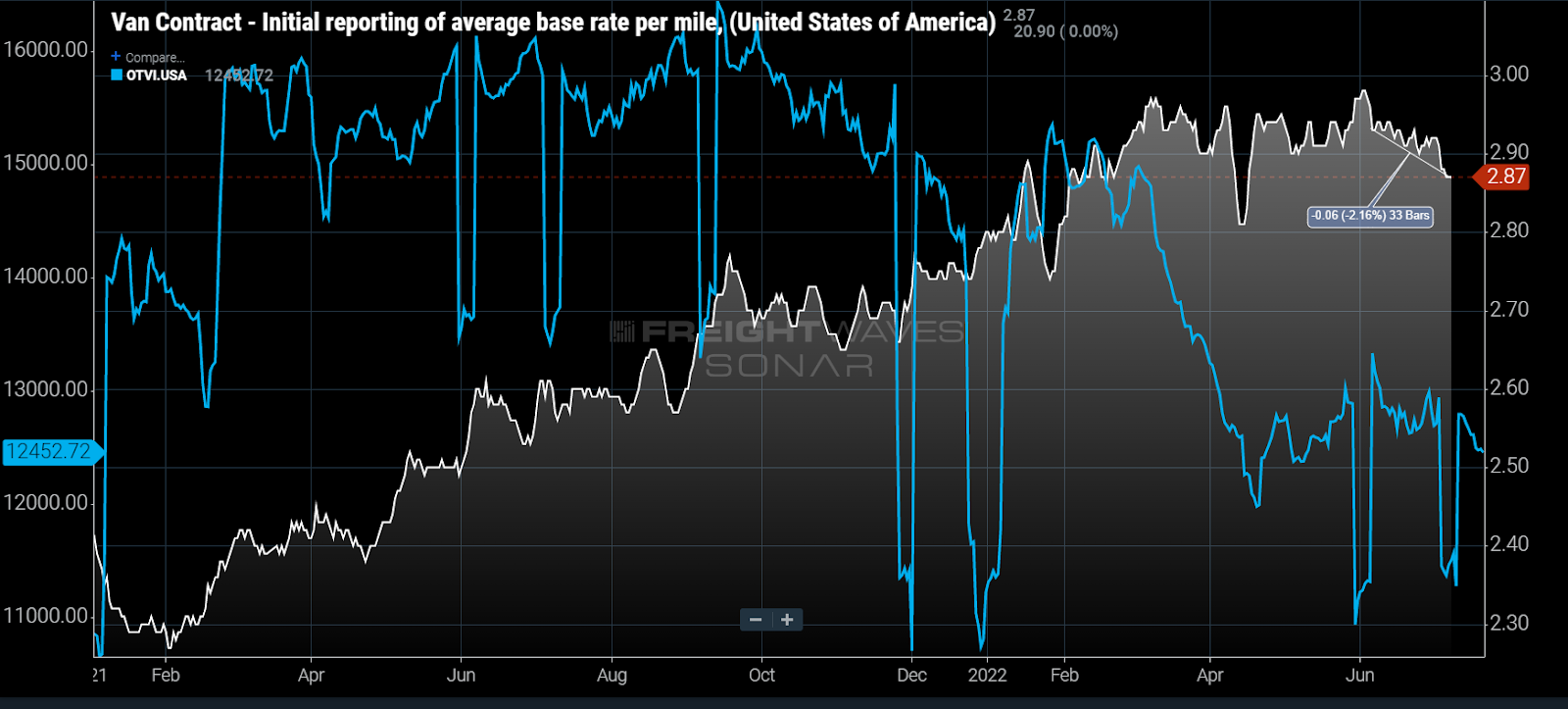

Chart of the Week: Van Contract Rates Initial Report, Outbound Tender Volume Index – USA SONAR: VCRPM1.USA, OTVI.USA

Truckload van contract rates have started to show early signs of contraction this July according to FreightWaves’ invoice data, which pulls from a database representing $20 billion worth of annual spend. Van contract rates (VCRPM1) have dropped over 2% since the start of July to a value of $2.87, which has broken the $2.90-per-mile threshold that has been in place since early March.

The dip in contract rates appears to be driven by a drop in demand for truckload capacity that has persisted through the summer. The Outbound Tender Volume Index (OTVI), which measures shippers’ electronic requests for truckload capacity at previously agreed upon rates, fell 20% from March 6 to April 21 this year and has maintained about an 18% annual decline through the summer.

