This week’s FreightWaves Supply Chain Pricing Power Index: 30 (Shippers)

Last week’s FreightWaves Supply Chain Pricing Power Index: 30 (Shippers)

Three-month FreightWaves Supply Chain Pricing Power Index Outlook: 20 (Shippers)

The FreightWaves Supply Chain Pricing Power Index uses the analytics and data in FreightWaves SONAR to analyze the market and estimate the negotiating power for rates between shippers and carriers.

This week’s Pricing Power Index is based on the following indicators:

Are glasses half-empty or rose-tinted?

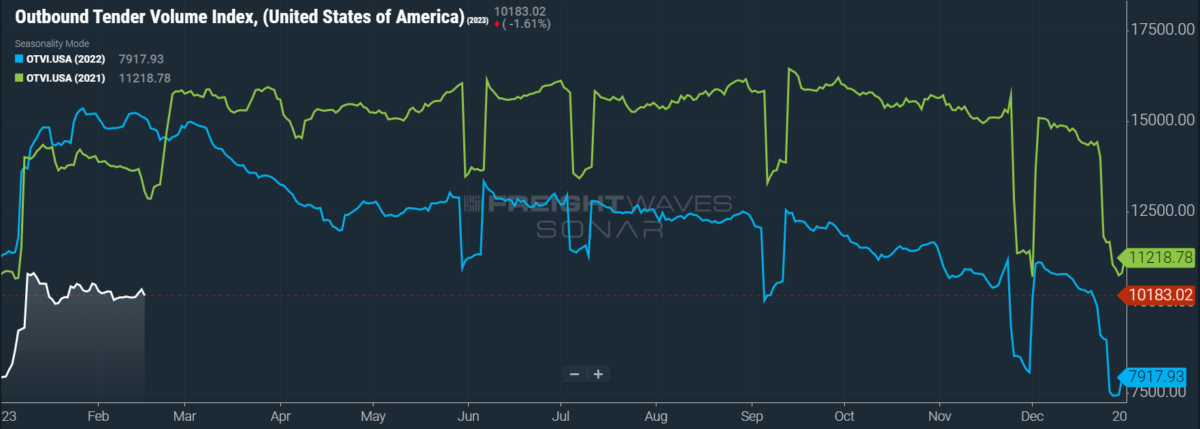

Strangely enough, tender volumes are abiding by seasonal trends. The first quarter of 2022 was unusually active as shippers tried to get ahead of disruptions to capacity, which historically tightens in the spring. Of course, the bottom began to fall out in March, kick-starting a downward trend that persisted throughout the year. Thus far into 2023, freight demand leveled out and is now beginning to pick up steam slightly. While headwinds to future demand have not disappeared, shippers are supplying markets with volumes on a steady basis — especially relative to the volatility of the past three years.

SONAR: OTVI.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

This week, the Outbound Tender Volume Index (OTVI), which measures national freight demand by shippers’ request for capacity, rose 0.53% on a week-over-week (w/w) basis. On a year-over-year (y/y) basis, OTVI is down 32.2%, although such y/y comparisons can be colored by significant shifts in tender rejections. OTVI, which includes both accepted and rejected tenders, can be artificially inflated by an uptick in the Outbound Tender Reject Index (OTRI).

