National freight volumes recovered from their Easter slump this week with the Outbound Tender Volume Index averaging 4% higher this week versus last. Even more interesting, volumes are averaging on par with May volumes year-over-year. By contrast, however, shorter haul (0-99 miles) volumes are up approximately 12.8% versus the same week last year. According to FreightWaves proprietary tender volume data, indicating load volumes are flat but with less miles.

Less miles can mean lower utilization for carriers as more time is spent loading or unloading versus driving, where most of the money is made due to the fact most trucking rates are on a per mile basis. There are truckload minimums and detention charges to try and mitigate some of the cost of operating a heavy vehicle that is not moving much, but they are not generally successful at lowering trucking operation ratios, unless the mileage is very short and times at the dock are very low.

Wait times are trending higher, averaging almost 9% higher in the first four months of 2019 versus the same period last year according to FreightWaves Wait Time Index based on aggregated ELD data. The trend does appear to be softening over the last few months, but averages are just over the two-hour mark at 146 minutes of average wait time for getting loaded or unloaded on a dock.

With freight patterns remaining relatively consistent over the past few months, capacity continues to be relatively loose. The Outbound Tender Rejection Index stopped declining this week and have ticked up 9 basis points (bps) the last two days of April. This is not expected to be a big trend reversing pivot as much as it is a typical end of the month pattern.

Last year tender rejection rates began to increase in earnest in the second week of May leading up to Memorial Day. There is a chance this could be the start of the late spring shift in capacity that is typical, but so far the increase in rejection rates is still too small to call.

Another sign that is significant but too short-lived to call a trend is the volumes surging out of the Atlanta market, the nation’s second largest single outbound market with 4.3% of the total U.S. outbound volume. It should be noted that volumes were this high in March, so it is still too soon to call it a full comeback. At the same time, a 17% increase in weekly volume is nothing to sneeze at, especially in a top three market not located east of the Mississippi. Capacity remains loose in the region regardless of the surge.

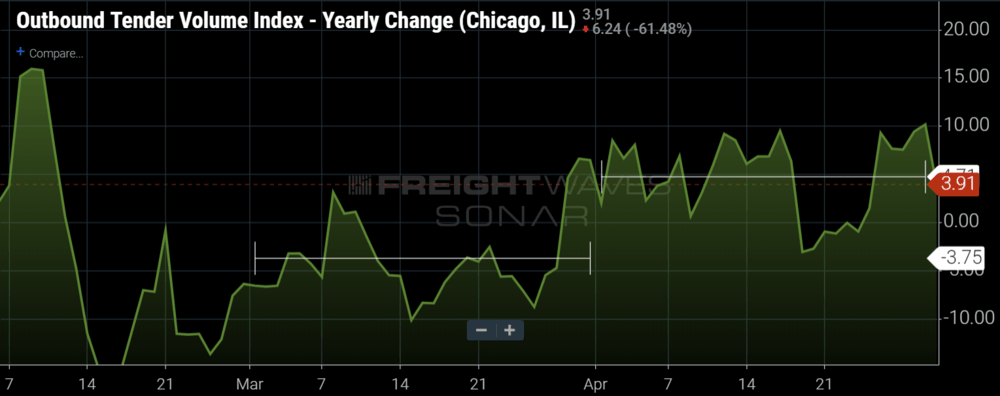

Any surging volume on the east coast is worthy of attention due to the amount of activity that continues to be present out West. Volumes are still averaging much higher from a year-over-year perspective in the larger western markets of L.A. and Seattle, but are starting to show longer term trends towards more seasonal levels. Meanwhile, the Chicago market — pivotal freight market in the U.S. — is showing signs of strengthening after having a very soft March. April volumes were up over 4% over 2018 levels in April versus averaging 3.75% under 2018 volumes in March.