Container-liner schedules are about to provide a telling clue on U.S. cargo demand.

Arrival schedules for May and June are set. U.S. ports will see double-digit declines in inbound capacity. Whether carriers will keep “blanking” (canceling) sailings on the same scale into the third quarter remains unknown — but not for much longer.

If mass cancellations extend into July at elevated May-June levels, it means that carriers are not receiving enough bookings from shippers, implying a weak recovery after social distancing restrictions are lifted. If carriers move back in the direction of pre-coronavirus scheduling levels, it’s a positive signal on demand.

“For the month of July, we’re at 10% cancellations, while May and June are at 19% and 18%, respectively,” said Simon Sundboell, founder and CEO of Copenhagen-based eeSea, a platform that maps container-industry schedules.

Given transit times and the need to provide pre-notification to shippers, Sundboell told FreightWaves that “the latest notice for blank sailings with arrivals into the U.S. in early July would be around mid-May to early June.” In other words, the scope of July cancellations will be revealed over the next few weeks.

Positive signals

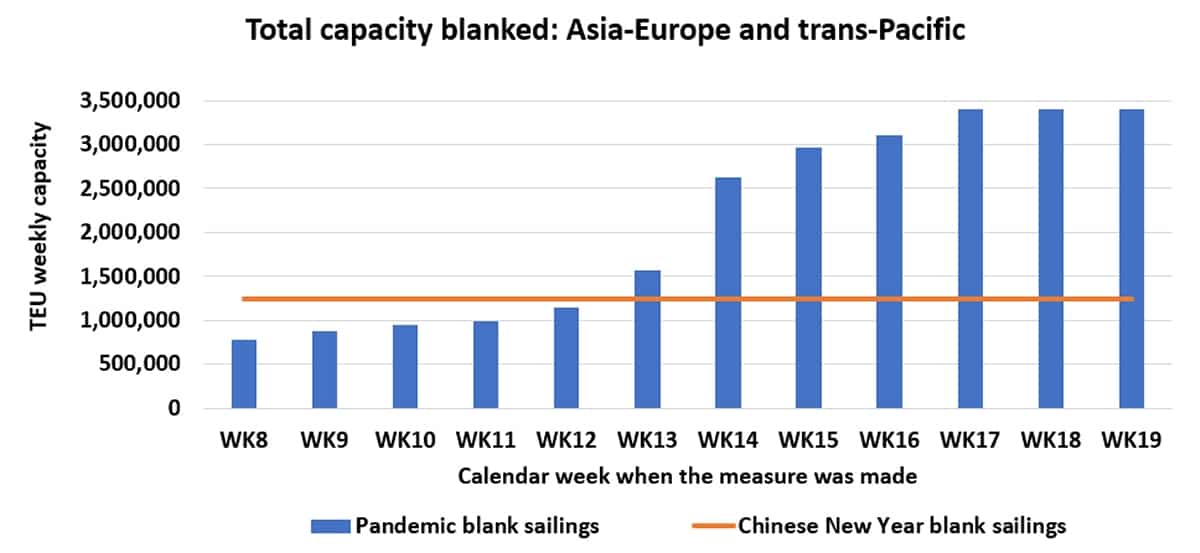

The good news is that blank-sailing announcements have been waning.

According to Alan Murphy, CEO of Copenhagen-based Sea-Intelligence, “Over the last week, carriers have only announced an additional six blank sailings across the main deep-sea trades, which clearly shows that we have reached a plateau, where carriers are now only blanking very few additional sailings, and for the moment are satisfied that the currently announced blank-sailings program is sufficient to underpin the freight rate levels.”

Looking at second-quarter fallout, Murphy said that the Asia-North America West Coast cancellations are hitting Prince Rupert, Canada and Long Beach, California the hardest, “with both ports seeing a 20-25% reduction in port calls.”

In the U.S. East Coast market, which is served both directly as well as by Caribbean transshipment terminals, Sea-Intelligence sees the greatest blank-sailing impact befalling the transshipment hub in Freeport, Bahamas. “Carriers are clearly preferring direct cargo under the circumstances,” noted Murphy.

