Never before has the humble ocean shipping container been this important to American business. If you can’t get one, you can’t move your international cargo — and supply has never been tighter. The cost of global trade is now contingent on how many containers exist, where they are and where they aren’t.

How many containers exist is controlled by China. Virtually every ocean shipping container in the world is built there.

Just three Chinese companies account for the majority of production, with Chinese factories now building more than 96% of the world’s dry cargo containers and 100% of the world’s refrigerated containers, according to U.K. consultancy Drewry.

Carl Bentzel of the Federal Maritime Commission (FMC) said earlier this month, “I am concerned that this equipment is controlled by a state-owned enterprise and that we’re completely reliant, and I have questions about whether or not there’s been market manipulation of what is potentially a monopoly.”

U.S. shippers are indeed reliant on equipment manufactured by a very small number of state-linked Chinese companies that are said to be actively managing capacity. But beyond expressing concern, there’s nothing the FMC or anyone else in America can do about it.

To understand how container manufacturing came to be dominated by so few Chinese entities and why it’s commercially unfeasible for this equipment to be built competitively at scale in the U.S., American Shipper interviewed John Fossey, head of container equipment and leasing research at Drewry.

The good news, according to Fossey, is that the current global equipment capacity crunch should ease as port congestion lessens and with China on track to manufacture a record number of containers this year.

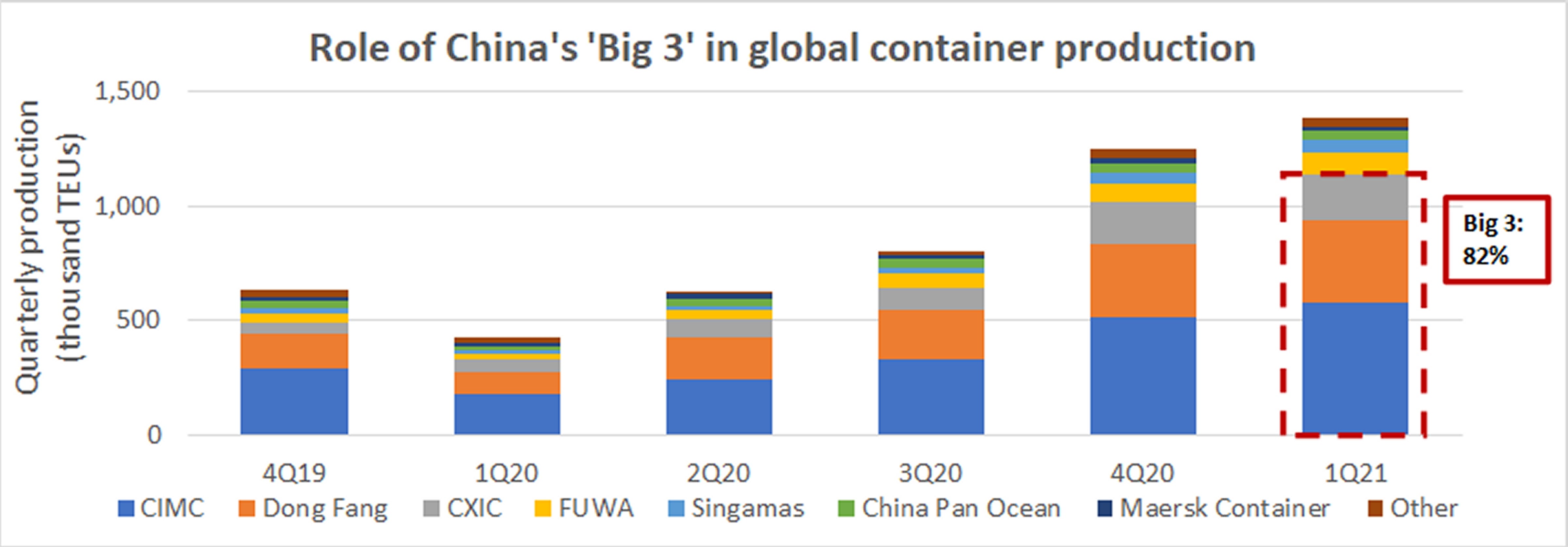

China’s ‘Big 3’

Container manufacturing migrated from South Korea to China in the 1990s. “That was very much supported by the Chinese government,” explained Fossey. “With Chinese manufacturing capacity increasing and their need to export everything, it made sense to build the containers there too.”

