If your business thrives when spot rates are high, there is both good and bad news. The bad news is that those rates haven’t found a floor yet. The good news is that they likely will in the next three to six months, and then start climbing again in the second half of 2023.

At least that’s the most widely shared opinion of the nearly 400 carriers and brokers/3PLs that FreightWaves Research surveyed last week. Asked when spot rates would hit rock bottom in the current cycle, 44.05% answered Q1 2023, and an additional 25.57% said Q2 2023. Just 13.42% thought the trough would come in Q3 or later.

[Source: FreightWaves Research]

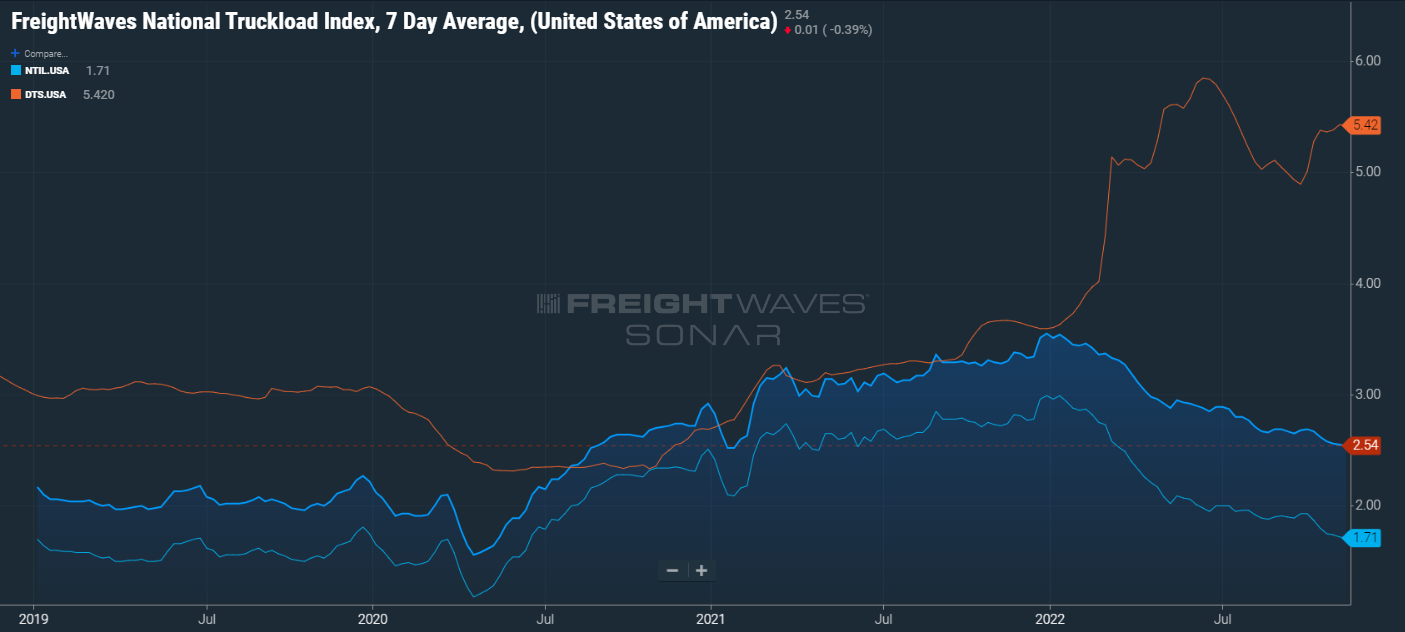

Spot rates have already hit their lowest point, said 16.96% of respondents, or about one in six. It’s possible rates have started climbing again for their businesses, but FreightWaves’ National Truckload Index (NTI.USA) — a seven-day moving average of spot rates — has continued to drop since the survey was first emailed. The index registered around $2.58 on Nov. 7 and currently stands at around $2.54.

Additionally, NTIF.USA, a 30-day forecast based on historical rates, imports, wholesale fuel prices and contract rate data, is projecting NTI.USA will sit around $2.45 in the middle of December.

This means carriers aren’t out of the woods yet. But they might now be seeing glimmers of sunlight.

[Source: FreightWaves Research]

There is consensus that rates will turn around once we move past the first half of 2023. See the trend shown from the three most common answers for where respondents thought rates would be at the beginning of each of the following quarters.

Watch: When will the spot market bottom out?

Q2 2023 (6 months from now)

- 10 – 19% lower (21.27%)

- 1 – 9% lower (19.75%)

- About the same (18.99%)

Q4 2023 (12 months from now)

- 1 – 9% higher (22.53%)

- About the same (21.03%)

- 10 – 19% higher (15.95%)

Q2 2024 (18 months from now)

- 1 – 9% higher (24.30%)

- 10 – 19% higher (21.01%)

- About the same (14.43%)

If you analyze results for this question by way of weighted averages, in which 7 equals “About the same,” you see scores of 5.95 for Q2 2023 (1%-9% lower), 7.14 for Q4 2023 (About the same) and 7.81 for Q2 2024 (1%-9% higher).

A difficult time for carriers

Many carriers have been battered by high fuel prices and equipment costs in 2022. They’ve also had to contend with inflationary pressures driving down consumer and industrial demand. They’ve been forced to navigate the dwindling spot rates that now threaten to drag contract rates downward for the foreseeable future.

For most of this year, tendering freight to the spot market has been dramatically cheaper than contracted freight, but that reality won’t hold forever. The spread will naturally start to narrow, as contract rates are bid lower to better reflect the spot market. The percentage of contract freight and compliance should decline. If this starts happening, more freight will be shifted to the spot market, changing the balance between load volumes and truck capacity.

Q4 2022 shows the freight market at an interesting place. As peak season approaches (or doesn’t), so too does rock bottom for carriers’ market disadvantage. It remains uncertain what kind of seasonal bump volume and rejections data will see from holiday consumption, if any.

Currently, the Outbound Tender Reject Index in FreightWaves’ SONAR (OTRI.USA) is hovering right around 4% as volume (OVTI.USA) continues to fall with it. That 4% rejection rate is lower than at this time in 2019 — the last genuine down year for carriers — and most analysts believe this peak season will do little to balance the market in a meaningful way.

A little more info on carriers and brokers

[Source: FreightWaves Research]

Every fleet size we surveyed chose Q1 2023 as the most common expectation for rock bottom spot rates, except for those with 250-999 tractors. The most common answer for that group was Q2 2023.

[Source: FreightWaves Research]

The broker trend was slightly more suggestive of differing opinions depending on the size of the company. Like carriers, most brokers believe the bottom will hit in Q1 2023. But something interesting happens as the brokerages’ gross revenue increases: It becomes more likely that respondents believe the bottom is coming in Q2.

If there is a credible explanation for this, it might be that large brokerages tend to be less exposed to the spot market, and therefore could be less in touch with the challenges that smaller brokers are already facing.

Want to see this data before everyone else?

It doesn’t have to be an industry secret. Our most diligent subscribers get this data ahead of time, and you could too.

Are you a carrier, shipper or intermediary (broker/3PL)? If you fall into one of those groups, you’re eligible to take part in future surveys like this one by signing up for our newsletters (NOTE: don’t forget to specify your industry where asked).

For almost all of our surveys, respondents get instant access to results once they submit. You can subscribe here.

Related articles:

Adan kula oshow

I am good drive of truck. anyone can help me to get this job I am ready plz contact me +254712194177 Joe help me to get drive Job plz for the sake of God