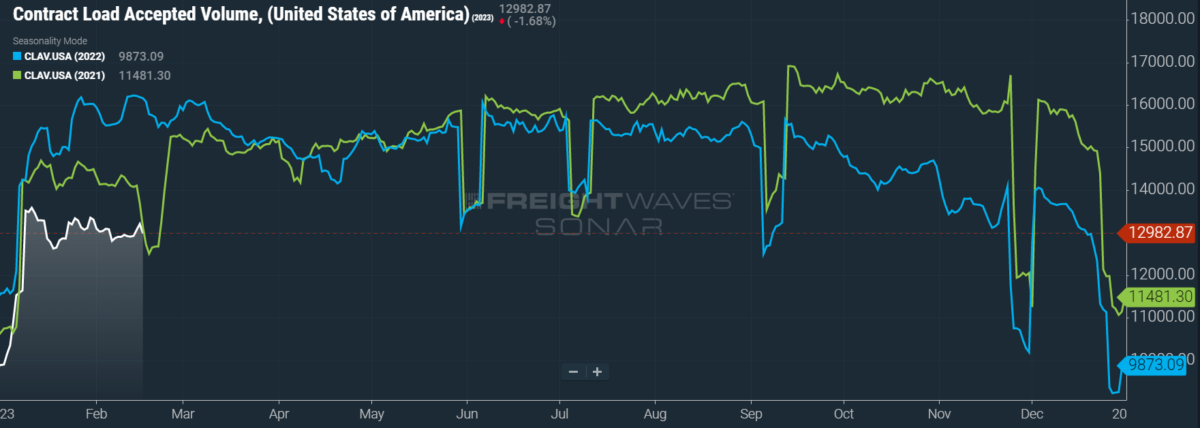

SONAR: CLAV.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

Contract Load Accepted Volumes (CLAV) is an index that measures accepted load volumes moving under contracted agreements. In short, it is similar to OTVI but without the rejected tenders. Looking at accepted tender volumes, we see a rise of 0.62% w/w as well as a fall of 19.6% y/y. This y/y difference confirms that actual cracks in freight demand — and not merely OTRI’s y/y decline — are driving OTVI lower.

For clarity’s sake, that volume levels are underperforming against 2022 is more telling about that year’s unique bull run than about current trends. CLAV has been firmly in between the highs of 2021-22 and the lows of 2019-20. Comparisons should impress more easily against 2020 and ’21 soon, since the former year saw markets rocked by lockdowns early in the pandemic and the latter year suffered a severe cold snap that shut down freight activity for a spell. So, although I have been quite bearish for quite some time, it is important not to lean into overblown despair. At the same time that tender volumes are remaining constant, however, carriers — both large and small — are still suffering from the excess of capacity (discussed below).

Supporting this view is a recent report from Cass Information Systems stating that shipment levels in January, which were helped by “mild weather and improving auto production,” were flat with December on a seasonally adjusted basis. Per Cass, shipments were also up 4.3% y/y in January, though the report stresses that the omicron outbreak in January ’22 made for easy comps. Given that CLAV was down 14% y/y in January, it is worth noting that FTL volumes contribute roughly half of Cass’ shipment index, which also accounts for LTL and intermodal volumes.

On a related note, Cass also observes a growing strength in the truckload sector’s market share, as shippers have increasingly switched modes from LTL and rail. Cass ultimately forecasts that shipments will be flat throughout the quarter on a seasonal basis. Uber Freight, on the other hand, is less optimistic. It predicts that the “spot market recession” of 2022 will snowball into a “broad-based volume recession” in the first half of 2023, given the weaknesses seen in imports, manufacturing output and retail sales. Uber Freight does, however, allow for the possibility of markets tightening in the back half of the year.

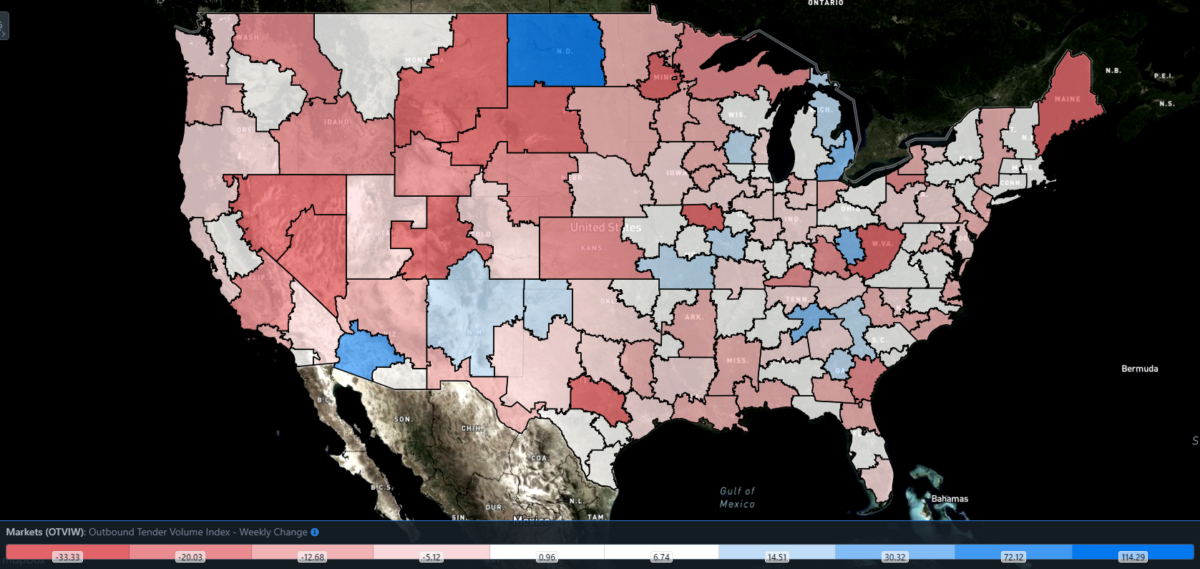

SONAR: Outbound Tender Volume Index – Weekly Change (OTVIW).

