C.H. Robinson, North America’s largest third-party logistics provider, released financial results for the third quarter before the market opened Wednesday that fell well short of analyst expectations.

The company reported diluted earnings per share of $1.78 compared to consensus estimates of $2.17, a decline of 3.8% year over year (y/y).

C.H. Robinson’s total revenue came in at $6 billion, below Wall Street’s expectations of $6.32 billion and a 4% decline from the same period last year. The company’s adjusted gross profit increased by 5.1% y/y to $887 million.

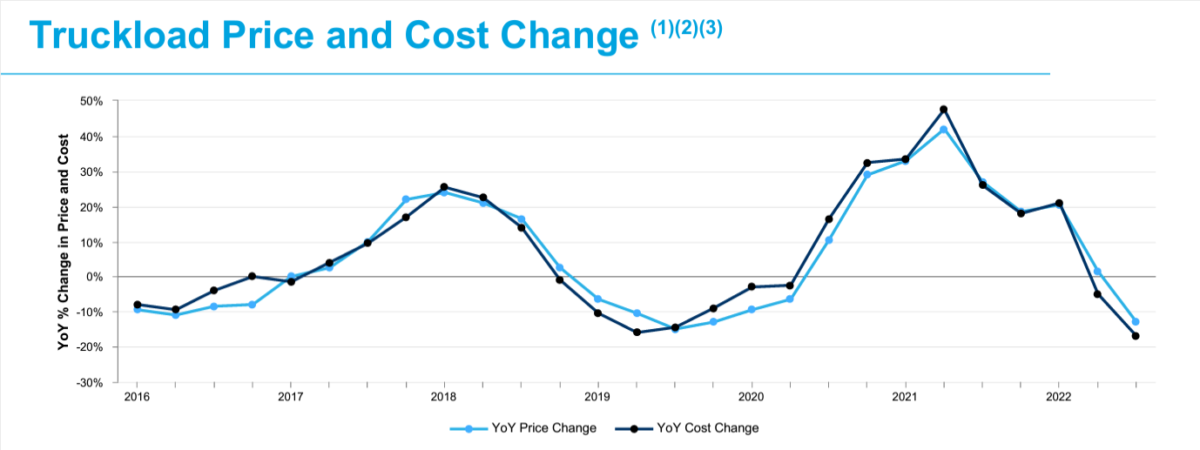

“On our second-quarter earnings call in late July, I talked about a deceleration in demand that we expected to see in the second half of 2022 in three large verticals for freight, including weakness in the retail market and further slowing in the housing market,” said Bob Biesterfeld, president and CEO of C.H. Robinson. “We’re now seeing those expectations play out, with slowing freight demand and price declines in the freight forwarding and surface transportation markets.”

