Management from J.B. Hunt Transport Services (NASDAQ: JBHT) had a “cautious tone” on the company’s second-quarter earnings conference call with analysts when discussing expectations for the remainder of the year. The lack of an update on future freight demand largely stems from uncertainty on the part of its shipper client base. Accelerating frequency in COVID-19 cases and the fear of another wave of the virus has limited visibility into the third quarter and beyond.

The Lowell, Arkansas-based company reported earnings per share of $1.14, well ahead of consensus estimates in the mid-80-cent range.

Total revenue declined 5% year-over-year to $2.15 billion, down only 0.5% excluding fuel surcharge revenue. Operating income fell 9% to $175 million, with increased purchased transportation costs, investments in technology and roughly $11 million in COVID-19-related operating costs providing headwinds. “Uncollectible customer accounts” totaling $4.6 million resulted in increased charges during the quarter as well.

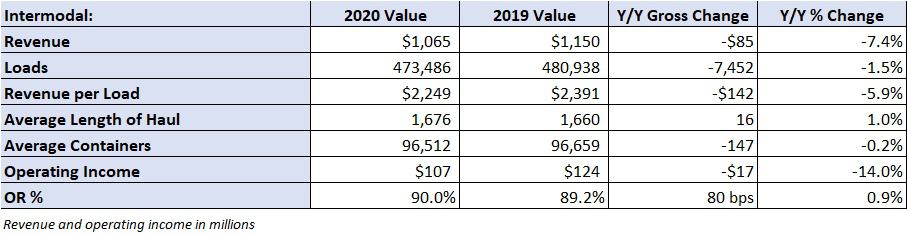

Intermodal benefits from market share gains

Intermodal volumes, down only 1.5% year-over-year, improved as the quarter progressed. Loads were down 6% in April, down 4% in May and up 5% in June. By comparison, the domestic intermodal industry saw volumes decline in the high-single-digit range during the quarter. The much-better-than-feared result was in part due to market share gains achieved in 2019.

Network imbalance remains as transcontinental loads were up 3% and eastern volumes fell 7%. Management said they see the potential for more empty container movements in the third quarter as they rebalance equipment. Loads per container, or box turns, declined 1.4% year-over-year and 3.7% sequentially from the first quarter.

Revenue per load declined 6% year-over-year, basically flat excluding fuel. Management said 80% of its intermodal contracts have been priced for the year. Pricing has actually moved lower, but an improved freight mix has helped keep revenue per load flat. The new bid cycle starts in October.

The company’s intermodal operating ratio (OR) saw 80 basis points of degradation year-over-year to 90%. OR, operating costs expressed as a percentage of revenue, is the inverse of operating margin. Moving empty containers to the West Coast to balance the network will result in higher costs during the third quarter. Also, the year-over-year volume comparisons get tougher in the back half of 2020 given the company’s success taking intermodal market share over the last four quarters. The long-term operating margin goal for the intermodal division remains at 11% to 13%.

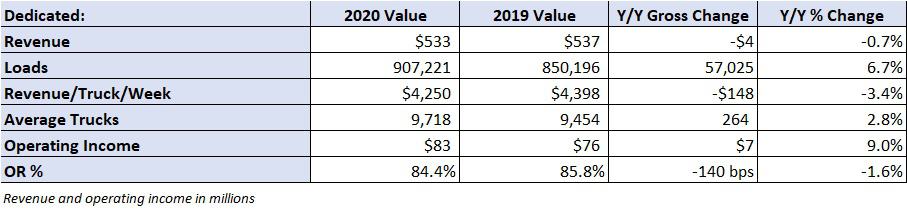

Dedicated the star again

The dedicated division was the star again as results came in ahead of management’s expectations. Revenue was down less than 1% year-over-year at $533 million. Loads improved nearly 7% in the period with revenue per truck per week declining 3% (flat excluding fuel). This was better than management’s original guidance, which cautioned that loads could be flat sequentially from the first quarter, implying a year-over-year decline.

The division’s OR improved 140 basis points year-over-year to 84.4%. Management said driver turnover has been historically low the past few months. Also, lower travel and entertainment expenses and safety-related costs provided tailwinds.

Management still expects to add 600 to 800 trucks to the dedicated fleet this year with 130 being added in the second quarter. The long-term expectation is for dedicated margins to be in the 11% to 13% range. Asked why that goal wouldn’t be higher with the better than 15% performance in the quarter, management pointed to favorable conditions — diminished traffic, improved transit times and lower liability claims — associated with COVID-19 restrictions that lowered costs.

Brokerage woes continue

J.B. Hunt’s brokerage division reported a 9% decline in revenue with loads down 11% and a 2% improvement in revenue per load. Pressed on the lack of load growth, management said the unit has been successful taking share in committed contractual business and that reduced spot transactions weighed on total brokerage loads. Contractual loads accounted for 71% of total load volume in the quarter.

The unit reported an operating loss of $13.1 million. Management described the brokerage market as “difficult” with margins that are “unsustainable.” They said the start of the quarter was the high mark for margins with June providing the low end. The market has further tightened into July. As truck capacity has tightened, previously awarded contractual freight is being rejected by carriers and coming back to the market to be rebid.

Marketplace for J.B Hunt 360° continues to see double-digit growth in all of the key metrics like load searching, quoting and acceptance. Brokerage revenue of $229 million was executed on the platform in the quarter, up $7 million from the prior-year period. The platform’s carrier tractor count increased almost 20% year-over-year to 717,700 units.

Management is still calling for the division to be profitable in the back half of 2021. They believe scaling the business from current levels will be the key to profitability for the unit. Future incremental loads will be more profitable as some cost buckets will remain flat moving forward.

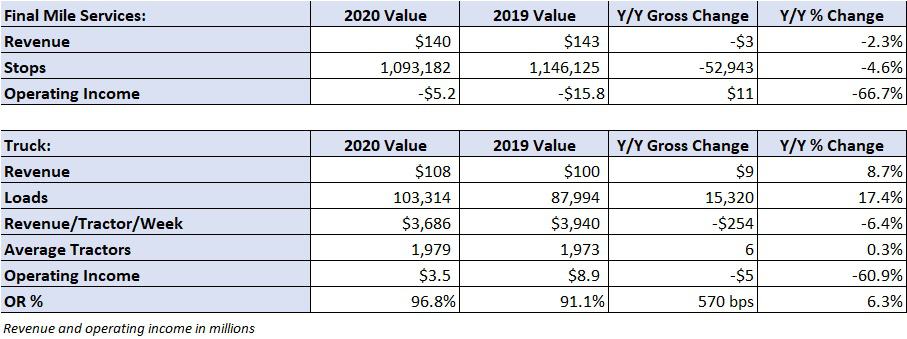

Final mile and truck

Final mile recorded a $5.2 million loss in the period as key retail segments were under pressure and the unit’s furniture business was off 30%. The segment is expected to be profitable in the third quarter.

The truck division reported a 17% year-over-year increase in loads with revenue per truck per week declining 6%. Revenue per loaded mile excluding fuel surcharges declined 7% from the year-ago period, and contractual rates were down approximately 5%.

J.B. Hunt will continue to preserve cash in light of uncertainty in the freight markets.

The company recorded capital expenditures (capex) of $265 million in the first half of 2020 compared to $475 million for the first half of 2019. The company ended the period with $275 million in cash and a debt-to-earnings before interest, taxes, depreciation and amortization (EBITDA) ratio of 1x.

Shares of JBHT are up 1.7% in after-hours trading.

Click for more FreightWaves articles by Todd Maiden.

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post • Chicago, IL Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now