Several states this week announced plans to begin reopening their economies. That could mean that non-essential freight, which has been almost non-existent in some areas, could return as well. But, moving goods into areas with no outbound loads could be costly, and the overall environment for trucking conditions remains negative, according to consulting firm FTR.

FTR’s most recent Trucking Conditions Index (TCI) fell to 0.96 in February. While still positive, it didn’t account for the steep decline in the economy since that date that occurred as most states issued shelter in place orders.

The TCI tracks changes in freight volumes, freight rates, fleet capacity, fuel price, and financing.

“Although trucking conditions might prove to be comparable to the worst of the Great Recession, the trucking industry – like the rest of the economy – has never seen such an abrupt deterioration,” Avery Vise, vice president of trucking, said. “The need to restock grocery shelves provided a brief boost for some segments, but the economic shutdown now has taken a toll on the whole industry. While an economic restart likely will begin in May, the damage wrought during this period will weaken trucking conditions for months to come.”

FTR is predicting the TCI will shift into negative territory for its April and May readings and remain that way into 2021.

Those readings could get a boost in the weeks ahead as businesses in some states begin reopening. Georgia, Tennessee, Texas and Florida all announced some level of opening up of society. In Georgia, Gov. Brian Kemp announced many businesses could reopen. South Carolina has lifted restrictions on retail stores and Tennessee Gov. Bill Lee said his state’s stay-at-home order would expire on April 30. A similar announcement came from Texas governor Greg Abbott.

Even in hard-hit states like New York, Washington and California, there has been optimism of relaxing some restrictions in the weeks and months ahead, and all of this adds up to freight demand as stores replenish supplies and consumers start spending again.

Still, the numbers are not good in a market that has too much capacity and not enough freight. ACT Research’s For-Hire Trucking Index for March showed further contraction for both volumes and freight rates, now at 42.4 and 43.2. Productivity, while neutral at 50.0, likely was supported by the temporary pantry-stocking phenomenon, it said.

Tim Denoyer, ACT Research’s vice president and senior analyst, said the readings were a little surprising.

“Because of the talk surrounding a surge in freight driven by pantry stocking, the Volume Index decline was somewhat surprising, but likely reflects the start of shutdowns late in March,” he said.

Rates will remain under pressure, Denoyer said.

“COVID-19 is adding a new level of pricing pressure due to the sharp decline in load volumes into an already overcapacitized market. Our for-hire carriers continue to show better capacity discipline than the industry at large, which we see as a good leading indicator of tighter capacity down the road,” Denoyer said.