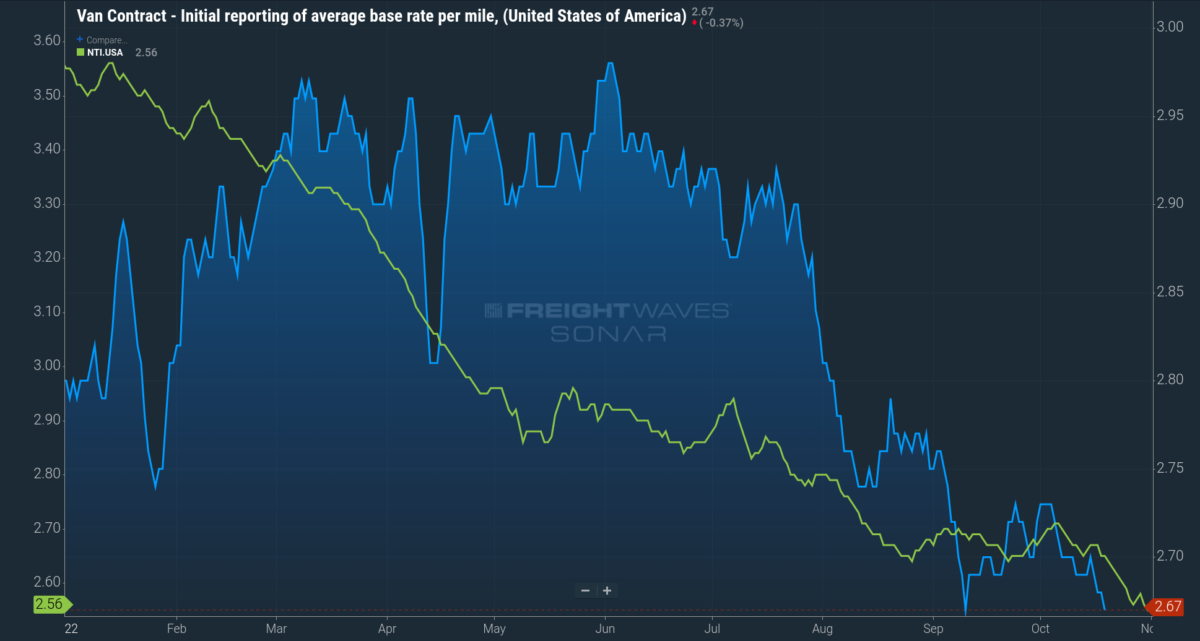

The company’s North American Surface Transportation (NAST) segment reported revenue growth of 4.9% compared to a year ago, up to $4 billion. The company cited declines in truckload pricing as the price charged to customers, excluding fuel surcharge, declined 13% in the quarter compared to 2021.

To learn more about FreightWaves SONAR, click here.

NAST’s adjusted gross profit increased by 22.5% y/y to $563.8 million, down nearly 10% sequentially. The boost in adjusted gross profit stems from a 17% decline in the truckload linehaul costs. Adjusted gross profit for the truckload segment of NAST increased by 20.8% y/y due to a 20.5% rise in adjusted gross profit per shipment and a 0.5% increase in truckload volumes.

The company’s LTL adjusted gross profit grew faster than the truckload sector, rising 22.7% y/y, despite a 1.5% decrease in LTL volumes.

The company continues to get squeezed as NAST operating expenses increased 13.1%, stemming from a 10.8% increase in headcount, legal settlements and technology expenses.

Source: Company earnings, FreightWaves analysis

The company’s growth engine over the past few years, Global Forwarding, faced severe headwinds during the quarter. Global Forwarding revenue declined by 23.6% in the quarter to $1.5 billion as the ocean market cooled throughout Q3. The decline in Global Forwarding revenue is accelerating, declining 28.5% sequentially, following the 4.6% decline from the first quarter to the second quarter. The segment’s adjusted gross profit declined 20.1% y/y to $248.4 million.

Ocean’s adjusted gross profit declined by 25.6% in the quarter, stemming from a 24% decrease in adjusted gross profit per shipment and a 2.5% decline in ocean shipments. The air cargo market’s decline wasn’t as significant as adjusted gross profit fell 21.1% y/y. Unlike the ocean market, the decline in air was driven by a dramatic decline in volumes as metric tons shipped declined by 16.5%.

Global Forwarding, like NAST, continues to face pressure in operating expenses, rising 11.5% y/y, as headcount increased 13.5%.

All other corporate results, which include Robinson Fresh, Managed Services and Other Surface Transportation, experienced revenue growth of 6.8% to $501.8 million. Adjusted gross profit for Robinson Fresh increased 3.8% to $27.7 million; Managed Services rose 10.8% to $29.5 million; and Other Surface Transportation fell 10.5% to $17.7 million.

“But we also need to continue evolving our organization to bring focus to our highest strategic priorities, including keeping the needs of our customers and carriers at the center of what we do and lowering our overall cost structure by driving scale. The work that our team is executing on related to scaling our digital processes and operating model, while working backwards from the needs of our customers and carriers, is focused on driving improvements in our customer and carrier experience, and in turn, driving market share gains and growth. We’re also focused on improving productivity, which in turn reduces our long-term operating costs and increases profits, leading to continued strong returns to shareholders,” Biesterfeld stated.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now