The Chicago freight market is showing signs of normalizing after a hotter than average environment in the heart of winter. Spot freight in January and the first half of February was super hot, outpacing contract rates and showing an unusual pattern that is normally not seen.

In a normal winter, freight movements typically decline in late December and early January as shippers decrease activity. Shippers demand slows down as employees take time off, consumers slow spending and pay down credit, and commercial capex budgets take a breather after the New Year. Additionally, demand tapers as people retreat indoors and are less active as consumers.

This year was different. The overflow of freight that was left over from the end of the year, combined with the capacity crunch exacerbated by the ELD mandate, caused spot pricing to stay unusually strong. We believe the ELD “shock” was a short-term phenomenon related to drivers getting used to the technology, drivers that were uncomfortable dealing with the technology, and general confusion caused by the operation of the tech.

Chicago is a major hub in the freight marketplace, with an outsized role in the U.S. industrial sector. Automotive and heavy manufacturing are major industries in the region. Chicago is also a major inland port of containers coming in from overseas. If you want to predict trends in the US industrial economy, without being influenced by the energy or seasonal markets, Chicago is a bellwether.

We are seeing early indicators that the hyperinflation in the spot market in Chicagoland is starting to soften, as shippers shift demand away from the spot market carriers and into committed contractual providers.

In the first part of January, shippers were still using 2017 rates that were at the end of the cycle and lower than carriers would be willing to accept. In turn, carriers were rejecting those loads. These rates were set in the 2017 bid season by carriers that offered aggressively priced lanes, in return for volume at a time when the market was soft. When the spot-market heated carriers were not willing to honor those inferior rates, or willing to accept excess surge loads that shippers had requested above their base commitment.

According to DAT, in January outbound spot rates out of Chicago to Atlanta climbed from $2.57 to $2.84/mile and $2.14 to $2.26/mile in the Chicago to Dallas lane.

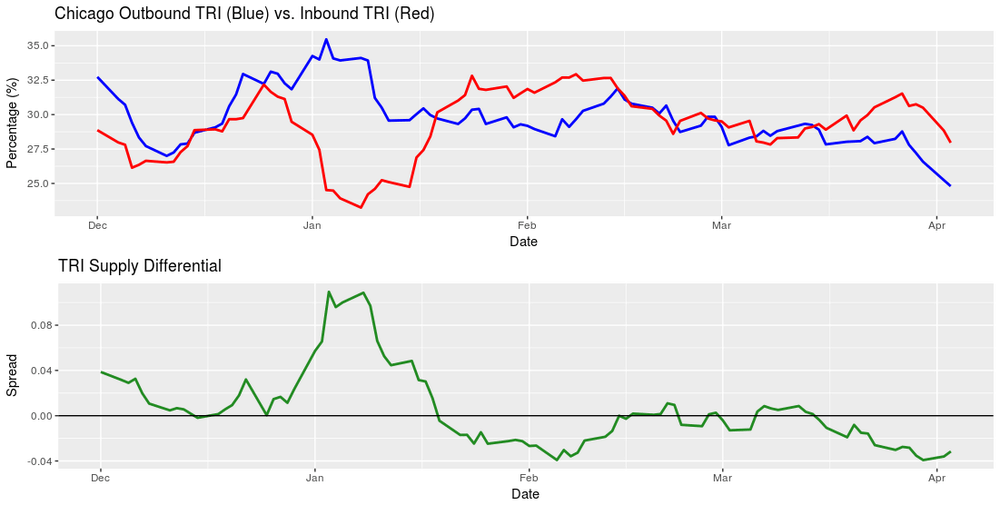

We can see how carriers played this market by looking at our TRI (Tender Rejection Index) and examining what percent of loads were rejected in January and following it through the rest of the quarter. We also can compare inbound tenders to outbound tenders and what the inbound and outbound rejection ratios would indicate.

What we saw was telling: Chicago’s unusual spike in spot market pricing was led by a heavy positive inversion of the Tender Rejection Index Outbound (TRI-O) and the Tender Rejection Index Inbound (TRI-I). With capacity so tight in the market out of Chicago related to ELD implementation and higher than normal spot rates, carriers were shifting a significant amount of capacity in the Chicago market to take advantage.

Simply stated, carriers were aggressively moving capacity into Chicago to take advantage of higher than normal spot rates. We believe the unusual development in early January was almost entirely related to the ELD shock and not fundamental to the long term trend of the market. After the initial adjustment period, the Chicago market stayed in balance for much of the first quarter with an end of the quarter surge that follows normal patterns.

Shippers in the market that were exposed to higher than normal spot pricing or higher concentrations in spot loads ended up finding ways to cope. This was in the form of higher committed rates, in return for consistent capacity supply or dedicated capacity from large enterprise carriers. When the new bid awards came out, shippers were eager to offer carriers their asking price. As we predicted back in September, carriers have been able to secure double-digit rate increases in their new contracts.

The new contract rates tend to come into effect in late March and April. By looking at the data, the outbound action in the market shifted from the spot market and into the contract market. Carriers are honoring these tenders with far less rejections than we saw earlier in the year, suggesting they are happy with their new rates out of Chicago.

We believe that the Chicago spot market has corrected and is headed back to normal cycles. Unfortunately for carriers that were hoping for an April 1 ELD enforcement mandate to create a capacity crisis, this does not appear to have happened. As technical traders would say, the ELD hard enforcement has been priced into the market.

Stay up-to-date with the latest commentary and insights on FreightTech and the impact to the markets by subscribing.