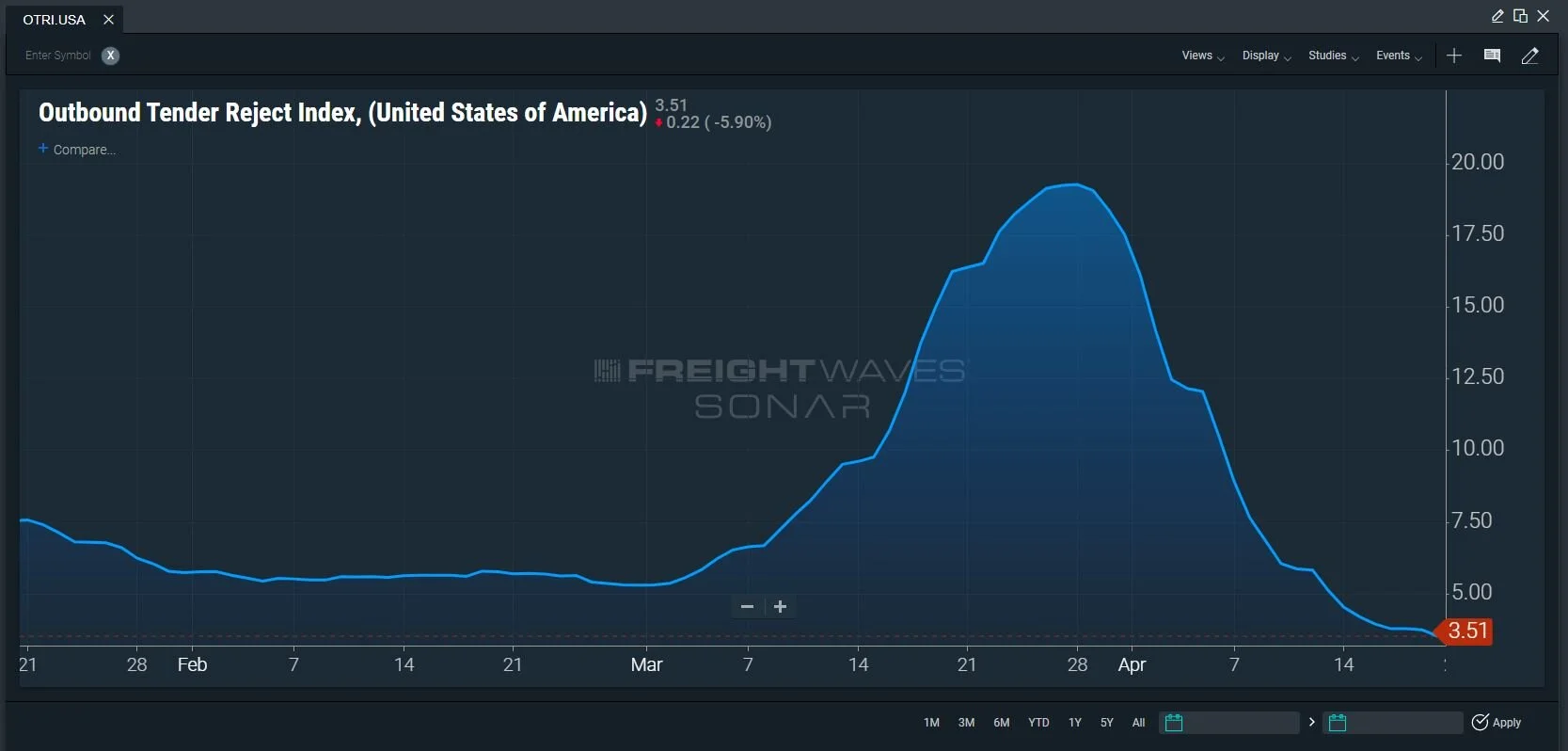

Some of this dynamic is being displayed in FreightWaves’ Tender Reject Index (SONAR: OTRI.USA). OTRI.USA, which measures carriers’ willingness to accept loads that are tendered to them by shippers under contract terms, expressed as a percentage of loads rejected to total loads tendered, has fallen to 3.51, down from a rate of 19.35 on March 28.

An oversupply of capacity is also pushing down rates, and without a clear vision of what will happen in the months ahead, rates are only showing moderate potential increases. FreightWaves’ Predictive Rates tool in SONAR allows users to input origin and destination lane pairs and it provides low, median and high price targets for rates along that lane for future dates.

For instance, Los Angeles to Atlanta is showing a rate range of $1.06 per mile to $1.46 per mile (excluding fuel surcharge) on May 21. It stays in that range until the fall when it rises to $1.18 to $1.66 on Oct. 21.

A similar story is unfolding along the Ontario, California, to Atlanta lane. The Predictive Rate tool is suggesting rates will range from $1.09 per mile to $1.50 per mile with a median of $1.30 on May 21. Longer range, the price target is $1.21 to $1.71 on Oct. 21.

Rates from Los Angeles to Dallas, Texas, have a slightly higher projection, ranging from $1.29 to $1.77 on May 21 and showing further strength in the fall with a range of $1.39 to $1.95 on Oct. 21. The rate along the Los Angeles to Dallas lane over the last seven days, according to Truckstop.com data found within SONAR (SONAR: TSTOPVRPM.LAXDAL), is $1.15 per mile.

The one-month rate range prediction on the Dallas to Atlanta lane is $1.26 to $1.52 with a six-month range of $1.17 to $1.44. The Dallas to Atlanta rate (SONAR: TSTOPVRPM.DALATL) over the past seven days, according to Truckstop.com, is $1.15 per mile.

Even as states reopen, there is too much uncertainty ahead to predict boom times returning, but there is finally some optimism appearing.

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

Future of Rail Symposium

Reshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post • Chicago, IL Register NowReshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

The Signal at Chattanooga Choo Choo • Chattanooga TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now