Management from Covenant Logistics Group provided some optimism regarding the truckload market on a call with analysts Thursday. Customers making progress reducing inventories, capacity leaving the industry and the work the company has done to reduce cyclicality in its business model were some of the reasons for the upbeat tone.

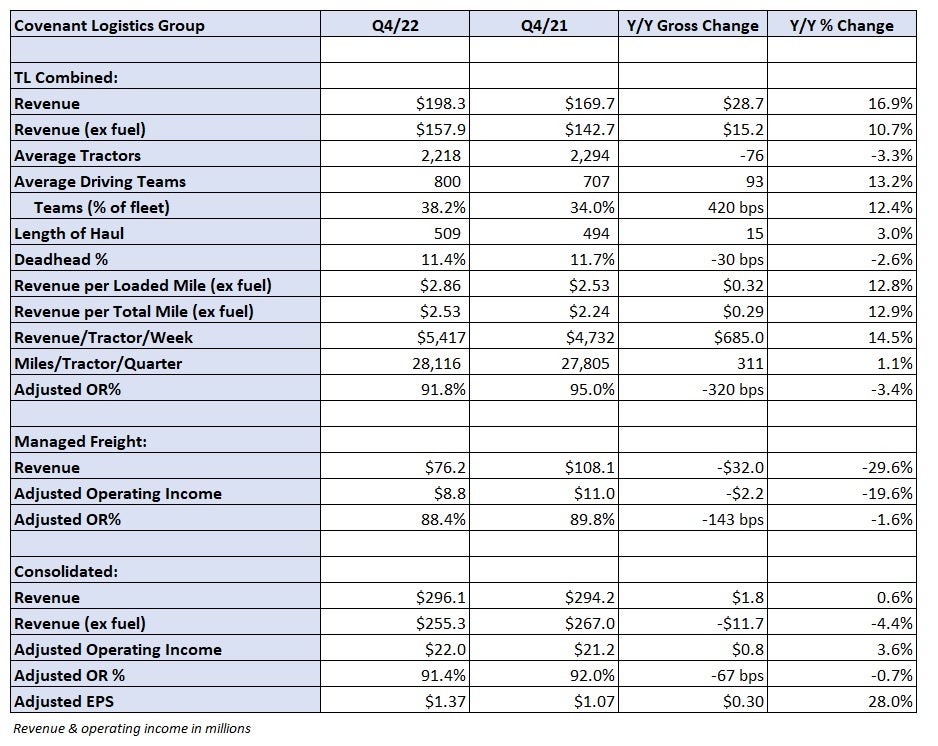

Covenant (NASDAQ: CVLG) reported $1.37 in adjusted earnings per share for the fourth quarter Wednesday after the market closed. The number missed consensus expectations by a nickel and excluded what it expects to be non-recurring charges.

“I think that we hit the bottom around Thanksgiving and I think that we’ve just been there,” said David Parker, chairman and CEO. “We’ve not seen a second downward trough below Thanksgiving and we have sensed that all in the month of January as well.”

Parker expects negative gross domestic product in the first half of 2023 but thinks the company’s customers will have whittled inventories to desired levels at some point in the second quarter. Covenant’s pipeline is strong, “better than you think it would be in the month of January,” and only a few of its accounts are really pushing back on pricing, he said.

Revenue in Covenant’s TL segment increased 17% year over year (y/y) to $198 million, up 11% excluding fuel surcharges. Revenue per tractor per week increased 15% on an average fleet count that was down 3%. The company’s dedicated fleet was down 10% y/y as unprofitable accounts were exited and some customers reduced the number of trucks needed daily.

The expedited segment logged a 17% y/y increase in revenue per tractor per week to $7,639. The period benefitted from loads from the Federal Emergency Management Agency, which were tied to Hurricane Ian relief efforts. The dedicated fleet saw the metric increase 6% y/y in the quarter.

Covenant has been relying more on its brokerage unit for loads to fill its trucks as freight demand has diminished. Currently, brokered loads account for 5% of the mix compared to as little as 1% when the market was stronger.

“The rates on that 5% are 1990 rates,” Parker said. “I mean it’s the most horrible thing I’ve ever seen. The rates are pathetic, especially coming off the West Coast. Two plus two does equal four. You can’t haul 1990 rates with 2023 costs and think you’re going to stay in business. I think in the next couple of months we will see a rush of capacity that is going.”