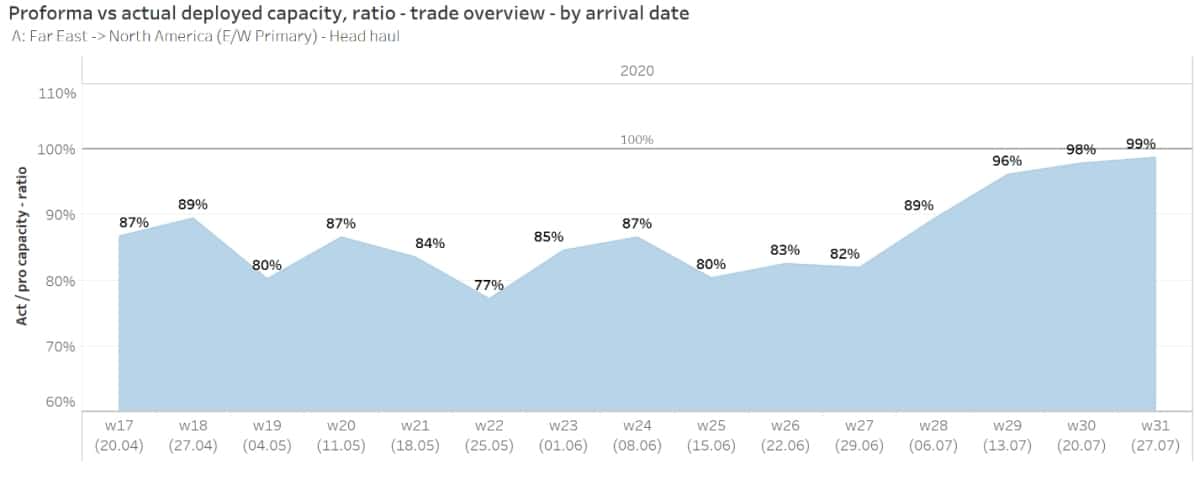

The data from eeSea reveals how the impact of blank sailings will play out for U.S. ports on a weekly basis across May and June.

This month, inbound container-ship capacity from Asia will be down the most, by 23%, during the week of May 25. Next month, capacity will be reduced the most, by 20%, in the week of June 16.

The slot utilization of the non-cancelled sailings is yet another important indicator. If, for example, 20% of the current week’s arrivals are canceled and the slot utilization on the remaining 80% is actually down versus previous levels, it would imply increased blank sailings ahead.

But utilization is not falling, according to Nerijus Poskus, global head of ocean freight at Flexport, a San Francisco-based digital freight forwarder and customs broker. “Most sailings are very full and rolling cargo,” he told FreightWaves.

“Premium [ocean] products are gaining even more share from air,” said Poskus, who reported that “two extra loaders were deployed on the trans-Pacific eastbound to deal with surging demand.” An extra loader is an unscheduled extra sailing, the opposite of a blank sailing.

Lag effect on import volumes

Sailing cancellations to U.S. ports inherently limit the capacity of arriving cargo ships, and by extension, U.S. imports. However, there are lag effects in terms of how ocean schedule changes translate into the number of import containers on roads and rail.

After a ship arrives, a box in a premium service with priority discharge may get from the ship to the customs gate in a day, but it could take three to five days on a non-premium service. And containers could be in the yard for weeks prior to passing through customs if the consignee doesn’t pick up the box promptly (something that is expected to be commonplace amid coronavirus shutdowns). Even after a customs declaration is submitted, it can take another four to five days before it shows up in customs data platforms.

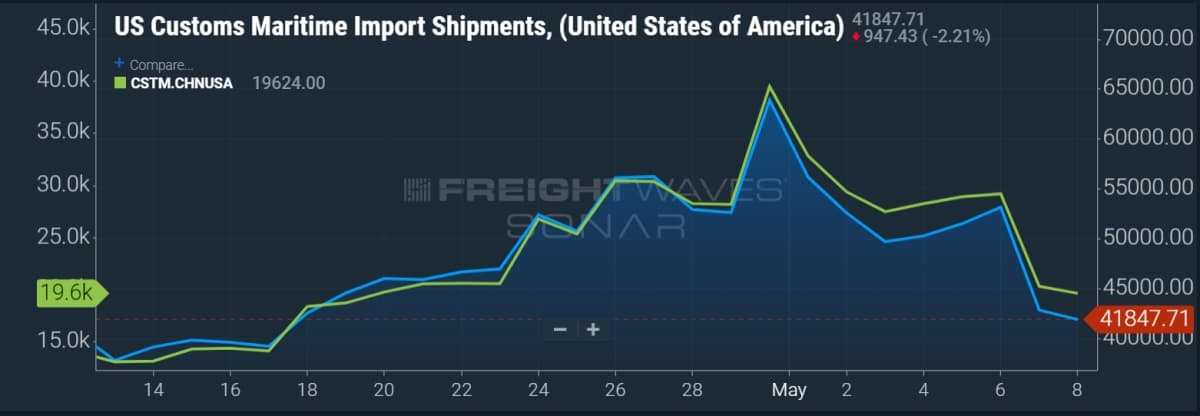

The number of customs filings (SONAR: CSTM.USA) surged in late April as cargo loaded just after the end of the China lockdown finally passed through the customs system (after being unloaded from ships that arrived at the U.S. docks earlier in April). The blank sailings are now pushing the customs numbers back down sharply, albeit with a lag effect that should make the decline even more pronounced by the end of the month.

The data also shows a continued very tight correlation between U.S. countrywide customs maritime import shipments and those specifically from China, confirming just how intertwined the two countries remain.

Freight rates stay firm

Ocean carriers cancelled so many sailings in May and June because they needed to prop up freight rates. If they allow rates to fall at a time of depressed volumes, they will face heightened insolvency risk.

So far, the carriers are succeeding on the rate front.

The price to ship a forty-foot equivalent unit container on the mainline routes is tracked by the Freightos Baltic Daily Index. On a global level (SONAR: FBXD.GLBL), rates are up 8% year-on-year. Rates from Asia to the U.S. West Coast (SONAR.FBXD.CNAW) are up 15% and rates to the East Coast (SONAR.FBXD.CNAE) are down 4%. Click for more FreightWaves/American Shipper articles by Greg Miller