Truckload carrier Heartland Express reported another net loss on Tuesday, but again logged sequential operating improvement.

The North Liberty, Iowa-based company reported a headline net loss of $19.4 million, or 25 cents per share. However, the result included a $19 million impairment charge associated with its decision to integrate and rebrand the Contract Freighters, Inc. (CFI) fleet, which it acquired in 2022. Backing out the one-time charge moves the adjusted EPS line closer to a 6-cent loss, 2 cents better than the consensus estimate. (The adjusted loss was 5 cents per share when backing out deal-related amortization expenses.)

“We believe the investments made to improve our internal processes and systems along with the strategic decision to consolidate our two largest operating fleets of drivers into Heartland Express at the end of 2025, have and will continue to allow us to improve our operating results,” said CEO Mike Gerdin in a news release. “Further, we believe that this gives us the best probability for success and allows us to better capitalize on potential industry and market improvements in 2026.”

(Heartland does not host a quarterly call.)

The quarter had the benefit of $12.2 million in gains on equipment sales, more than double the year-ago period. That was approximately a 6-cent-per-share tailwind. The quarter marked 10 straight net losses, excluding one-time real estate gains.

Revenue of $179 million was down 26% year over year and $15 million below the consensus estimate.

(Heartland does not provide operating metrics for utilization and pricing.)

The company posted a 101.6% adjusted operating ratio in the quarter, 270 basis points worse y/y but 190 bps better than the third quarter. Heartland has reported sequential adjusted OR improvement in each of the past three quarters.

Heartland (NASDAQ: HTLD) now has all of its fleets operating on the same TMS. It has rebalanced and rightsized the network, removing unprofitable freight and excess real estate.

The company reiterated financial goals of profitably growing the topline (organically and through M&A), returning to low- to mid-80s ORs, and achieving a debt-free balance sheet.

Operating cash flows totaled $89 million in 2025, down from $144 million in 2024.

Heartland reduced net debt (inclusive of financing lease obligations) by $11 million in the fourth quarter to $141 million outstanding. It ended the year with $89 million available on an untapped revolving credit facility and was in compliance with financial covenants.

An average tractor age of 2.6 years remains elevated by Heartland’s historical standards.

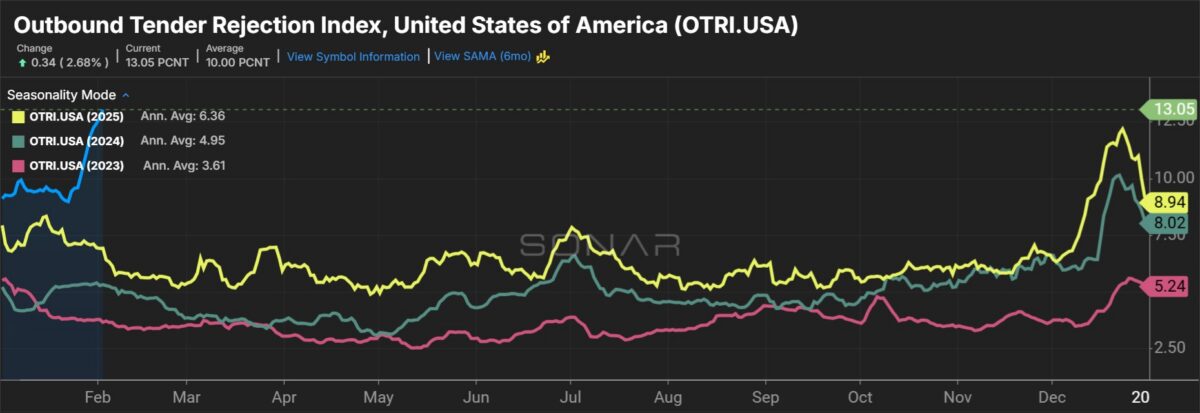

Gerdin noted “positive signs” as truck capacity is coming out of the market but said a material improvement is unlikely to occur “until some months later in 2026.”

“We are however seeing early trends of positive shifts in customer volume, certain rates, and increasing customer expectations which are a positive change from the last three years of operation.”

Shares of HTLD were up 2.9% at 1:46 p.m. EST on Tuesday compared to the S&P 500, which was down 1.4%. The stock is up 56% since the week prior to Thanksgiving when TL spot rates began to surge.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now