Chalk up yet another record for ocean shipping. More vessels traded hands in the first half of this year than in any other six-month stretch — yet another industry signal that’s flashing green.

It’s not just container ships. An exceptionally high number of tankers and bulkers were sold as well. Values of ship assets have continued to rise across the board, not only in container and dry cargo shipping, where freight rates are very strong, but also, incongruously, in tanker shipping, where freight rates are abysmal.

The higher ship prices go, the higher the shipowner’s net asset value (NAV, the market-adjusted value of the fleet and other assets, minus liabilities). The higher NAV goes, the higher stock prices should theoretically go.

According to Steve Gordon, managing director of Clarksons Research, “The stellar S&P [sale and purchase] market achieved ‘top marks,’ with all-time record transactions of more than 85 million DWT [deadweight tons], up 131% on H1 2020 and 31% on H2 2020, and more than double the long-term trend.

“At this run rate, around 8% of the fleet will change ownership in 2021,” said Gordon.

Stifel analyst Ben Nolan cited “a frenzy of activity,” explaining that the “real surge” in investment is in S&P deals more so than newbuild orders. “Typically, about 1,200 large oceangoing ships are bought and sold annually, but we have already reached that level in 2021,” said Nolan.

Container sector

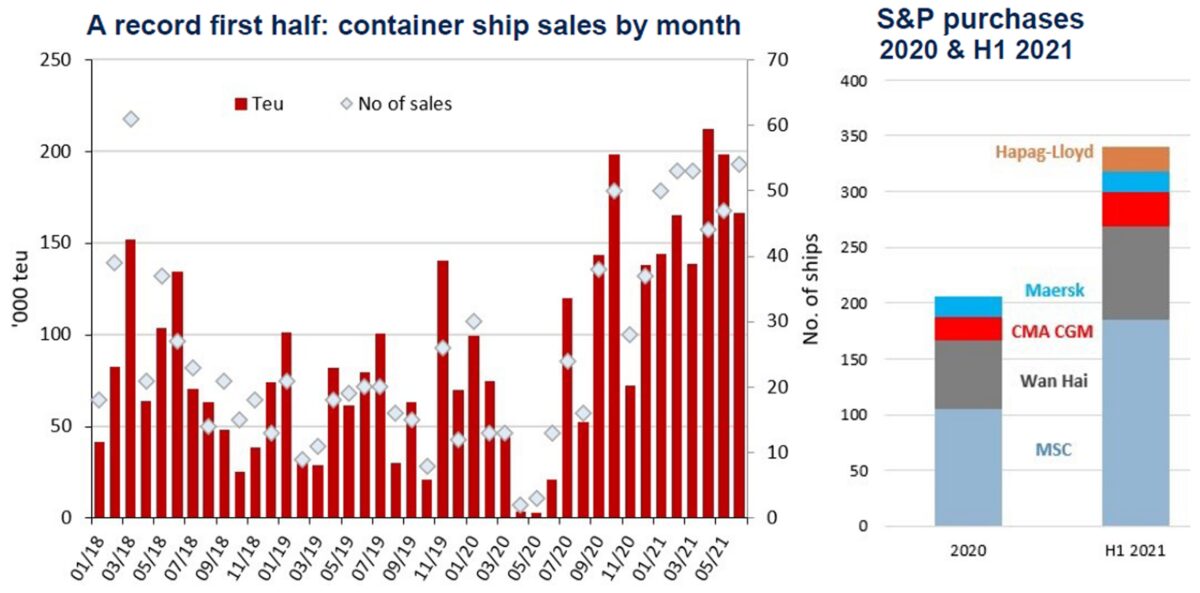

According to Alphaliner, 301 container ships with aggregate capacity of 1,025,000 twenty-foot equivalent units (TEUs) traded hands in January-June. “The volume represents the largest TEU amount ever bought and sold in a six-month period,” it said.

Mediterranean Shipping Co. (MSC) led the charge, buying 53 ships totaling 185,590 TEUs in the first half. It has bought 72 ships totaling 289,950 TEUs since last August — “a buying binge that is unprecedented in history,” said Alphaliner.

The more exposed liners are to skyrocketing freight rates, the higher their profits will be. Carriers can increase near-term exposure in two ways: by chartering in ships or buying them secondhand.

