Management from Forward Air told analysts on its third-quarter earnings call Thursday that “cleansing” its customer book drove record results in the period.

The Greeneville, Tennessee-based asset-light trucking and logistics company has been upgrading the freight mix to include “denser, high-value freight.” Forward (NASDAQ: FWRD) is maximizing yield per shipment by focusing on a mix that is skewed toward industrial tech and parts versus lighter and lower-margined e-commerce parcels.

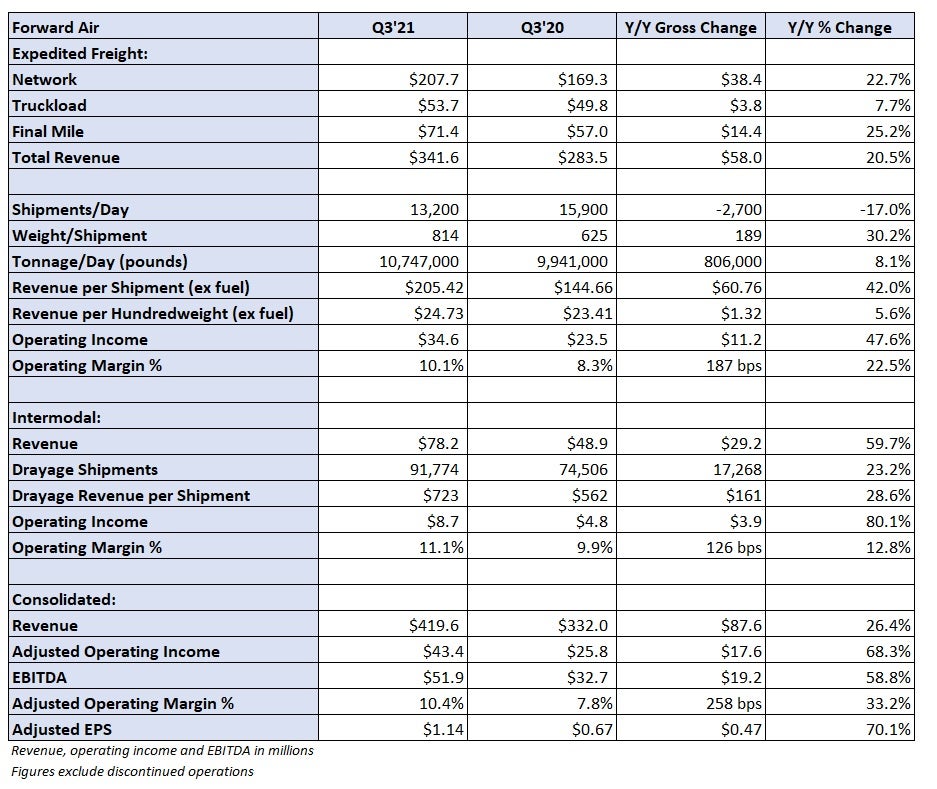

The improvement was notable in the period as less-than-truckload tonnage per day in the expedited segment was up 8% year-over-year even though daily shipments were down 17%. A 30% increase in weight per shipment to 814 pounds provided the difference.

A 6% increase in yield, or revenue per hundredweight excluding fuel surcharges, filled out the rest of the 23% revenue increase for the segment.

“We executed a transition throughout the quarter,” said Tom Schmitt, chairman, president and CEO. “We are working, and we did work, very closely with our LTL customers, eliminating inefficient freight — inefficient meaning loose, oversized, nonpalletized [freight] — from our system.”

Schmitt said the plan has worked as the network is unclogged and incremental capacity has been created as shipment counts have been reduced.

The impact was notable in September, when the company recorded its highest monthly net income as LTL weight per shipment (+30% year-over-year) and revenue per shipment (+50% year-over-year) were also the highest on record. The LTL margin for the month was 17.5%.

Forward is going to continue to push the initiative and is selling its offering to beneficial cargo owners and commercial shippers, which management said will complement its traditional 3PL and forwarder customer base.

Through the first half of October, LTL revenue was up 35% year-over-year as daily tonnage accelerated further, up 13.1%.

The operating margin in the expedited segment, which also includes truckload and final mile, increased 190 bps year-over-year in the quarter to 10.1%.

On a consolidated basis, Forward reported adjusted earnings per share from continuing operations of $1.14, 7 cents better than the high end of its guidance range and the consensus estimate. The result was 47 cents higher than the year-ago quarter.

Revenue growth of 26% year-over-year to $420 million was slightly below management’s guidance range of up 28% to 32%.

Continuing operations exclude the high-frequency pool distribution segment, which was sold in February.

New guidance calls for 20%-plus EPS growth in 2022 and 2023

Forward is calling for more “double-doubles” (double-digit margins along with double-digit revenue growth) on a go-forward basis.

Fourth-quarter revenue is expected to increase between 23% and 27% with earnings per share of $1.25 to $1.29, ahead of the current consensus estimate of $1.16.

The company also laid out longer-term growth targets.

It is calling for full-year 2023 revenue to range between $2 billion and $2.6 billion (compared to approximately $1.64 billion this year at the midpoint of the guidance range) with EPS of $6.30 to $6.70 (compared to adjusted EPS of $4.30 to $4.34 in 2021).

The growth isn’t weighted toward any specific period as management expects 2022 to include more double-doubles and split the 2021 and 2023 EPS forecasts. Essentially, management sees a runway to grow earnings in excess of 20% in the next two years.

Schmitt said the 2023 revenue result will depend on organic growth and that the high end of the range is dependent on M&A. He expects significant organic LTL growth as terminals will be added and the intermodal and final-mile segments see margin improvement. He said acquiring a brokerage operation would provide Forward with additional capacity, allowing it to take on more LTL volume.

“What we’ve seen in the last year is there are cases and there will be cases where our customers are calling on us and they are going to want to rely on us to move their freight. They are asking us to flex beyond those two sources of power [drivers and independent contractors],” Schmitt said. “Enhanced focus on brokerage means finding access to quality power that allows us to flex up in those situations.”

Shares of FWRD closed up more than 5% Thursday compared to the S&P 500, which was up 1%.