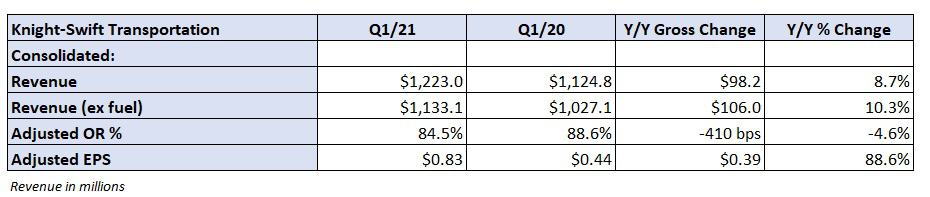

The nation’s largest truckload carrier, Knight-Swift Transportation (NYSE: KNX), posted a better-than-expected first quarter Wednesday. The Phoenix-based company reported adjusted earnings per share of 83 cents, 13 cents ahead of consensus and 39 cents better than the year-ago quarter.

The quarter benefited from a reversal of almost $23 million in other income when compared to the prior year. “The year-over-year improvement was primarily driven by gains recognized within our portfolio of investments in the first quarter of 2021,” the press release stated.

The result also benefited from a $7.5 million increase in gains on equipment sales and a lower tax rate (-130 basis points) compared to the 2020 first quarter.

Knight-Swift raised its full-year adjusted EPS guidance to a range of $3.45 to $3.60, roughly 7% higher than the original guidance at the midpoint of the range. The new guide sits well ahead of the current consensus expectation, which is $3.40, but reflects the outperformance in nonoperating income in the quarter.

The company’s guidance assumes a mid-teen percentage increase in over-the-road contract rates as “over-the-road truckload demand is at unprecedented levels and expected to continue into 2022.”

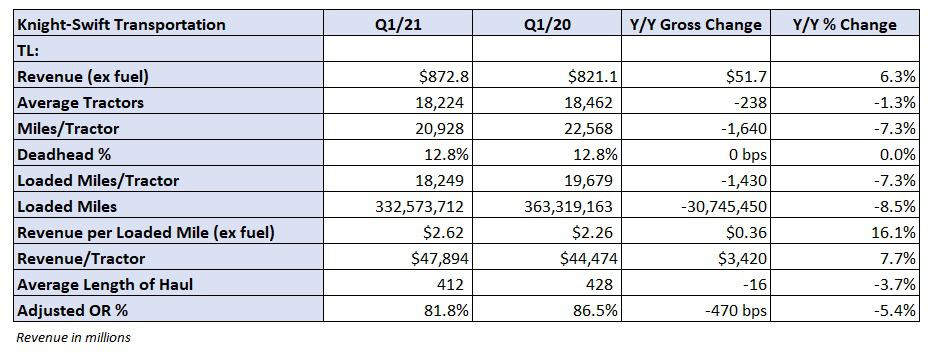

Knight-Swift’s trucking segment reported a 6% year-over-year increase in revenue, excluding fuel surcharges, at $873 million. Loaded miles per tractor declined 7% in part due to severe winter storms during the quarter, which was offset by a 16% increase in revenue per loaded mile (ex-fuel) to $2.62.

The division’s cost structure was fairly stable in the period. Salaries, wages and benefits as a percentage of revenue declined 120 bps year-over-year, which was largely offset by a 110 bp increase in purchased transportation.

“Our Trucking segment overcame inclement weather conditions and driver sourcing challenges during the quarter and improved average revenue per tractor by 7.7%, which resulted in a 470 basis point improvement in the adjusted operating ratio to 81.8% in the first quarter of 2021 from 86.5% in the first quarter of 2020,” the release continued.

The Swift fleet operated at a 78.5% adjusted OR with Knight operating at a 79% level.

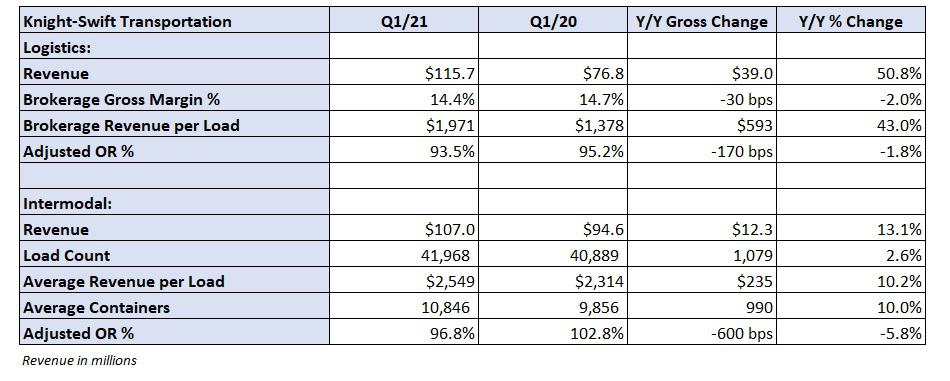

Brokerage revenue increased 51% year-over-year to $116 million as revenue per load surged 43% and loads increased just north of 5%. Gross margin in the division dipped 30 bps to 14.4%. The company’s power-only offering accounted for 25% of total brokerage volumes with its digital brokerage platform, Select, accounting for 20% of volumes.

Intermodal revenue increased 13% year-over-year with revenue per load, up 10%, driving the bulk of the increase. The division returned to a profit, posting a 96.8% adjusted OR.

“Despite weather and service disruptions during the first quarter of 2021, our intermodal segment achieved year-over-year improvements in operating results, and we anticipate ongoing improvement in the coming quarters,” the report read.

The company reiterated net capital expenditures of $450 million to $500 million in 2021, 22% higher than the 2020 investment at the midpoint. The bulk of the spend is slated for tractor and trailer replacement and improvements to its terminal network. Knight-Swift’s average tractor age increased to 2.3 years in the quarter from 2 years a year ago.

Knight-Swift ended the quarter with $853 million of available liquidity and net debt of $632 million, down $126 million from the end of 2020. The company generated $306 million in cash from operations, $262 million in free cash flow.

The company recently raised the dividend by 25% to 10 cents per share and repurchased $54 million of its stock in the quarter.

Shares of KNX are down more than 4% in early trading compared to the S&P 500, which is up 0.5%. The quality of the earnings beat and guidance raise, largely due to increases in nonoperating income, is likely the reason for the underperformance.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now