The Logistics Managers’ Index Report for March comes right at the inflection point between one of the strongest freight markets ever and the downtown that inevitably follows such a peak.

Its summary and data points are all at highs or near-highs throughout the various categories. But the discussion of what comes next fully reflects the signs that suggest a downturn has commenced.

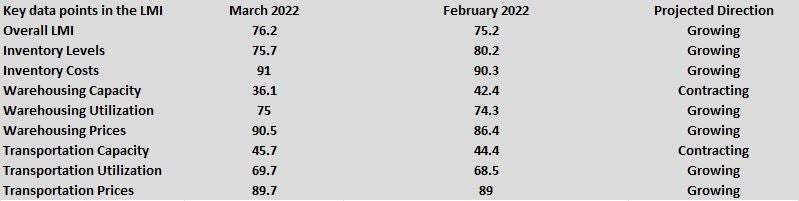

The raw numbers show no obvious signs of market weakness, as most of the individual categories have moved in the direction that signals a strong market. The LMI for March was 76.2, an all-time high, and was up 1 point from February, according to the report released Tuesday. The average for the first quarter was 74.5, significantly above the historic average of 65.2.

“The first three months of 2022 have been marked by high levels of inventory, and insufficient capacity to deal with it,” the report said.

The report is a joint venture by researchers at Arizona State University, Colorado State University, Rochester Institute of Technology, Rutgers University and the University of Nevada, Reno. It is produced in conjunction with the Council of Supply Chain Management Professionals.

Its index is known as a “diffusion index.” The coalition that puts the index together describes it this way: “(A)ny reading above 50 percent indicates that logistics is expanding; a reading below 50 percent is indicative of a shrinking logistics industry.”

The report is not just a backward-looking review. The survey of logistics managers also found several trends that suggest the peak of the freight market is past.

The survey breaks respondents into upstream and downstream: Upstream are the shippers and suppliers of goods; downstream are the buyers and the warehouses.

Upstream respondents, according to the survey, “saw some loosening in the transportation market.” The data coming in from that sector was suggesting an expansion of capacity as the month closed, the first expansion in 18 months.

“This could also mean that we are finally seeing a move away from the unsustainable supply/demand mismatch we have seen over the past 18 months and moving back towards a more viable market equilibrium,” the report said.

Specifically, the figures on transportation capacity reported an “early” and “late” split, and several categories showed a distinct difference between the first part of the month and the latter.

For example, transportation prices, from the perspective of the downstream, came in at an index number of 95.2 for the first part of the month. That declined to 90 in the latter half. The drop was even bigger from the perspective of the upstream: The number declined to 84.8 from 94.2.

The report also discussed the sustainability of the current market elsewhere in the report, noting that the good times couldn’t go on forever. “What we do know is that the wild growth of the last 18 months could never have been sustainable long-run, and that eventually supply chains would hit an inflection point,” the report said. “The question now is whether this inflection will merely balance out supply and demand, helping companies to catch their breath, or plunge the economy into a recession.”

One part of the supply chain that isn’t going to be seeing any sort of easing, according to the report, is warehouses. And one of the reasons is that inventories are soaring.

The inventory level for the month was at 75.7, down from the all-time high of 80.2 a month ago. “Many firms are having difficulties managing all of this inventory, and the excess downstream inventories are now flooding the shelves of off-price retailers like TJ Maxx (NYSE: TJX), Ross (NASDAQ: ROST) and Dollar General (NYSE: DG),” the report said.

Partly as a result, the report said inventory costs were up 0.7 points to 91, an all-time high. “There is little indication that this will change anytime soon, as future predictions for inventory costs are anticipated to remain very high throughout the next 12 months,” the report said.

And the need to store all these goods is running into a warehouse capacity figure of 36.1, which the report said is the lowest in the history of the index. “Unlike what we’re seeing with transportation, there is no movement toward a softening of capacity or price in the warehousing market,” the report said.

One aspect of the inventory build, according to the report, could be companies socking in product well in advance of a potential West Coast dockworkers strike. The current labor contract expires July 1.

If a company is seeking to build more warehouse space, the timeline for doing so has extended to two years from a normal period of nine months, the report said.

While the high price of diesel was discussed in the report, one of the specific observations was on how it might impact truck traffic coming out of, and going back into, the ports of Southern California. Deadhead costs could rise by $2,000 to $3,000 per load because of the high price of diesel. “This will make it less attractive to drive empty trucks back to California, and could significantly impact the tender rejection rate,” the report said.

It cited a recent FreightWaves report on the FreightWaves Supply Chain Pricing Power Index, which showed a significant downturn in volumes out of Ontario, California.

More articles by John Kingston

Truck transportation jobs drop for first time in nearly 2 years

Top performer in Variant’s Ambassador program made 100K before driving a mile

What’s the status of AB5 and its possible impact on trucking in California?

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

Future of Rail Symposium

Reshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post • Chicago, IL Register NowReshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

The Signal at Chattanooga Choo Choo • Chattanooga TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now