To learn more about FreightWaves SONAR, click here.

Of the 135 total markets, 58 reported weekly increases in tender volume, with mostly modest gains in freight demand.

Given that Cass cited “improving auto production” as a tailwind for current truckload volumes, it should come as little surprise that Detroit — also known as Motor City — is benefiting from gains in freight demand. Detroit’s local OTVI rose 30.3% w/w, the largest such increase among major markets. Despite these hopeful trends, domestic auto production has yet to recover fully from the pandemic and remains well below the highs of the mid-90s.

By mode: Van and reefer volumes alike are underperforming against the overall OTVI this week, implying that the market’s current positive w/w performance stems from strength in other modes, like flatbeds. The Van Outbound Tender Volume Index (VOTVI) is the lesser of the two evils, down only 0.33% w/w. Recently published retail sales data from January was incredibly strong across the board, with a healthy mix of spending on goods and services. Some of the weaker categories, however, included home improvement, electronics and appliance stores — all of which signal consumer-driven freight demand.

Meanwhile, the Reefer Outbound Tender Volume Index (ROTVI) is not much worse, sliding 0.51% w/w. As mentioned several times in this column, ROTVI has suffered from milder-than-usual weather this season, leading shippers without the need to insulate their temperature-sensitive freight in reefers. That said, produce season is right around the corner, which should offer some measure of relief to reefer carriers in the coming months.

Layoffs start to rock a sinking ship

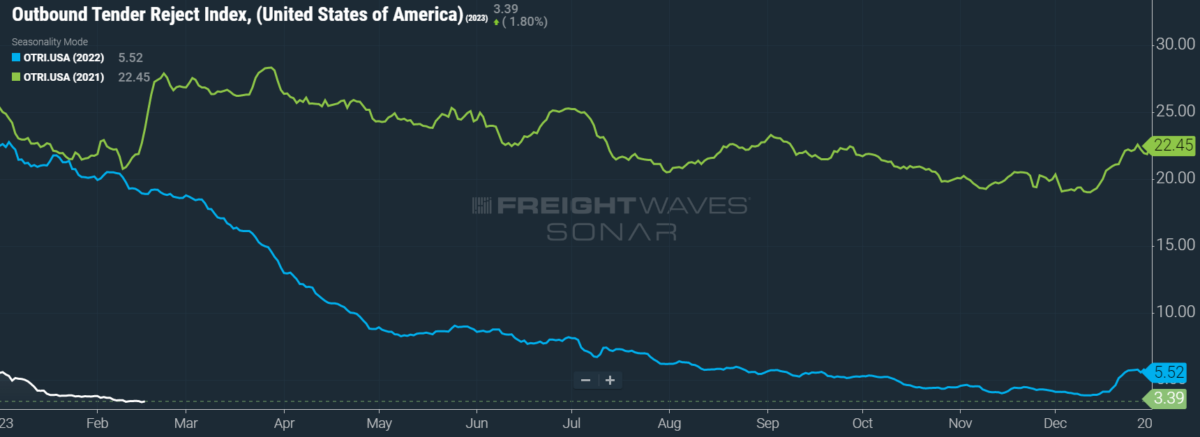

Until recently, I have excepted OTRI’s all-time low of 2.57% from comparisons to the present day. This low, I argued, was reached during the incredible circumstances of April 2020, when the entire Western world ground to a screeching halt during the onset of the COVID-19 pandemic. A better floor, I claimed, would be August 2019’s low of 3.78%, since it was achieved simply by cyclical market factors that led to an industrywide recession.

In a broad sense, there is not a great deal of difference between 2.57% and 3.78% in terms of market health — both numbers point to a critical situation for carriers. What the difference does signify, however, is the relative pain of these carriers. There were some that scraped through the previous trucking recession only to be taken out by the pandemic. When looking at these figures, carriers might reflect on how they functioned during these previous lows for a window into what lies in store.

