The highlights from Thursday’s SONAR reports. For more information on SONAR — the fastest freight-forecasting platform in the industry — or to request a demo, click here. Also, be sure to check out the latest SONAR update, TRAC — the freshest spot rate data in the industry.

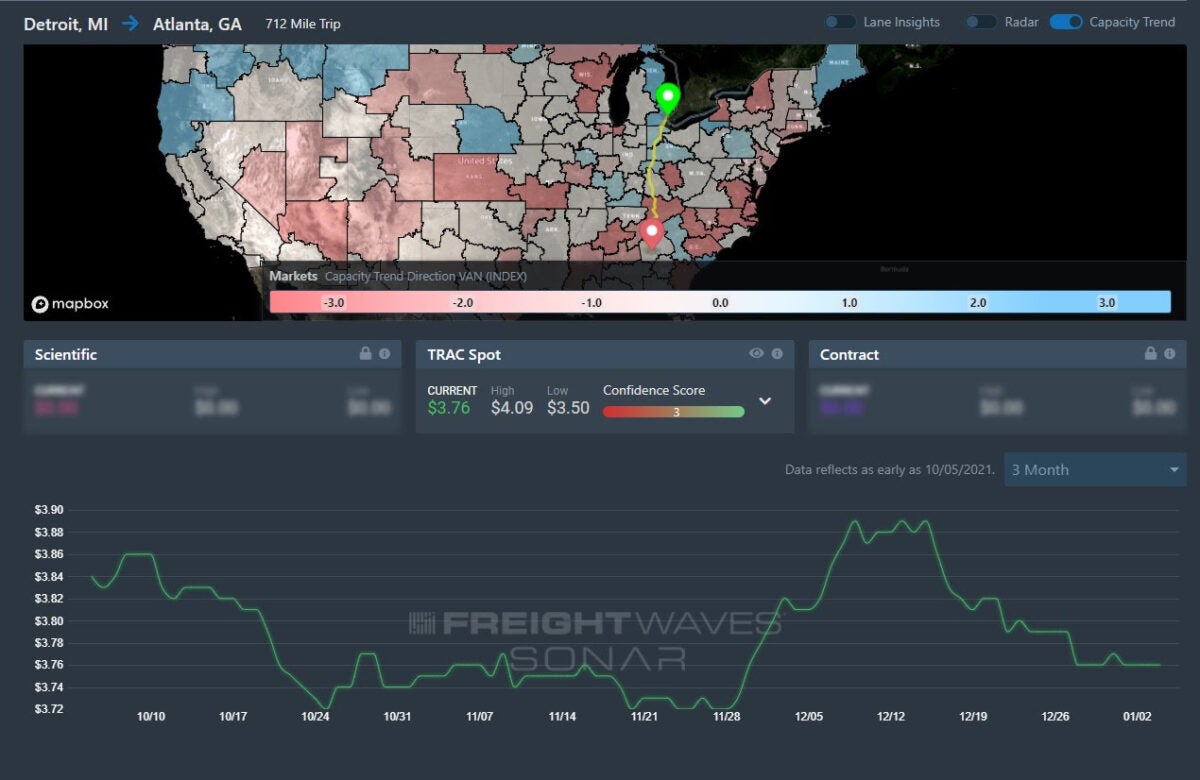

Lane to watch: Detroit to Atlanta

Overview: Spot rates decrease as capacity loosens because of a decrease in tender rejections.

Highlights:

- Outbound tender rejections decreased in the Detroit market 45.5% – from a high of 42.5% in late December 2021 to 19.33% this week.

- The Atlanta market tender rejections remain at 18%, in line with seasonal trends compared to 24-30% rejections during spring produce surges.

- FreightWaves TRAC spot rates for the Detroit to Atlanta lane decreased 13% from late December highs of $3.89 per mile, leveling out at $3.76 per mile to date during the first week of January.

What does this mean for you?

Brokers: Continue to develop a dense carrier network to drive down rates, as the recent surge in tender rejections appear holiday-related. Spot rates remain elevated but expect to see downward rate pressure if tender rejections continue to drop (which indicates carriers have capacity or are honoring their contracted rates for the lane). If stuffing on contracted lanes, benchmark internal rates compared to other customer accounts to see if the contracted rates are no longer competitive to secure capacity.

Carriers: Tender compliance will be a priority in the coming weeks as drivers return to work and customers attempt to tender shipments that they couldn’t find capacity for during the holidays. The sky-high rejection rates from late December put carriers in a situation of customer relationship management due to dwindling capacity. Managing customer expectations over the next few days will be crucial.

Shippers: Loosening capacity presents an opportunity for pushback on tender acceptance and service expectations. Both carriers and brokers took advantage of the fourth quarter 2021 surge and now there is an opportunity to identify potential savings if spot market rates decrease, or a recently completed RFP went into effect. Both carriers and brokers will seek to repair relationships strained from the holiday capacity crunch.