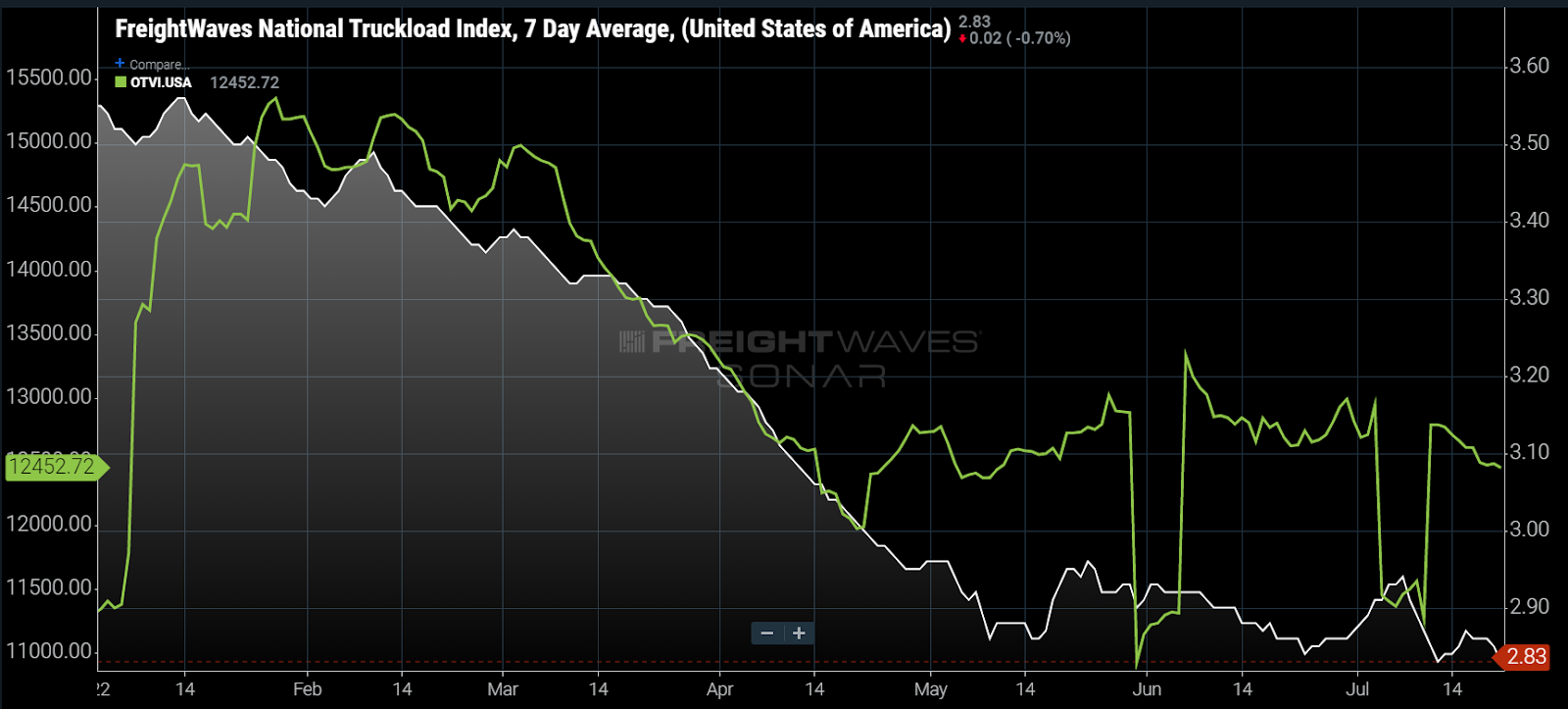

While the truckload spot market was immediately impacted by the drop in shipping activity, the contracted truckload environment has been largely unscathed.

The National Truckload Index (NTI), which measures the national average truckload spot rate for van loads, had been falling slowly since the first of the year but accelerated its descent about a week after the OTVI started its strong downward push. The NTI fell 6.3% from mid-January to mid-March and then 14% from mid-March to the middle of May.

It is important to note the differences between the spot market, which tends to get most of the attention, and the contracted freight market. The spot market represents roughly 15-25% of the total truckload volume in the U.S. Rates are negotiated with up to three-day lead times on average and are generally only good for a few days before expiring. Because of all of this, rates are much more volatile than their contracted counterparts.