SONAR: OTRI.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

Over the past week, OTRI, which measures relative capacity in the market, fell to 3.39% after an earlier dip to 3.33%, a change of 8 basis points (bps) from the week before. OTRI is now 1,549 bps below year-ago levels.

Convoy, a digital freight platform, announced a new service for its shipper customers that seeks to offer the stability of contract freight while retaining the flexible scaling of spot freight. The service, known as Dedicated On Demand, enables shippers to set an estimate of how much capacity is needed over a set period like traditional freight contracts. Unlike traditional contracts, the bid cycle is much shorter and can allow for surge capacity without the need to delve into the often-volatile spot market.

This announcement was marred, however, by the news that Convoy would shutter its Atlanta office and lay off an undisclosed number of employees. While this news was presented as part of a restructuring process that should juice efficiency metrics (and make investors happy), it comes amid a wave of similar layoffs in the logistics sector. Coyote Logistics, which was acquired by UPS in 2015, is set to lay off approximately 200 employees in the coming days. Although no major bankruptcies have rocked the industry just yet, there have been telling signs about weakness in the sector.

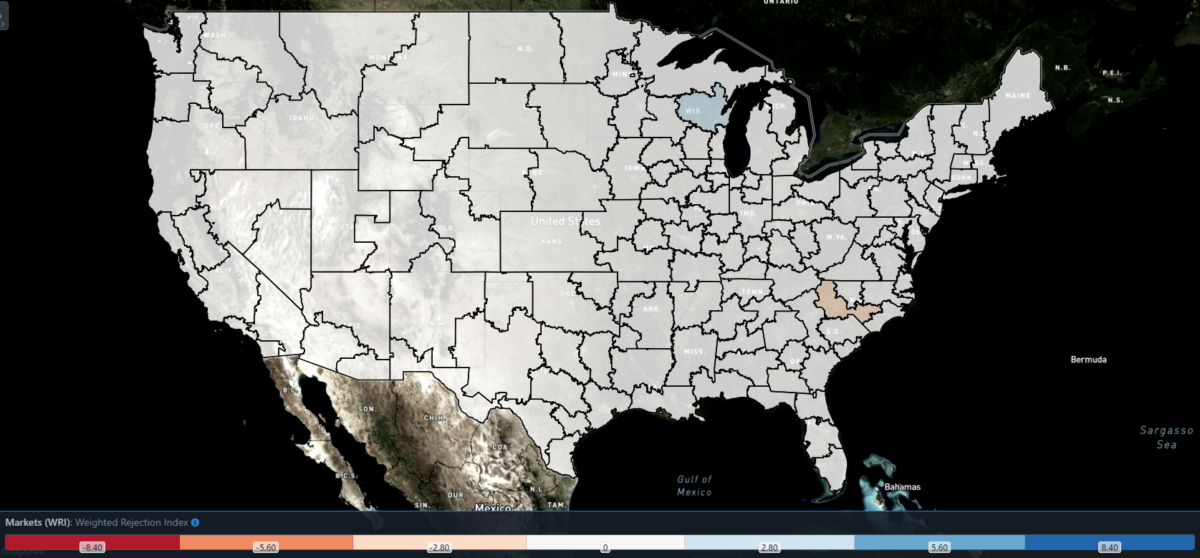

SONAR: WRI (color)

To learn more about FreightWaves SONAR, click here.

The map above shows the Weighted Rejection Index (WRI), the product of the Outbound Tender Reject Index — Weekly Change and Outbound Tender Market Share, as a way to prioritize rejection rate changes. As capacity is generally finding freight this week, only one region posted blue markets, which are usually the ones to focus on.

Of the 135 markets, 59 reported higher rejection rates over the past week, though 32 of those saw increases of only 100 or fewer bps.

As a Chicago native, it pains me to report on the market of Green Bay, Wisconsin. But rejection rates in Green Bay are among the highest in the nation, with the market’s OTRI sitting at 10.38% after a w/w jump of 386 bps. Per USDA data, Wisconsin has shipped over 44 million pounds of potatoes over the past 30 days, a not insignificant contribution to local reefer volumes. The Green Bay market is also known for its insufferable quarterbacks and manufacture of paper products like napkins.

To learn more about FreightWaves SONAR, click here.