He hopes to have a good portion of the brokered freight replaced by new accounts in the next 30 days where the rates are almost double. Roughly 70% of Covenant’s customer book is customized, engineered or niche and is performing well above spot market rates.

“When they start buying more Coca-Colas and it gets warm in May … the end of April … freight is going to pick up even if it’s a negative GDP growth,” Parker said. “We’re just having to muddle through it.”

The combined TL fleet recorded a 91.8% adjusted operating ratio, 320 basis points better y/y. Increases in salaries, wages and benefits (up 310 bps y/y as a percentage of revenue) and insurance and claims (up 150 bps) were headwinds.

Truck deliveries ramp up in Q4; unadjusted EPS takes hit

During the quarter, Covenant recorded roughly $10 million (57 cents per share) in incremental expenses tied to breaking equipment leases early, disposing tractors and poor utilization. The company made the decision to park roughly 600 units, those with the highest maintenance costs and worst fuel efficiency, as diminished demand and lower rates no longer warranted their use.

Covenant’s operations and maintenance expense was roughly 21 cents per mile in 2021. That number ballooned to 29 cents per mile in 2022, rapidly increasing as the year progressed. In some instances, the carrier was layering additional trucks into the daily budget at dedicated accounts just to account for breakdowns.

Covenant took delivery of 250 units above its normal trade plan in the quarter, which represented more than half of its entire 2022 truck order. Also, it saw delays returning tractors to lessors in proper working condition due to parts shortages. Management said the goal is to split the difference between the recent cost-per-mile averages, noting broad inflation will likely keep the 21-cents-per-mile number out of reach.

In addition to a lower maintenance cost profile and improved fuel efficiency, increased uptime will provide a cost tailwind. Also, the company will see an increase in gains on sale, roughly $1 million in the fourth quarter, as it will be selling owned equipment in the coming months versus simply turning in leased trucks. Covenant plans to take delivery of 900 new tractors in 2023 compared to an initial expectation of 600 units.

While the excluded charges aren’t true one-offs and represent events that typically occur in the normal course of operations, they have been excluded from results due to the magnitude of the activity in the quarter. However, there could be a tail to these incremental expenses given the increased purchasing plan in 2023.

Covenant lowered its average tractor age to 2.1 years during the quarter, which was flat year y/y but down from 2.4 years in the third quarter.

The EPS number saw a 2-cent headwind due to lower contribution from its minority interest in a leasing company. That was more than offset by an 8-cent benefit from higher gains on equipment sales and a lower tax rate when compared to the 2021 fourth quarter.

2023 outlook

Looking forward, Parker is becoming “more and more bullish.”

He believes changes to the business model have made the company’s earnings less volatile. Recent investments in sales and the acquisition of a hazardous materials hauler a year ago should provide some topline catalysts. Also, Covenant is lowering its cost structure through fleet upgrades and should see some improvement in claims, given better safety metrics.

In past downturns, Covenant’s earnings would fall by 50% to 75%. However, the goal is to minimize EPS degradation to just 25% to 30% this year. Much of that depends on the macroenvironment.

“No doubt things are soft out there, but our cost structure for the first quarter is going to look better than our cost structure in the fourth quarter,” said Paul Bunn, president and COO. “Revenue won’t be as robust, but our cost structure will be better.”

Covenant is not going to play the rate game with shippers and will allow accounts to walk if the relationship doesn’t provide value both ways.

“We will go do other things,” Parker said. “Whether that means reduce our trucks, whether it means go do acquisitions, whether it means repurchase stock, whatever that means we will do whatever the market tells us to do. I am bullish during a very bleak time out there that there’s going to be a lot of opportunities going forward.”

Revenue in the managed freight segment fell 30% y/y to $76 million due to a tough y/y comp and a muted peak season. Adjusted operating income was down 20%, but the segment’s adjusted OR improved 140 bps to 88.4%, or an 11.6% operating margin. Looking forward, margins are expected to return to pre-pandemic levels of mid-single-digit percentages as capacity is rationalized and some brokers remain very rate competitive.

Covenant’s guidance calls for net capital expenditures between $75 million and $85 million in 2023, including $87 million to $97 million in equipment purchases. The company recently sold a terminal, netting $12 million that will be used to offset capex during the year. Covenant recorded $48 million in net capex during 2022.

Investors appeared less optimistic Thursday about the company’s earnings bridge to 2023. Shares of CVLG were down 20.3% at 2:30 p.m. EST compared to the S&P 500, which was up 0.7%.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now