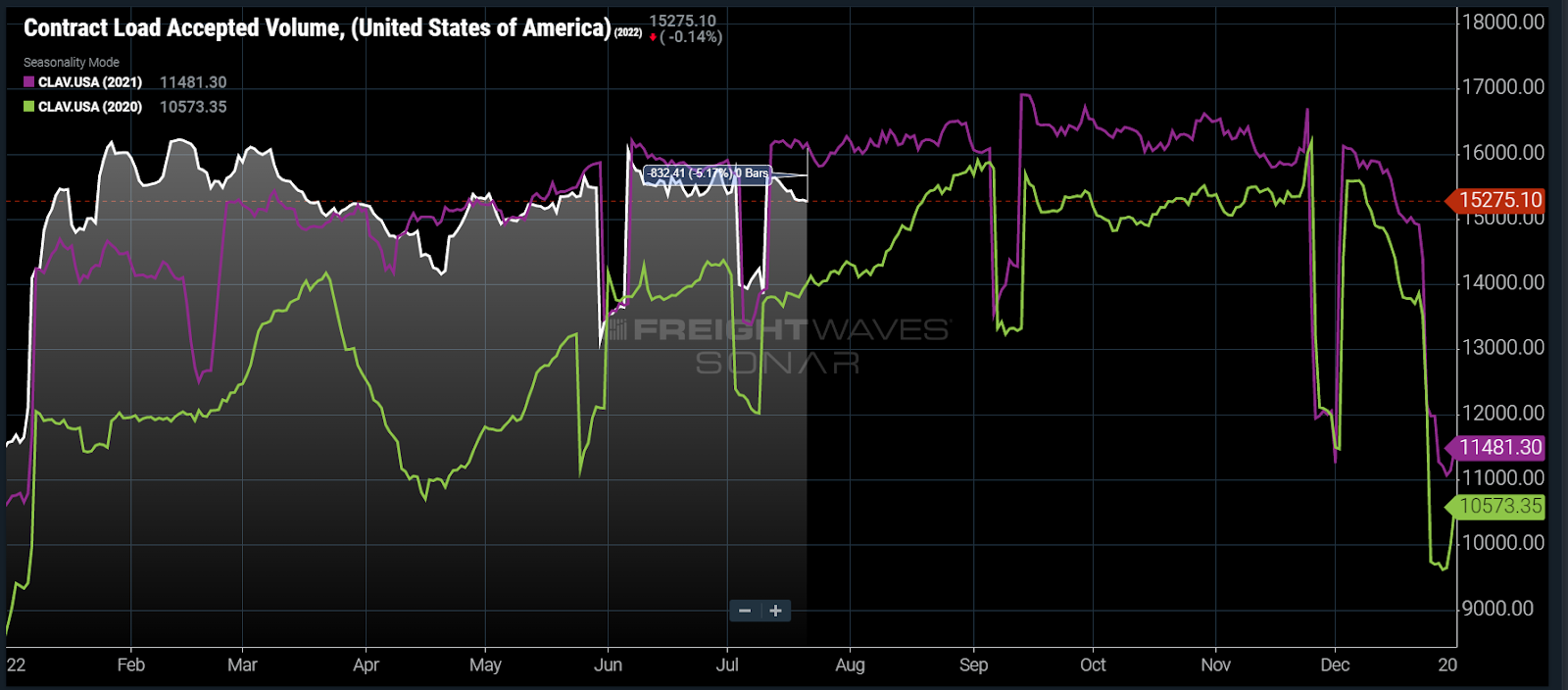

Until this month, contract volumes have not deteriorated significantly from a year-over-year (y/y) perspective. The Contract Load Accepted Volume Index (CLAV), which measures only accepted contract tenders, was above or even with 2021 levels through May. June was the first month in over two years that showed an annual contraction, averaging about 2% lower than the previous year.

Considering contract rates are up approximately 11% y/y, heavily contracted carriers have not yet felt a significant hit to revenue with only a marginal drop in volume. The CLAV is showing that things may be changing to start the third quarter.

Since July 1, the CLAV is showing an acceleration in annual decline, expanding from a 2% to 5% yearly differential. Pair this with the dip in contract rates and it shows the first signs of contract market deterioration since early 2020.

How far will rates fall?

