Commentary

The Chainalytics-Cowen Monthly Freight Indices came out yesterday reporting a softening of the freight markets in the month of April stating, “Freight Indices remain elevated year over year, but have softened considerably.” The problem with this is the information is not incredibly viable on June 18th, as markets have changed considerably since the end of April where the report ends. The market is in a completely different place in mid-June with spot rates expanding.

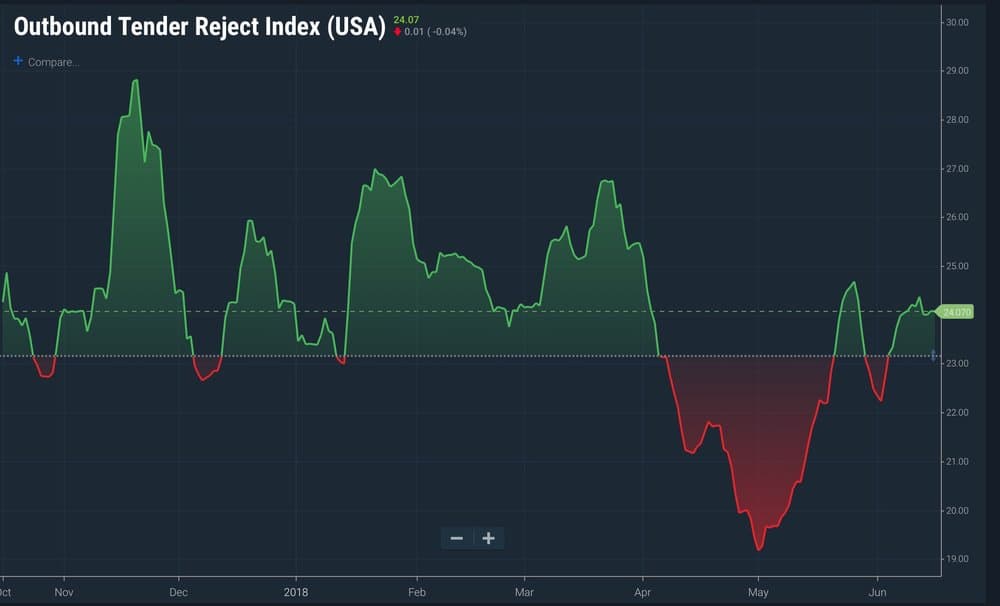

FreightWaves national Tender Reject Index (TRI) showed a similar market “cooling” as the Chainalytics-Cowen indices are reporting, moving from load rejections of 26.43% in late March to 19.15% by the end of April, a 27.5% decrease in rejections.

But, since early May the market has seen a return to a more volatile form with rejections around 24%, indicating the potential in the spot market to haul freight at a higher rate.

As a former pricing manager and financial analyst for a trucking company, I used to get excited about any general market data I could get that helped me figure out our place in the broader market. I quickly figured out in 2017 it really didn’t do me any good to find out in late July the market had suffered capacity constraints, and we had missed our chance to adjust our operation and pricing to take advantage and lessen our exposure to potential increased costs.

In the past, when freight markets and patterns were more stable, looking at data that was a month and a half old was not necessarily a bad thing. General market data was useful in the way that it helped you understand your place in the big picture. The data allowed shippers and carriers to evaluate their operating strategies and make effective adjustments, as the market did not have the volatility we are seeing today. Shippers and carriers could rely on predictable seasonal patterns dominating with intermediate, short-lived disruptions. The stability meant there wasn’t a strong need for broader visibility.

The trucking industry is one of the most fragmented in business with the largest carriers owning no more than 3% of the overall market. Most companies’ financial departments, regardless of industry, judge themselves against themselves in the form of year over year comparisons. This internal comparison works better in industries with lower fragmentation, but in trucking it is a very limited view.

The fragmentation in transportation means most companies in the industry are operating blindly, and only have small pieces of information to gain a general understanding how they are operating in relation to the broader market. In my example above, I wanted to know if our company outperforming the market or were we special. I found out we were not that special and may have missed an opportunity due to our limited view.

Aside from the extreme fragmentation keeping all the participants in the freight markets in the dark, many transportation companies and shipping departments utilize price/revenue reporting as their primary item for evaluation. The reason for pricing/revenue derivatives is that it is one of the easiest pieces of information to understand. Most shippers (transportation departments), trucking companies, and brokerage houses understand what $2.50 per mile or $2,000 flat rate means in the Atlanta to Chicago lane. Most would agree this is a relatively high rate. The understanding of prices is very relatable to almost all divisions of the company. The problem with pricing/revenue information is that it is very lagged and is a poor tool for real time market reporting.

DAT, commonly viewed as the benchmark of spot data because of the relevance to current market conditions and not a super-trailing trailing indicator, showed some softness in April and early May, that has since showed significant recovery. Chainalytics’ data is sourced through shipper info and does not have the same regular cadence as DAT’s spot data.

According to Don Thornton, SVP of Sales and Marketing at DAT, their index showed significant changes in the market over the past few weeks, with price appreciation across the market, with the Southeast and Midwest seeing the highest change. This is all good news for carriers going into the heavier shipping season on the backhalf of the year.

In the past month, FreightWaves has reported multiple disruptions in the Los Angeles, Dallas, and now Atlanta markets as capacity tightness ripples across the country. These reports are based on near-real time data that is based on the previous day’s electronic tendering activity. The reason we created the TRI is to find a way to bypass lags in revenue cycles and date recognition issues and get to a more activity-based metric. The TRI is not slowed by pricing or revenue reporting cycles.

Just like many metrics, the TRI does not necessarily stand alone and not all price reporting tools are created equal. DAT is far more up to date in terms of price reporting as it relates to the current market. We notice they tend to corroborate our market signals with their rate reporting. An example of this is they are currently reporting national spot rates on the rise, moving from $1.82 per mile in May to $1.96 in the past week, while turndowns moved from 19% to 24% during the same period. One can not determine everthing from either number (i.e. a rate is great for understanding where the market has been, but doesn’t give a directional signal; and TRI gives a directional signal, but doesn’t give a rate to quote off of).

Pricing and revenue data is invaluable when evaluating the market and cannot be replaced entirely, but they require time to refine and report making them a poor tool for measuring current market conditions by themselves. A month and a half old data may have worked 3 years ago, but today’s volatile market needs faster measures.

Stay up-to-date with the latest commentary and insights on FreightTech and the impact to the markets by subscribing.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now