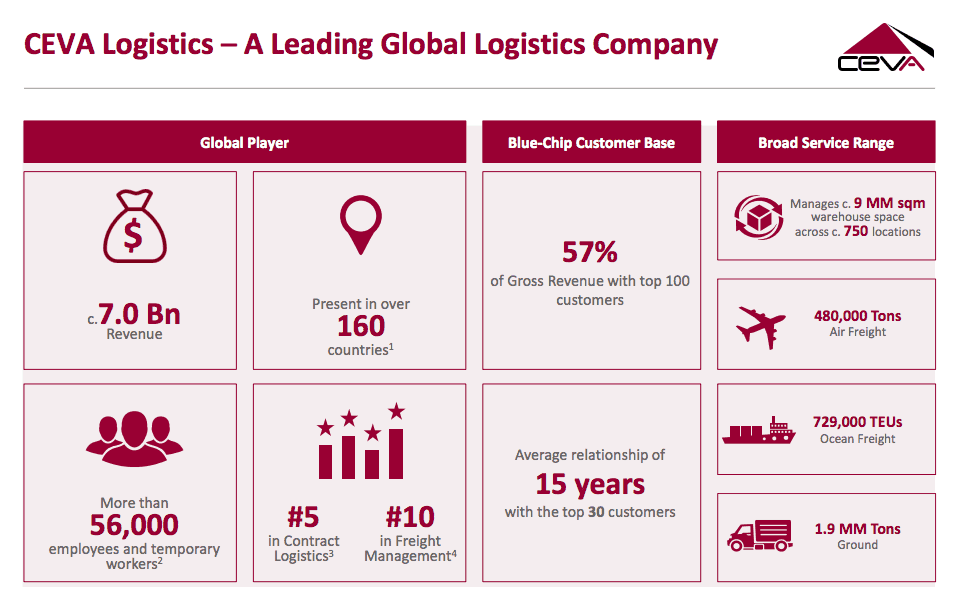

Ceva itself manages 96 million square feet of warehouse space and handles 729,000 teus of containers, 1.9 million tons of ground freight and 480,000 tons of air freight.

It saw 10% revenue growth in the first half of 2018, rising to $3.64 billion with operating profit of $119 million up 14% from a year ago.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now