China grew its market share ever since and has been completely dominant for the past 15 years. In the first quarter of this year, the top three Chinese builders accounted for 82% of global container production, according to Drewry data.

China International Marine Containers (CIMC) produced 580,000 twenty-foot equivalent units (TEUs), accounting for a market share of 42%; Dong Fang International Containers, 358,000 TEUs (26%); and CXIC Group 200,000 TEUs (14%). Market shares were similar in full-year 2020, when a total of 3.1 million TEUs were produced, according to Drewry.

“There is significant state interest in the major companies, and strategies are to some extent controlled by the China Container Industry Association [CCIA],” said Fossey, who added, “I suppose you could argue that CIMC, which is far and away the largest, really runs the CCIA.”

‘Factories are behaving differently’

Between 2017 and early 2020, “container prices fell quite dramatically and manufacturers at best enjoyed wafer-thin margins, so the three main companies decided to try to support some kind of pricing for the dry freight boxes,” said Fossey. “They basically got together and said, ‘Look, we’re not going to produce these containers at a loss.’

“At the end of 2019 the price was just $1,650-$1,750 per TEU and they wanted a minimum of about $2,000. After the COVID shutdowns in the first quarter of 2020, they did start to raise their prices. And as we all know, with the strong consumer demand in the U.S. and Europe after that, prices just went through the roof. By the end of 2020 and into this year, we’ve seen prices at around $3,500.”

During a quarterly call earlier this year, Tim Page, interim president and CEO of container-equipment lessor CAI International (NYSE: CAI), asserted, “The factories are behaving differently than they have in the past. They don’t have any interest in increasing production at the expense of price. I think it’s a new dynamic in our industry. And I think it’s going to stick. They’re more focused on maintaining high container prices.”

Asked about Page’s comment, Fossey said, “That makes absolute sense. That’s exactly the strategy they’ve adopted. These factories could do two 12-hour shifts a day, but they don’t want to flood the market with boxes because they want to keep the price where it is now or perhaps slightly lower. They don’t want to ever get back down to $1,750 or $1,800.”

Chinese production is rising sharply

At a time when availability of container equipment is more important than ever to shippers, this setup might sound concerning from a U.S. trade perspective.

Analogous to foreign-flag liners that manage ship capacity to support freight pricing, Chinese container equipment manufacturers are reportedly managing production capacity to bolster new-box prices paid by liners and lessors. And unlike ocean carriers, Chinese equipment manufacturers are completely outside of the purview of U.S. regulators.

But Chinese production decisions are not responsible for container shortfalls in the U.S., maintained Fossey.

“I genuinely believe and Drewry research has demonstrated that, in principle, there are enough containers in operation today to satisfy global trade demand. The problem is that the containers are all in the wrong place, with all the congestion and the velocity of containers moving through the network being considerably slower.”

Meanwhile, Chinese production this year is very high — even if it’s not as high as it might be under a two-shift system. “They’ve gone from five days at 10 hours a day to six days at 10-11 hours a day,” said Fossey.

If the first four months of this year are any indication, Chinese factories are on pace to top 2018’s record of 4.4 million TEUs, equating to double-digit growth year on year.

Fossey believes that when port congestion eventually eases, the effective box supply will increase and demand for new production in China will pull back. He expects production “to slow down a little bit” in the second half versus the first.

Why can’t America compete?

A container seems like a relatively simple piece of equipment that could theoretically be built at a U.S. factory. In practice, however, a U.S.-built container could not compete for liner and lessor customers with a Chinese-built box.