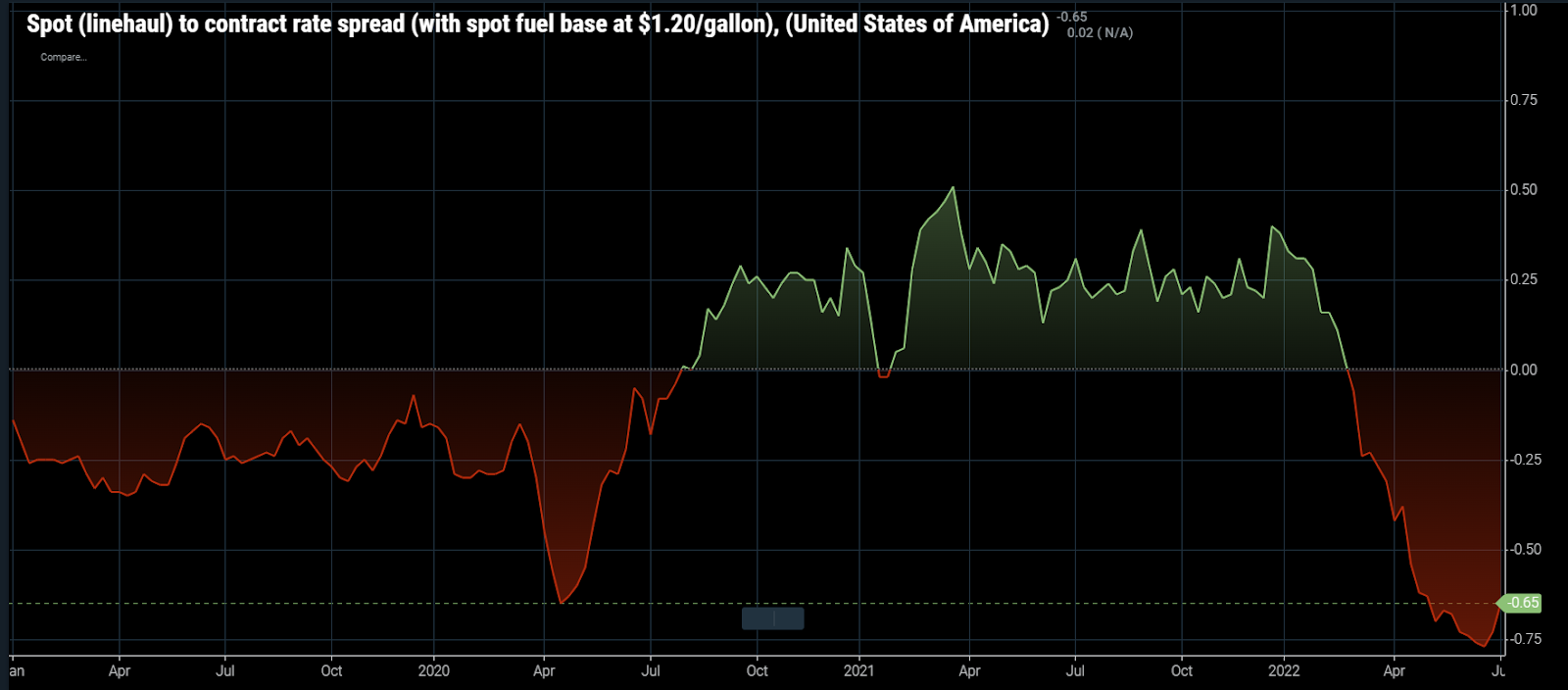

The current spread between contract and spot rates excluding fuel suggests that contract rates could fall another 14% if the spot market remains stable, but the timing is in question.

The spread between contract and spot rates has been lower than the early pandemic, which was historically low. That is starting to correct as contract rates fall.

Contract rates declined about 4-5% from late 2018 to early 2020 after gaining 16% from 2017. The point is that contract rates increase at a much faster rate than they decline and a quick contraction will probably not occur, but the current trend suggests that they will fall further.

J.B. Hunt’s newly appointed president, Shelley Simpson, stated, “We’re having a seasonally normal July,” which may have sounded like a positive. For those who know trucking, July is a slower month compared to June and this may have been a veiled comment about what is to come.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

To request a SONAR demo, click here.

Chris Kenney

Excellent article, data is suggesting economic forecaster’s ignore another sign of recession