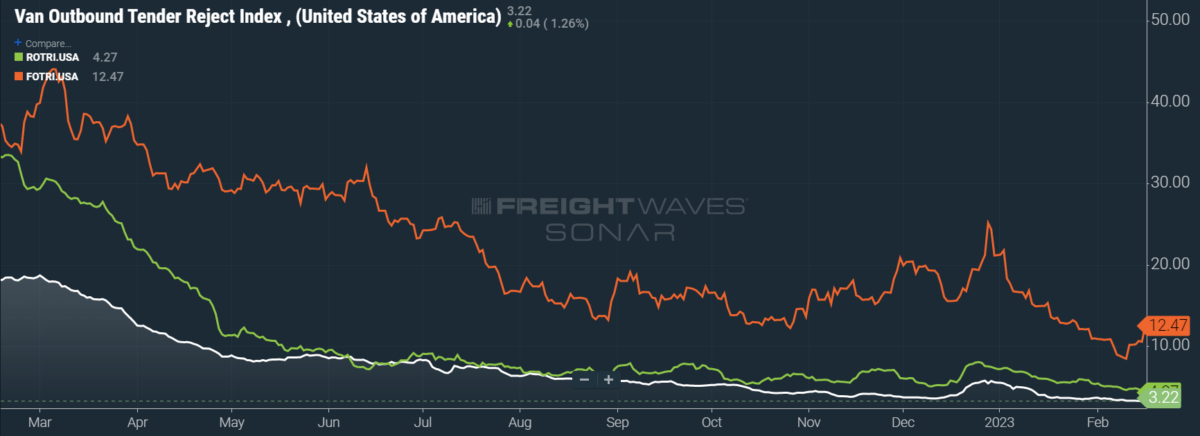

By mode: Just as flatbed rejection rates appeared to be locked in a downward spiral, they rallied this week to erase all of February’s losses (and then some). The Flatbed Outbound Tender Reject Index (FOTRI) swelled 389 bps w/w to 12.47%. It is unclear what is driving this current rebound, although the housing market is showing some preliminary signs of thawing. Even so, housing starts — which drive flatbed demand from construction firms — continued along a five-month decline in January. Other sectors, such as manufacturing, are in a similar slump.

The remaining modes were not as fortunate, with losses suffered by the already-low Van Outbound Tender Reject Index (VOTRI) as well as the Reefer Outbound Tender Reject Index (ROTRI). This week, VOTRI tumbled 15 bps w/w to 3.22% while ROTRI lost 41 bps w/w, falling to 4.27%.

See spot (markets) limp

Spot rates are looking ugly right now, since it is yet uncertain where they will end up finding their floor. So long as capacity remains freely available and tender volumes do not rise from a sudden spike in demand, there are few (if any) sources of upward pressure on spot rates. As seen in OTRI’s movements, those carriers that are lucky enough to have contracted freight are clinging to it for dear life, leaving spot markets desolate. Painful as it may be, carriers will have to tread water for a few more months before any hope of relief is possible.

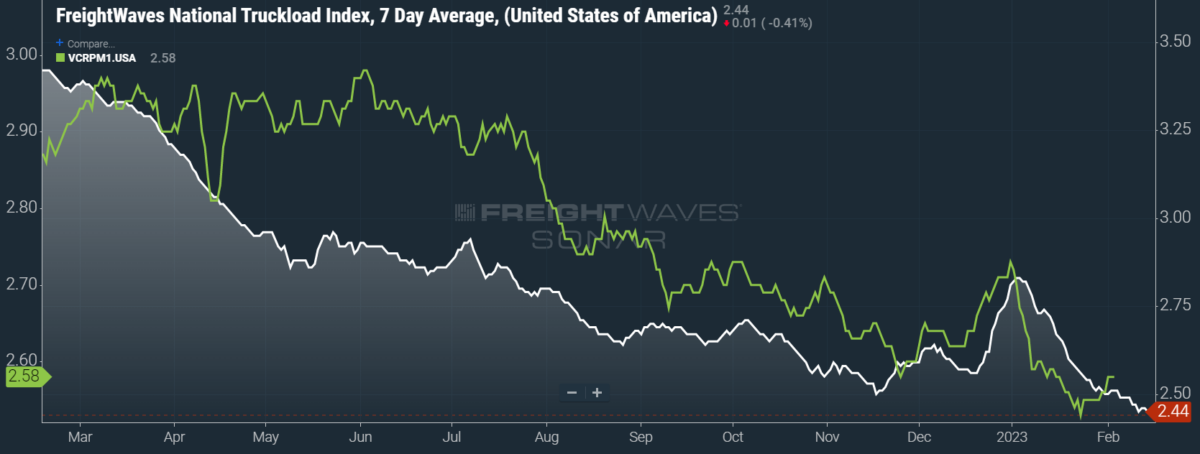

SONAR: National Truckload Index, 7-day average (white; right axis) and dry van contract rate (green; left axis).