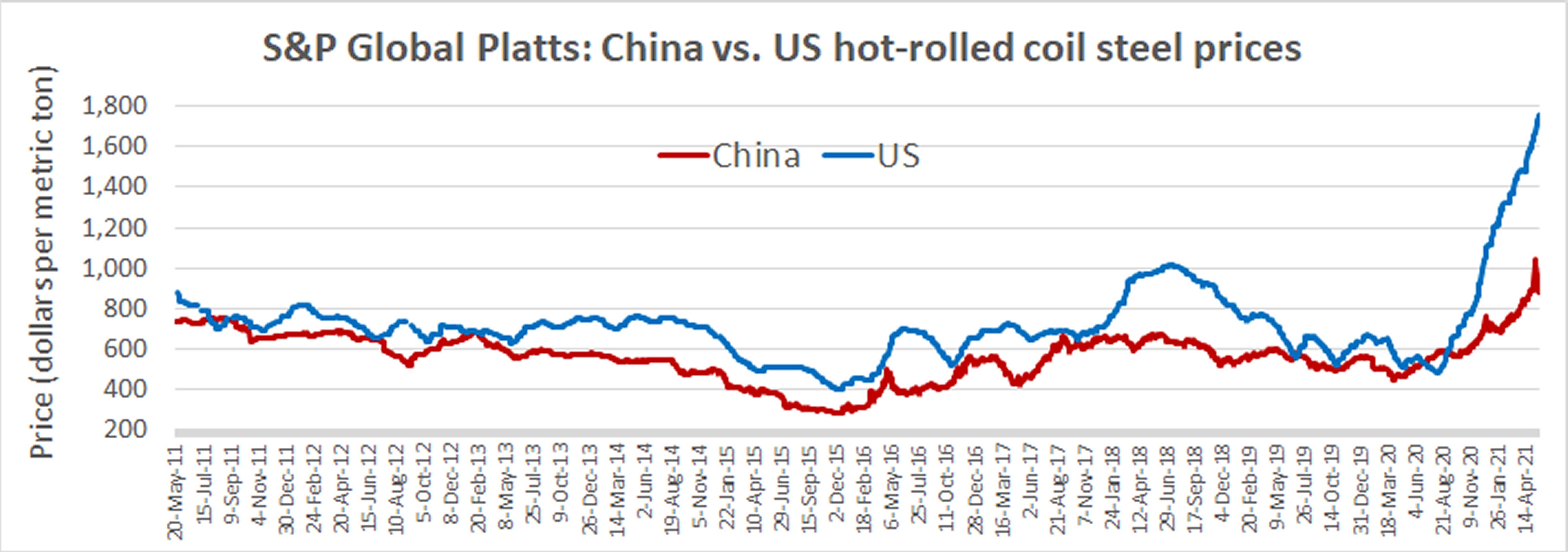

One issue is steel, the single most important input in the construction process. Drewry estimates that Corten (weathered) steel represents around 60% of the total cost of building a container.

According to data provided to American Shipper by S&P Global Platts, the price of U.S. hot-rolled coil (HRC) steel over the past decade has averaged 28% higher than Chinese HRC. More recently, the U.S. price has spiked to nearly double the price of HRC in China.

China’s other competitive advantages range from lower labor costs and higher government support to proximity to where refrigerated container machinery is produced.

“When you think about all the technology and investment they’ve made in plants and paint shops and drying facilities, it’s very difficult to see any other countries get to the same scale as China and have a competitive unit cost,” said Fossey.

There’s yet another advantage to building containers in China that’s particularly pivotal: lack of repositioning costs. “The liners and the lessors don’t have to spend huge amounts of money repositioning those containers to areas of demand. China is where the cargoes are being produced,” he said.

“If you’re a lessor, you want to send your containers out on your initial lease period straight into the carrier’s system with a load. You don’t want to be paying to reposition those boxes halfway around the world.”

Add it all up, said Fossey, and China “has the demand at its doorstep, it has the expertise, it has invested heavily in the sector, and it produces quality boxes at very competitive prices. If you compare building a container in China to anywhere else, it’s unbeatable.”

Click for more articles by Greg Miller

Related articles:

- California’s massive container-ship traffic jam is still really jammed

- No relief: Global container shortage likely to last until 2022

- US regulator probing China’s role in container shortage

- Flexport: Trans-Pacific deteriorating, brace for shipping ‘tsunami’

- ‘March madness’ at LA port amid ‘once in a lifetime’ surge

- Chinese factories won’t build enough boxes to save US shippers

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now