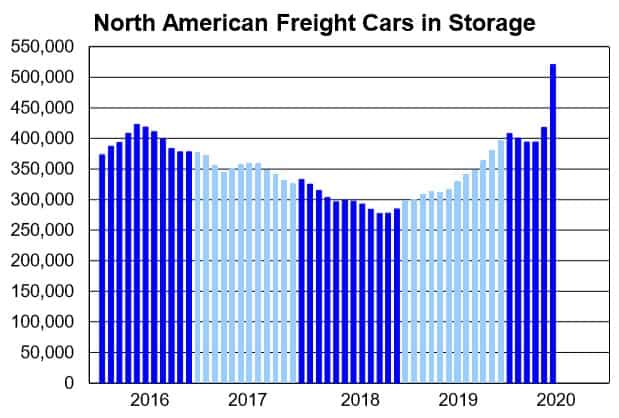

After hovering around the 400,000-unit mark all year, railcars in storage spiked 25% in May to 520,729. This was the one of many takeaways from the Association of American Railroads’ (AAR) June report.

As of June 1, 31.2% of the 1.67 million North American freight car fleet were in storage. The AAR considers a car in storage if it hasn’t hauled a load in the past 60 days and has moved empty since carrying its last load.

A soft industrial economy, exacerbated by COVID-19-related manufacturing shutdowns, has driven rail carloads materially lower. Through the week ending May 30, second-quarter 2020 Class I North American rail traffic is down nearly 20% year-over-year, following an almost 6% decline in the first quarter. Add in structural demand headwinds for coal and to a lesser degree steel and near-term structural headwinds in intermodal, it’s not hard to explain the spike in idled equipment.

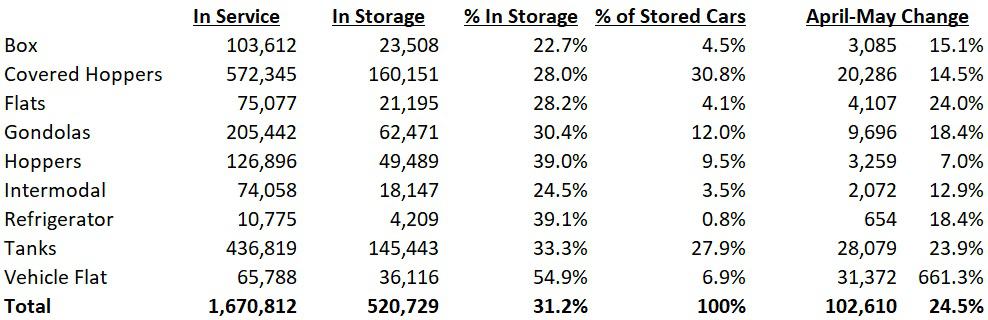

Cars in storage up across all commodity types

In total, 102,610 railcars were moved into storage in May. The increase was primarily driven by increases in stored vehicle flat cars (+31,372 units), tank cars (+28,079 units) and covered hoppers (+20,286).

The shutdown of the auto industry has resulted in 55% of the total vehicle railcar fleet being placed in storage. Thirty-nine percent of the refrigerator fleet (carrying food products, farm products and chemicals) is in storage, with a similar percentage of the hopper fleet (moving coal, metallic ores and nonmetallic minerals) being parked.

Covered hoppers (moving grain, chemicals and nonmetallic minerals) remain the largest car type in storage, representing 31% of all cars in storage and 28% of the covered hopper fleet.

Depressed oil and gas prices essentially pressed pause on the crude-by-rail story while shutdown mandates have dramatically curbed consumption at the pump. Tank cars (moving chemicals, petroleum and food products) accounted for the second most cars in storage during May, representing one-third of the tank fleet. North American petroleum and petroleum products traffic moved 33% lower year-over-year during the month.

Declines in intermodal traffic, down 14% year-over-year so far in the second quarter and almost double the first-quarter decline, have resulted in 25% of that fleet now being idle. Intermodal demand has been plagued by weaker inbound container volumes, excess truck capacity, lower spot rates and declines in diesel prices. Intermodal cars in storage increased 13% sequentially from April.

One highlight in recent weekly carload data is that the year-over-year decline in North American intermodal traffic eased in May, down 11.7% year-over-year compared to the 15.6% decline in April.

U.S. carloads fell 27.7% year-over-year in May, the biggest decline for any month on record dating back to 1989 and worse than the April decline of 25.2%. Excluding coal, U.S. carloads dropped 21.9% during May. All commodity types saw a decline during the month except for one: farm products excluding grain.

The report noted that “May was the worst month for U.S. coal carloads in history, breaking the record set in April.”

In addition to volume declines, precision scheduled railroading (PSR) initiatives, which are designed to improve asset utilization and reduce the number of railcars and locomotives needed, have sent a significant number of railcars into storage.

This is evident in network fluidity improvements reported by the Class I railroads. Train speeds have improved nearly 15% year-over-year on average thus far in the second quarter after improving 9% during the first quarter of 2020. Terminal dwell times are materially lower as well. Average dwell times are down 9% year-over-year quarter-to-date through the end of May after improving 10% during the first quarter.

While some have suggested that the improvement in these metrics has more to do with the precipitous declines in rail volumes, the diminished need for railcars is not currently being debated.

Weekly carloads declines appear to be improving. In the last week of May, total U.S. traffic was down only 17% year-over-year, an improvement from the four-week average of 20%.

Click for more FreightWaves articles by Todd Maiden.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now