Watch: Carrier Update

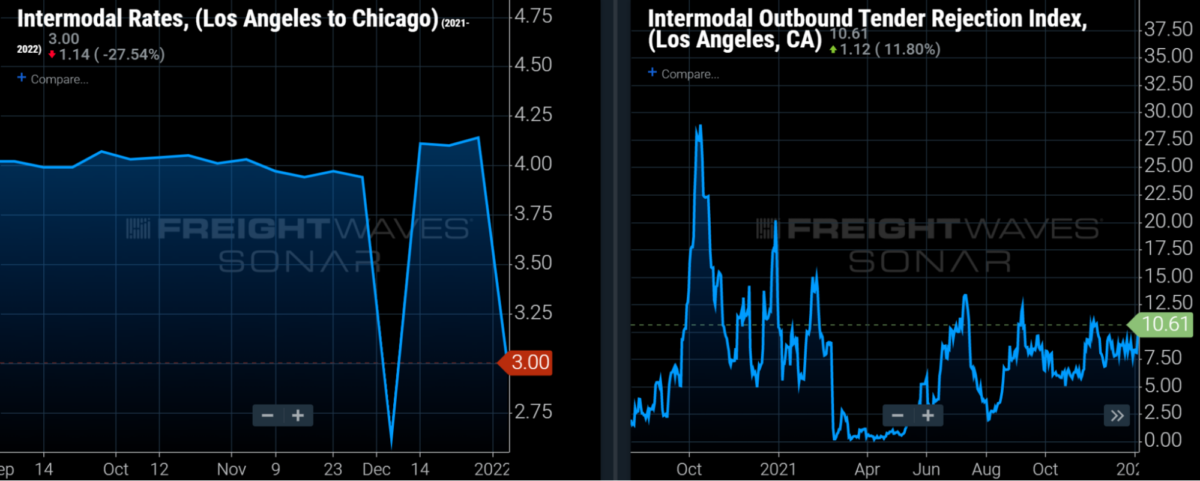

Lane to watch: Los Angeles to Chicago

Overview: Intermodal spot rates fall sharply, suggesting that there is more available intermodal capacity for outbound LA loads.

Highlights:

- In the past week, the door-to-door intermodal spot rate in the LA to Chicago lane declined by 27.4% (from $4.14/mile to $3.00/mile). Both quotes include fuel surcharges.

- The intermodal spot rates in the other major outbound LA intermodal lanes (i.e., LA to Dallas and LA to Atlanta) also declined by more than 20% in the past week, which suggests that intermodal capacity is becoming more available for outbound LA loads.

- The latest average dry van truckload spot rate in the LA to Chicago lane is $3.71/mile, including fuel surcharges, with $3.87/mile and $3.48/mile representing rates in the 67th and 33rd percentiles.

What does this mean for you?

Brokers: Raise your rates in the lane in order to preserve margins given that other brokers are paying more for dry van capacity in the lane. For those able to broker intermodal loads, that may again be an option for minimizing purchased transportation costs on less time-sensitive loads given the latest change in intermodal spot rates.

Carriers: Chicago is a solid destination for carriers currently; its van outbound tender rejection rate of 21.8% is 383 basis points (bps) above the national tender rejection rate and its status as a headhaul market. With intermodal rates significantly below dry van rates, loads requested in the lane are likely to be service-sensitive so look to be compensated accordingly.

Shippers: The latest intermodal spot rate is 19% below the latest dry van truckload rate, so intermodal is again a viable option for spot shippers. However, that could easily change in the coming weeks given that spot rates in the LA to Chicago lane have been highly volatile of late.

Watch: Shipper Update

Lane to watch: Richmond (Va.) to Atlanta

Overview: Spot rates are likely to climb in the days ahead as the Headhaul Index surges 27% w/w).

Highlights:

- The Port of Norfolk’s weekly maritime import shipment volumes have been at near-record highs for the last few weeks.

- The Headhaul Index in Richmond is up 27% w/w, but is positioned to climb further in the next week as import volumes remain elevated with pre-Chinese New Year cargo.

- Outbound tender volumes in Richmond are already up 30% w/w, and are expected to move higher.

What does this mean for you?

Brokers: The Richmond truckload market is likely to tighten significantly in the days ahead. Already, there has been a 27% w/w in outbound tender volumes, and with record import volumes pouring into the Port of Norfolk for the last few weeks, demand for truckload capacity in Richmond is likely to grow. Make sure you are getting your outbound Richmond loads booked earlier than usual, and be on watch for significant upward pressure on spot rates in the weeks to come.

Carriers: Stay firm on your rates; you are likely to see pricing power shift further into your favor in the days ahead. A large percentage of import volumes into the Port of Norfolk move inland via drayage carriers into the Richmond market. With near-record import volumes moving into the Port of Norfolk over the last few weeks, outbound truckload volumes in Richmond stand to benefit and the increase in demand will put even more upward pressure on spot rates.

Shippers: Your shipper cohorts currently have tender lead times at 2.8 days, but that is not likely to be enough for the increase in demand that is expected in the weeks ahead. In the tightest markets historically, shippers in Richmond have increased lead times to between 3 and 3.5 days to help offset tightening conditions in the outbound truckload market.