The rate at which transportation capacity contracted increased in September, according to a supply chain survey released Tuesday.

For 16 consecutive months, capacity has been on the decline. The latest reading of the Logistics Managers’ Index (LMI) showed the capacity component of the dataset fell 330 basis points from August to 37.2% in the month.

“The Transportation Capacity Index remains historically low, indicating continued downward pressure,” the report read. “Further, our data indicates that the downward pressure on transportation capacity remains extremely strong for downstream firms in supply chain (downstream Transportation Capacity Index is only 30.2), indicating that companies are facing significant challenges in ramping up shipments for the holiday season.”

The LMI is a diffusion index wherein a reading above 50% indicates expansion and a reading below 50% indicates contraction.

Transportation capacity has been in the 30% range (“significant contraction”) for 12 of the last 14 months.

Survey respondents also lowered their expectations for future transportation capacity. While slightly in expansion territory at 52%, the 12-month forward-looking sentiment fell 480 bps from last month.

The overall LMI, which measures activity throughout various points in the supply chain, logged a 72.2% reading, still in “significant expansion” mode but a 160-bp decline from August. The index has been above the 70% threshold for eight straight months and 11 of the last 13. The two exceptions were “a function of inventories being sold off during Q4.”

“If there is a drop-off, it seems unlikely that it will come soon,” the report added. “Over 131 billion packages (approximately 4,000 per second) were delivered in 2020, volume is expected to increase in 2021 and be elevated well into 2022. Slowness exists at every level in the supply chain and catching up to demand will be no menial task.”

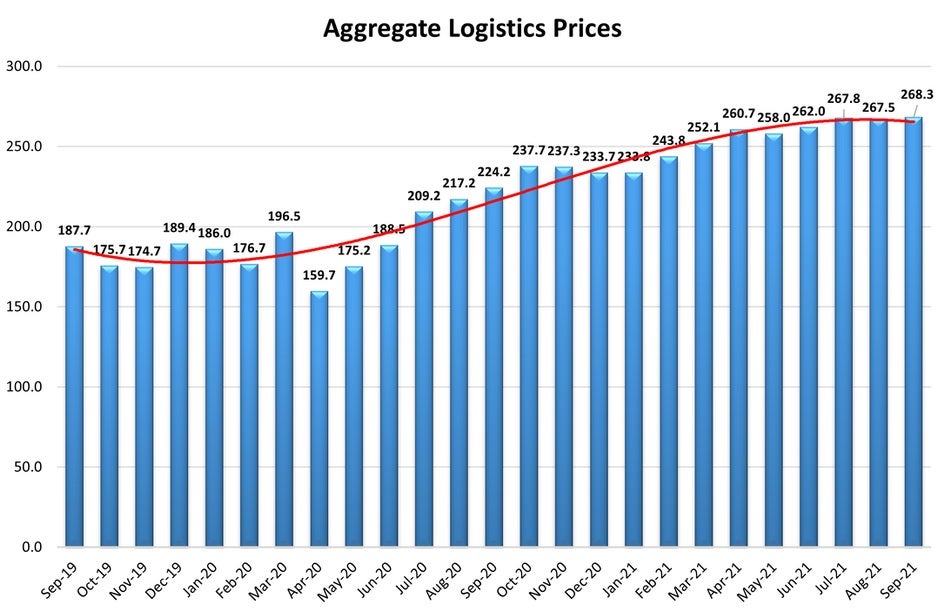

Transportation prices are soaring

The transportation prices subindex declined 130 bps to 92.4%. Consumer-facing companies reliant on capacity registered a 96.6% reading, which was the highest recording for any metric in the LMI’s history. The pricing index’s “astronomical rate” was the sixth report out of the last seven to register above 90%.

The aggregate logistics prices index, a combination of inventory, warehousing and transportation costs, reached an all-time high during the month as well.

“The continual increase in logistics costs continues to make the efficient, dependable movement of goods difficult for firms,” the report stated. “The fourth quarter is generally ‘crunch time’ in the logistics industry. However, the readings from January to September 2021 are the highest costs have ever been over any nine-month period in the history of the index.”

The future outlook for transportation prices logged a value of 86.9%, meaning rates are likely to “remain very strong” for at least another year.

Transportation utilization (69.5%) tightened further in the month, albeit at a rate 310 bps slower than August.

No room to store freight

Warehouse capacity (47.9%) remained in contraction territory but the reading was 880 bps higher than a month ago. Storage capacity has been on the decline for 13 consecutive months as “the warehousing crunch” has been “exacerbated by the slowness in transportation as firms have attempted to stock up ahead of time to stay ahead of potential supply delays.”

Warehouse pricing (89.3%) was up 130 bps, an all-time high. The dataset is up 18.8 percentage points year-over-year. The 12-month forward look for storage rates (87.9%) shows “respondents expect to be paying higher prices through the rest of the year and well into 2022.”

Inventory costs (86.6%) were up 20.1 percentage points from September 2020 and by a similar amount from the same month of 2019.

“Once again, we see that while the growth in overall inventories [58.6%] is slow due to high customer demand and slow delivery, the cost of storing goods continues to climb at a staggering pace – indicating that a high volume of goods is moving through supply chains at a high level of velocity.”

The LMI is a collaboration among Arizona State University, Colorado State University, Rochester Institute of Technology, Rutgers University and the University of Nevada, Reno, conducted in conjunction with the Council of Supply Chain Management Professionals.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now