Alphaliner noted that chartering activity has now slowed due to a lack of available tonnage. The shortage “could be here to stay, changing the face of the charter market.” Non-operating owners (NOOs) — companies that charter ships to liners — have been placing their vessels on multiyear charters, “meaning that a significant portion of the NOO fleet will not be available again in the charter market for years to come,” said Alphaliner.

Fewer charterable ships means carriers must buy vessels secondhand to increase near-term exposure to freight rates. At the same time, NOOs that have already chartered out their existing fleet are looking to buy more vessels so they can charter them to liners.

This dynamic should add even more fuel to the fire in the S&P market. Container-ship values “have been skyrocketing from April onwards,” said Alphaliner, noting that a 1,700-TEU ship was sold in June for $21.5 million, triple what this size of ship fetched in January.

According to Gordon, the Clarksons index that tracks secondhand container ship values surged 124% during the first half of the year.

Tanker sector

Frenetic S&P activity and soaring asset values make perfect sense in container shipping, given stratospheric freight rates. But why would sales and values be rising in the tanker sector, where rates, as Nolan put it, are “apocalypse-level bad”?

Allied Shipbroking reported that 278 tankers totaling 33.2 million DWT traded hands in the first half. Last year’s numbers were skewed low by COVID lockdowns. Looking to the more normal year of 2019, this year’s first-half tanker sales were double H1 2019’s in terms of DWT.

When freight markets collapse, as they did after the financial crisis, ships are divested amid declining asset values by distressed sellers needing to raise cash and stay afloat. That’s not what’s happening in the current tanker-rate depression. Tanker values are increasing even though almost all tankers in service are bleeding cash.

Clarksons’ secondhand tanker value index is up 12% since the beginning of the year. Tanker executives speaking at the recent Marine Money Week virtual event said that depending on the type of tanker, values are up as much as 25% from lows in late 2020.

“The disconnect between asset values and charter rates — I don’t think I’ve ever seen anything like this before, where rates have been so low for so long and rates have hung in there,” said Ridgebury Tankers CEO Bob Burke during the Marine Money Week event.

Burke attributed the disconnect to several factors. “One is that balance sheets have staying power from the party last year [when tanker rates were extremely high] so people are able to hold the line. Another is that this is not like past cycles where there’s a huge orderbook that has to be worked through. This time, we see an end point in the not-too-distant future when charter rates will go back up.” In other words, there’s no rush to be a seller, so those who sell only do so at a high price relative to current freight rates.

Christian Walgrave, director of research and commercial performance at Teekay Tankers (NYSE: TNK), told Marine Money Week attendees that tanker values are being buoyed by outside factors. “Newbuild prices have gone up because of the increasing price of steel and container ships soaking up yard capacity. That’s putting [upward] pressure on the modern end of the [secondhand] spectrum.”

Older tanker values are also being supported by higher steel prices. “Scrap prices are at a 10-year high,” said Walgrave. He also pointed to buyer demand for older ships deployed in “sanctioned trades.” Owners willing to risk carrying Venezuelan and Iranian oil receive premium rates, justifying higher values for older tonnage that would otherwise be scrapped.

Dry bulk sector

According to Allied Shipbroking, 532 bulkers totaling 37.4 million DWT traded hands in the first half. This is 143% above tonnage sold in the first half of 2019.

Clarksons’ secondhand bulker value index is up 38% since the beginning of the year.

Unlike in the tanker market, higher bulker sales activity and valuations are being supported by strong freight rates, which are at 10-year highs for medium- and smaller-size bulkers.

Dry bulk also faces more constraints on the newbuild front than other segments, which increases secondhand buying interest in secondhand tonnage when spot rates are high.

First, steel input costs make up a larger portion of the overall bulker newbuild cost than for more complex vessel types. Second, yards make higher margins building container ships, gas carriers and tankers than they do with bulkers. Third, bulkers are harder to “future proof” against yet-to-be-written decarbonization rules than other ships, because the expense of installing dual-fuel systems represents a larger portion of the overall newbuild cost.

According to Braemar ACM Shipbroking, “As orders for new bulk carriers have been suppressed, the secondhand market has been extremely hot. Secondhand values for bulkers, especially older tonnage, have made hefty gains. We expect activity to remain heated in the coming months as owners use this avenue to renew fleets and engage in the strong spot market.”

Click for more articles by Greg Miller

Related articles:

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now