Labor was the main talking point of J.B. Hunt Transport Services’ third-quarter earnings call with analysts Friday. Management from the Lowell, Arkansas-based transportation company said many of the nation’s supply chain obstacles are rooted in a shortage of workers.

“The thing that has been the most difficult for us to get eyes on is customer warehouse labor,” said J.B. Hunt (NASDAQ: JBHT) intermodal head Darren Field. “That’s where there is a significant bottleneck — our customers’ ability to unload the demand that they have.”

Earlier in the day, the company posted earnings per share of $1.88, which beat analysts’ estimates by 11 cents. The result was also 27 cents higher than the second quarter and 70 cents better than the year-ago period.

J.B. Hunt’s stock popped on the news. Shares of JBHT were 9.7% higher at 1:45 p.m. EDT Friday compared to the S&P 500, which was up 0.7%.

The company expects challenges throughout the transportation network to push peak season deeper into November and December, meaning inventory replenishment will be a favorable catalyst during the first quarter.

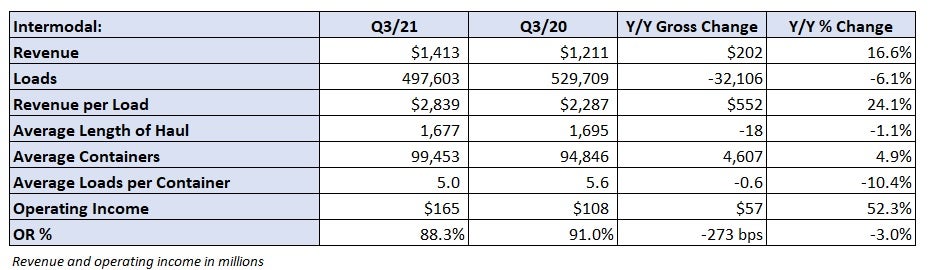

Labor headwinds limit strong intermodal performance

Delays in the time it takes warehouses to unload containers and get the equipment moving again was evident in the quarter. The company’s intermodal segment saw box turns fall to 5 times on average in the quarter versus 5.6x a year ago. J.B. Hunt’s boxes were turning 1.65 times each month during the second quarter. The rate was down to 1.62 this quarter.

In efforts to have customers flip boxes faster, J.B. Hunt began enforcing accessorial charges for excessive delays more stringently. However, Field said that the results of the initiative “have been mixed,” noting that the goal was to “move more volume and provide more capacity for customers, which was not the case in the quarter.”

Intermodal loads were 6% lower year-over-year during the third quarter but revenue increased 17% to $1.41 billion. A 24% increase in revenue per load, which was the combination of improved mix, higher rates and an increase in fuel surcharge revenue, was the reason.

Core price increases were strong, according to management, and covered cost inflation (operating costs were up 20% per load). Management wouldn’t provide details on how much the accessorial program influenced revenue per load. It did say that core price increases accelerated sequentially in the third quarter and outpaced the rate at which expenses increased.

In the third quarter, J.B. Hunt added 2,853 intermodal containers to its fleet of more than 102,000 units, part of a larger program to alleviate network congestion. In total, the company plans to take delivery of 12,000 containers by early 2022 with approximately 8,000 to 9,000 units entering the fleet by year end.

Field said it’s too early to provide intermodal rate commentary for 2022 as costs like driver pay and purchased transportation remain volatile.

He also said it was too soon to determine when box turns could improve.

“We’re focusing with our customers every single day on how to improve that number related to their actions that are influencing it. Certainly, our rail providers are moving somewhat slower than we would have anticipated,” Field said. “I would have said at the end of Q2 that I can’t imagine it getting worse, and you know what, it did.”

J.B. Hunt’s primary rail partners BNSF (NYSE: BRK.B) and Norfolk Southern (NYSE: NSC) saw dwell times increase 2% and 15%, respectively, while train speeds declined by 5% and 6%, respectively, during the quarter.

Even with the headwinds, the intermodal operating ratio improved 270 basis points to 88.3%.

