The Food and Agriculture Organization of the United Nations (FAO) Food Price Index averaged 135.7 points in January, 1.1 percent higher than December and the highest level in 11 years. Driving the latest increase were month-over-month increases in the FAO Vegetable Oils Price Index and the Dairy Price Index of 4.2% and 2.4%, respectively.

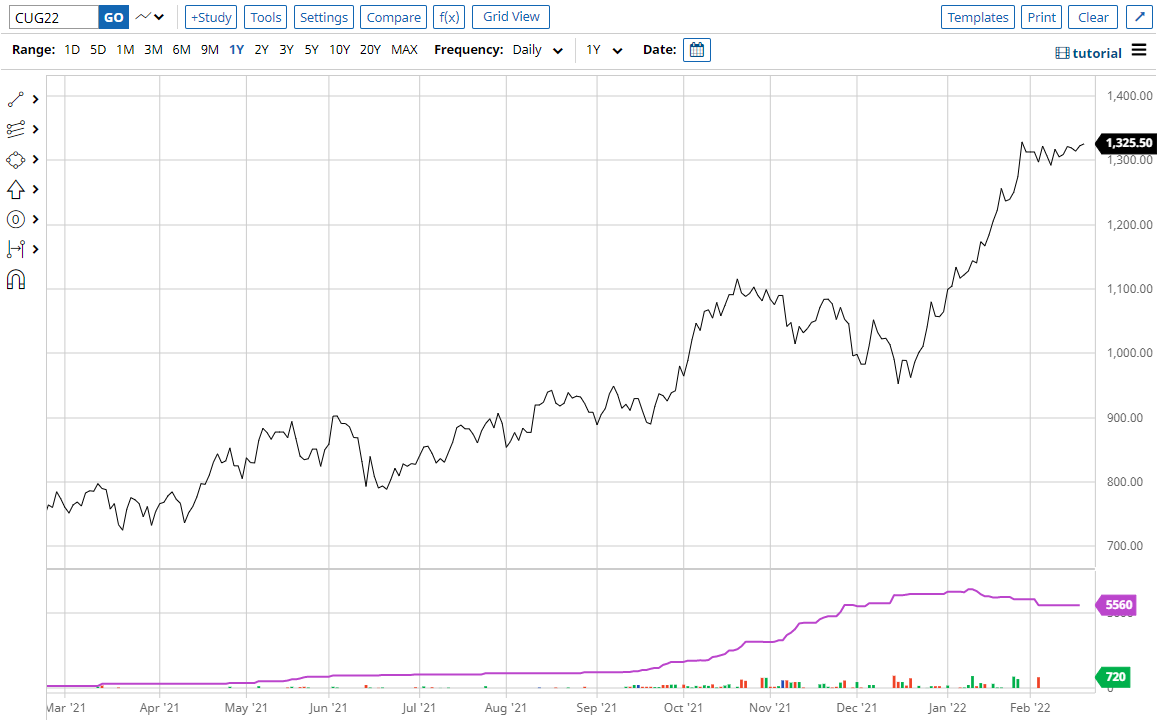

Palm oil is one of the components of the FAO Vegetable Oils Index, and its rise reflects concern that Indonesia, the world’s largest palm oil exporter, will curtail export volume. Palm oil is an ingredient in a wide range of food products, including ice cream, and personal care products, such as detergent and beauty products. In January, in an effort to control inflation in its own country, Indonesia issued a mandate requiring producers in the country to set aside 20% of palm oil shipments for domestic buyers. That mandate exacerbated rising palm oil prices caused by a typhoon that hit Malaysia. Malaysia and Indonesia are the primary sources of palm oil worldwide, representing about 85% of global output. For more detail, see this article from Mongabay.

Source: Barchart.com Inc.

On its most recent earnings call, consumer products giant Unilever cited palm oil as being one of the key drivers of its cost inflation, with palm oil prices up 130%, and as having particular impact on its beauty and personal care segments. Interestingly, one of the reasons that Unilever has given investors for its relatively low market share in Indonesia is that its competition, which is local to Indonesia, is vertically integrated, owning its own palm oil plantations.

Winsight Grocery Business breaks down recent share gains that national-brand CPG companies have made against private-label brands. According to IRI and Boston Consulting Group, overall CPG dollar sales rose 2.7% in 2021, on top of the extraordinary 10.6% sales growth in 2020. CPG sales volume declined 2% last year but is up 4.3% on a two-year stack. Large CPG companies (sales greater than $6 billion) gained 0.2 percentage points of market share to 45.9%. IRI/BCG found that private-label brands lost 0.4 percentage points of market share to 15.5% of CPG dollar sales.

The implication from putting the above sales numbers from IRI/BCG together suggests that retail inflation in CPG items was about 4.7% in 2021, on average, which is consistent with the “mid-single-digit” price increases that many of the public CPG companies have reported. Meanwhile, most CPG companies experienced cost inflation last year that exceeded that level, with some seeing cost inflation in the high single digits and others well into the double digits. That led to a degradation in gross margins which was modest for some CPG companies, such as branded food companies, and more severe for others, such as cleaning products companies. Most CPG companies plan further rounds of price increases in the coming months to restore margins to pre-pandemic levels, but some expect it to take 12-18 months, or longer, to fully restore margins to pre-pandemic levels.

Food Navigator describes PepsiCo’s investments to mitigate its supply chain challenges. Those investments include adding fulfillment centers, working on its last-mile delivery strategy, hiring 15,000 employees and launching a Frito-Lay direct-to-consumer site. In addition to the challenges that seemingly all CPG companies have faced of late, Pepsi highlights the rising cost of cooking oil as one of the major ingredients in cost pressure. Pepsi has been a strong performer during the pandemic as consumers bought more snack items, and those snacking habits, at least so far, have stuck.

To sign up for The Stockout, FreightWaves’ newsletter focused on CPG supply chains, please click here.

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

Future of Rail Symposium

Reshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post • Chicago, IL Register NowReshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

The Signal at Chattanooga Choo Choo • Chattanooga TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now