The Cass Freight Index Report showed another meaningful drop in shipments during June which left the author of the report, Donald Broughton, posing two questions. “Has economic contraction already begun? Will GDP be negative in Q2?”

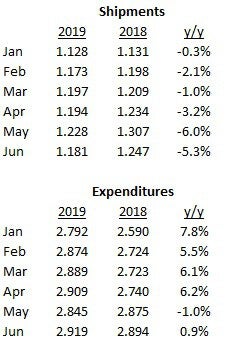

The Cass Freight Shipments Index declined 5.3 percent year-over-year in June, 3.8 percent lower than the May 2019 reading.

From the report, “With the [negative 5.3 percent] drop in June following the [negative 6.0 percent] drop in May, we repeat our message from last month: the shipments index has gone from ‘warning of a potential slowdown’ to ‘signaling an economic contraction’.”

The report continued, “The weakness in spot market pricing for many transportation services, especially trucking, is consistent with the negative Cass Shipments Index and, along with airfreight and railroad volume data, strengthens our concerns about the economy and the risk of ongoing trade policy disputes. Weakness in commodity prices and the decline in interest rates have joined the chorus of signals calling for an economic contraction,” wrote Broughton.

The report highlighted some concerns beyond that of seven straight year-over-year declines in the index. The report called out pronounced declines in international airfreight with specific reference to weakness in Asia, declining railroad carloads especially automotive and building materials, weakness in spot market pricing for transportation services notably in trucking, weakening chemical shipments and a “point of no return” trade dispute as further concerns for potential economic contraction.

The report continued, “our confidence in this outlook is emboldened” pointing to the evidence that since World War II no economic contraction or expansion has occurred without a preceding contraction or expansion in freight volumes.

The report continued further, questioning the strength of the 3.1 percent GDP growth seen in first quarter 2019. He said that the 3.2 percent headline GDP report, later revised lower to 3.1 percent, was surprising and inconsistent with overall freight shipments, but noted that the real number was likely half of what was reported.

“In the methodology used to calculate GDP, all increases in inventory are counted as additions to the GDP, all imports are counted as a negative to the GDP and all exports are counted as a positive to the GDP. Backing out the rising inventories, slowing imports and slightly higher exports, reduces the [first quarter] GDP to less than 1.5 percent,” said Broughton.

The Cass Freight Expenditures Index was up 0.9 percent year-over-year in June after a 1 percent year-over-year decline in May with the conclusion that “realized pricing power has gone negative.” The report said that truckload (TL) spot pricing (excluding fuel surcharges) has been falling for eleven months and that declines in diesel prices, along with excess truck capacity, will continue to drive TL rates lower.

The Cass Freight Expenditures Index is down 2.4 percent from the September 2018 peak.

“The highly discounted pricing available in the spot market has attracted an increased amount of demand, which has deteriorated pricing in the contract market (which is down $0.14 a mile or minus 7.3 percent in the last 10 months), and begun to close the gap between contract and spot [pricing],” said Broughton.

The weakness in the Cass report for June caps off what appears to have been a lackluster second quarter 2019 for freight. This report is consistent with recent data and news reported throughout the industry which prompted most stock analysts to lower their outlook and earnings expectations for publicly traded transportation companies heading into the second quarter earnings season.

If there was a silver lining in the report this was it, “We acknowledge that: all of these negative percentages are against extremely tough comparisons; and the Cass Shipments Index has gone negative before without being followed by a negative GDP.”

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now