Market share gains, double-digit growth in every segment

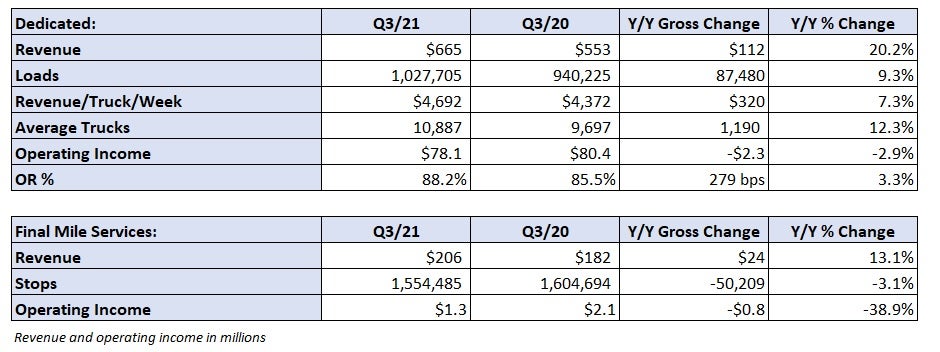

Dedicated revenue increased 20% year-over-year to $665 million as the average truck count increased 12% and revenue per truck climbed 7%. The division added 744 revenue-producing trucks sequentially in the quarter, which resulted in a spike in contract implementation costs. Increases in driver and non-driver compensation were headwinds as well. The OR eroded 280 bps to 88.2%.

Nick Hobbs, J.B. Hunt’s COO and president of contract services, said challenges finding workers are widespread.

“It’s across the board. It’s maintenance techs, it’s drivers. There’s going to be tremendous pressure on wages. I see that continuing on for quite some time, all throughout the supply chain,” Hobbs commented.

Similar contract startup headwinds were seen in the final-mile segment. Operating income was off 39% year-over-year to $1.3 million and well below the nearly $11 million recorded last quarter. In addition to the expense associated with onboarding new business, higher purchased transportation costs and lower volumes due to some customers struggling with product availability were obstacles.

Management said the company’s core legacy final-mile business was operating within its long-term margin goal of 4% to 8%.

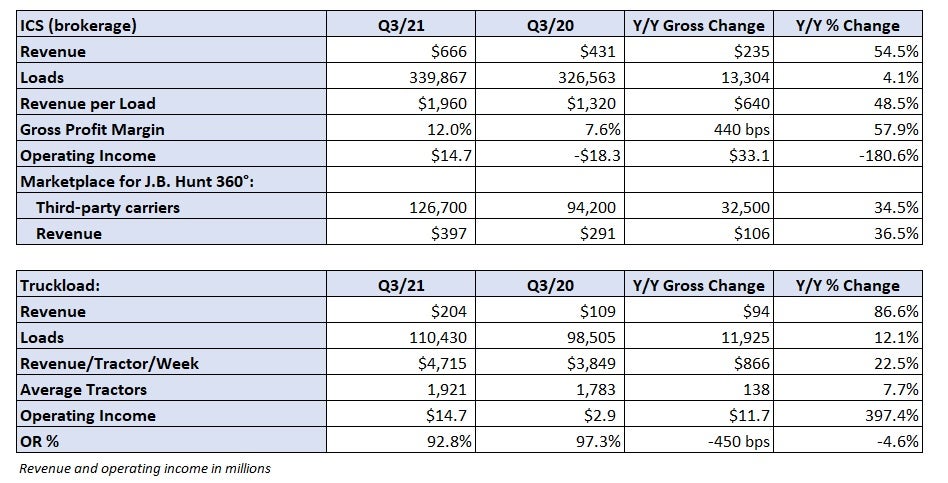

J.B. Hunt’s truckload division saw revenue increase 87% year-over-year to $204 million. Revenue per loaded mile including fuel was up 38% to $3.70, with rates among J.B. Hunt’s contractual customers increasing 29%.

This was the first quarter the division hit $200 million in revenue since 2007.

The company began scaling back truck capacity in the segment more than a decade ago in efforts to grow other offerings like dedicated. It has leaned on investments in drop-trailer pool 360box to grow revenue while allocating 60% fewer trucks to the division over the same time.

An additional 900 trailers were added in TL from the second to third quarters, which has the fleet approaching 10,000 units.

The brokerage segment recorded a 55% year-over-year revenue increase even though loads were only 4% higher. Revenue per load jumped 48% as rates continued to step higher. Operating income of $15 million was a turnaround from an $18 million loss booked a year ago.

“There will come a time when the congestion eases,” John Roberts, president and CEO, said. “We are going to stop very short of predicting when that will happen because, like you, we have no idea. But if somebody told me in the second half of ’22 things will loosen up a bit, I’m not going to be surprised, but at the same time we are going to have to wait and see.”

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now