Deutsche Bank transportation equities analyst Amit Mehrotra said that further downward revisions to truckload carriers’ earnings are already priced in, and investors can now buy upward momentum in the second half of 2020 at a discount.

Mehrotra’s September 22 investor note on U.S. Transportation, “Bullish on 2020,” explains why he thinks railroad, truckload, and less-than-truckload stocks are all poised for a positive inflection in early- to mid-2020.

“We see good opportunity for underlying freight flows and data to inflect positively next year, allowing for a re-acceleration in top-line trends after weak 2019 growth,” Mehrotra wrote.

The CASS shipment index has been negative on a year-over-year basis for nine straight months, which is about half the time of a typical downturn. Therefore, Mehrotra expects it to turn positive in mid-2020. Mehrotra also pointed out that DHL’s Global Barometer Index dipped below 50 for the first time since the last U.S. industrial recession, and a dip below 50 is typically followed by a sudden spike upward.

Finally, there are signs that global growth is stabilizing. According to Deutsche Bank’s Global Growth Model, 16% of countries showed accelerating growth in August versus just 10% in July. American industrial production lags global growth–foreign companies have to see demand for their products and earnings grow for a few quarters before they start investing in more machinery and resources. But stabilizing global growth now implies a bottoming and upward inflection in U.S. industrial production at some point near the middle of next year.

One comment by Mehrotra was especially intriguing to me.

“For the first time in 18 months (i.e. since CAT’s “high water mark” comment), we see a clear path for upside in shares of KNX, the country’s largest truckload company,” Mehrotra wrote.

The reference is to Caterpillar’s (NYSE: CAT) first quarter 2018 earnings call that April, when chief financial officer Brad Halverson said that the quarter’s earnings per share would be the ‘high water mark’ for the year. That remark put a dark cloud over the rest of the industrial sector’s earnings season.

Caterpillar, the heavy equipment manufacturer, is often considered a bellwether of the global economy. The company recorded $54 billion in revenue in 2018, and the majority of it was international. The industrial sectors it serves including construction, mining, timber, and oil and gas are highly sensitive to macroeconomic cycles.

Mehrotra’s comment illustrates the fundamental connection between basic industrial activity and freight demand, and how Caterpillar orders can be read through as leading indicators of U.S. truckload demand. The logic works like this: when foreign manufacturers sense an uptick in U.S. consumer demand, they invest in machinery to refurbish old facilities, build new production capacity, and extract more natural resources. Later, those goods hit American shores as imports and are moved by truck.

It’s worth remembering that while the first quarter of 2018 was Caterpillar’s “high water mark,” Knight-Swift (NYSE: KNX) didn’t hit its high water mark until the fourth quarter of 2018. So, in a very real sense, Caterpillar’s international orders are a leading indicator for U.S. domestic transportation demand.

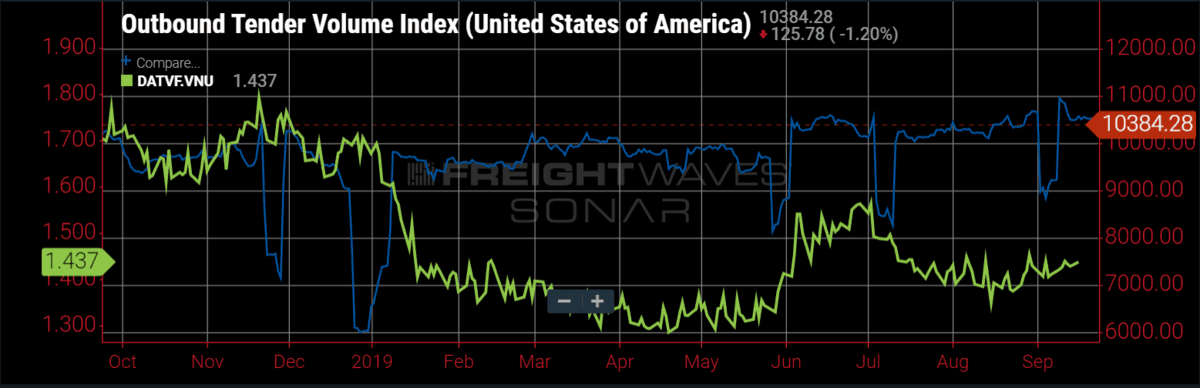

So far, tendered truckload volumes on a national basis (OTVI.USA) have been positive year-over-year for two months, and national average dry van spot rates (DATVF.VNU) are holding above their lows in the first quarter.

For U.S. truckload carriers, the third quarter earnings calls should be an opportunity to guide lower for 2020 and, hopefully, create room for a surprise to the upside.

“As such mgmt’s 1Q’20 guidance – expected next month with 3Q results – should be the catalyst for broad-based downward revisions, allowing market participants to pivot focus from numbers being too high to potential for positive revisions in 2H’2020 as truckload fundamentals tighten once again (reflecting ytd new truck orders that are well below replacement demand),” Mehrotra wrote.

Deutsche Bank likes Werner Enterprise (NASDAQ: WERN), too, but said that recently intensified competition for dedicated freight was a near-term risk to the carrier.

For railroads, Mehrotra’s argument was easier to follow. Consider how well the Class 1s have performed in a tough freight environment with negative year-over-year volumes, managing to keep lowering their operating ratios and utilizing their assets more efficiently. In the second quarter of 2019, Union Pacific (NYSE: UNP) reported an all-time operating ratio record of 59.6%, a 340 basis point improvement compared to the year prior, and all that on 1% lower operating revenue.

If the railroads are running their networks that profitably on weak revenues, then when freight demand accelerates and volumes break back into positive territory, the incremental margins will be very wide indeed. At a basic level, if the trains are still full enough to generate healthy profits at lower volume levels, when volume is added back, much more of that additional revenue will drop to the bottom line.

“We forecast UNP–the country’s largest railroad–to report its best-ever operating margin in 3Q (58% OR, +375bps yoy) despite enduring recession-type volume declines (-700bps),” Mehrotra wrote. “This is staggeringly strong operating performance and points to opportunity for low/mid-50s OR in an environment of slow and steady volume growth, which is likely in 2020.”

Investors are too focused on near-term risks like third quarter volumes and the decline of coal, Mehrotra explained, and should instead think about how profitable any additional volumes would be once the freight cycle inflects upward. Mehrotra’s “structural buys” in railroads include Union Pacific, CSX (NASDAQ: CSX), and Kansas City Southern (NYSE: KSU).

For less-than-truckload (LTL) stocks, Mehrotra likes Saia (NASDAQ: SAIA) and XPO Logistics (NYSE: XPO). XPO will benefit the most from a positive freight environment, while Old Dominion’s (NASDAQ: ODFL) shares still enjoy high multiples and will only move upward on earnings growth, Mehrotra wrote.

Mehrotra’s note concluded by arguing that near-term risks in rates and volumes have already been priced in to most modes of U.S. surface transportation and that investors can get in on a likely 2020 recovery for a discount.

“In this context we see an opportunity for a sector-wide uplift in earnings and valuation post 3Q results season, as headwinds lead to tailwinds and market participants discount a recovery in 2020,” Mehrotra wrote.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now