To learn more about FreightWaves SONAR, click here.

This week, the National Truckload Index (NTI) — which includes fuel surcharges and other accessorials — fell 3 cents per mile w/w to $2.44. Diesel prices have not made major movements recently since crude oil prices are bound within a certain window, though crude oil prices are quite volatile within those limits. Accordingly, the linehaul variant of the NTI (NTIL) — which excludes fuel surcharges and other accessorials — performed just as poorly this week, falling 3 cents per mile w/w to $1.73.

Contract rates, which exclude fuel surcharges and other accessorials like the NTIL, had a relatively good week, albeit without any gains that change our forecast. Since contract rates are reported on a two-week delay, the current data displays trends for the first few days of February. Contract rates climbed 3 cents per mile w/w to $2.58, rebounding from an earlier dip to $2.53.

To learn more about FreightWaves SONAR, click here.

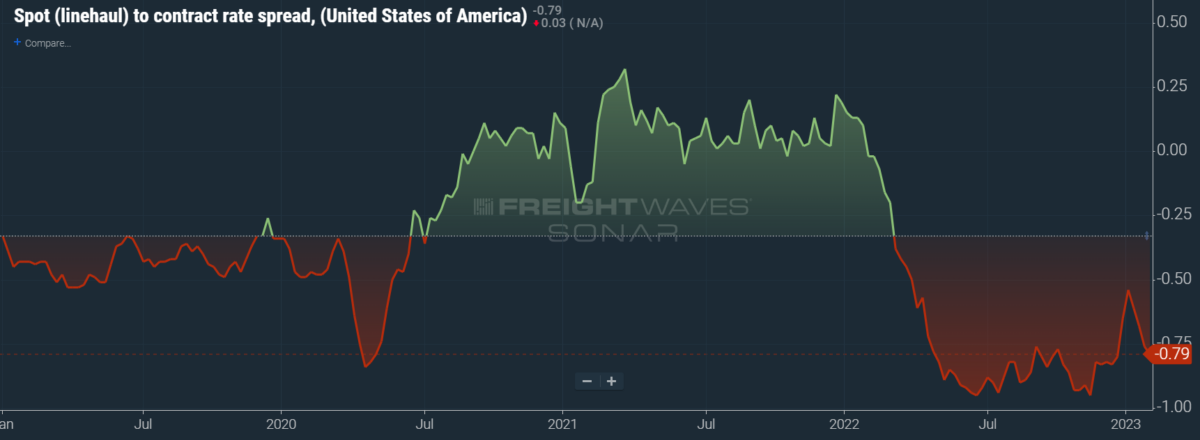

The chart above shows the spread between the NTIL and dry van contract rates, revealing the index has fallen to all-time lows in the data set, which dates to early 2019. Throughout that year, contract rates exceeded spot rates, leading to a record number of bankruptcies in the space. Once COVID-19 spread, spot rates reacted quickly, rising to record highs on a seemingly weekly basis, while contract rates slowly crept higher throughout 2021.

Despite this spread narrowing significantly over the first few weeks of the year, tightening by 20 cents per mile since mid-December, it has started to widen again. Since linehaul spot rates remain 79 cents below contract rates, there is still runway for contract rates to decline over the coming months.

To learn more about FreightWaves TRAC, click here.

The FreightWaves TRAC spot rate from Los Angeles to Dallas, arguably one of the densest freight lanes in the country, continues to reach new lows in the data set. Over the past week, the TRAC rate fell 8 cents per mile to $2.10. The daily NTI (NTID), which has fallen to $2.43, is still outpacing rates from Los Angeles to Dallas.

To learn more about FreightWaves TRAC, click here.

On the East Coast, especially out of Atlanta, rates are similarly declining and are still separating from the NTID. The FreightWaves TRAC rate from Atlanta to Philadelphia fell 1 cent per mile this week to reach $2.34, compounding previous losses. Except for Q4’s holiday run, rates along this lane have been dropping stepwise since mid-July, when the TRAC rate was $3.48 per mile.

For more information on the FreightWaves Passport, please contact Michael Rudolph at mrudolph@www.freightwaves.com or Tony Mulvey at tmulvey@www.freightwaves.com.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now