Recently, Knight-Swift announced a 28% positive revision on their earnings guidance for Q4 2018. Details will be confirmed on January 29th when they release officially. However, this industry leader appears to have been one of many to report better than expected earnings to the street. With a current market cap of 5.28 Billion, and continued above average performance, it’s confusing why they are still not getting the ‘investor love’ they deserve. Knight-Swift is currently trading at a PE Ratio of 7.61, and near the bottom of their 52 Week Price Range. Heartland and Covenant have recently followed suit with positive earnings surprises. We expect similar releases from Werner and US Xpress to come out soon. Perhaps this continued good news will bring the market along with it. This positive news is reflective of a very healthy fourth quarter for all in the truckload segment. After taking a breather in September, following a record-breaking six-month period, TPP (TCA Profitability Program) members rebounded with very healthy October and November results.

Since joining the TPP team in 2015, I’ve kept a close eye on Knight as they have always been the ‘one to watch’ among many in TPP. In their annual and quarterly filings, one thing that has always stood out when compared to other publicly-traded trucking companies is their degree of transparency. In their 2017 Annual Report (the first as a combined Knight-Swift entity), the first 100 pages are devoted to Executive and Director compensation and disclosures. Normally, this kind of detail is annexed to the middle or footnotes of other company filings. Putting it at the front tells the reader (or investor) that nothing is being hidden, and it conveys a strong message of accountability with respect to their leadership team. Although it be simply be correlation, as opposed to correlation, however it wouldn’t be a reach to assume that accountability and transparency has driven above average results for this company.

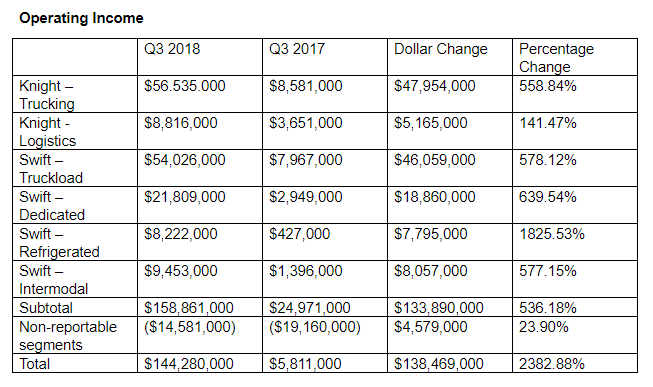

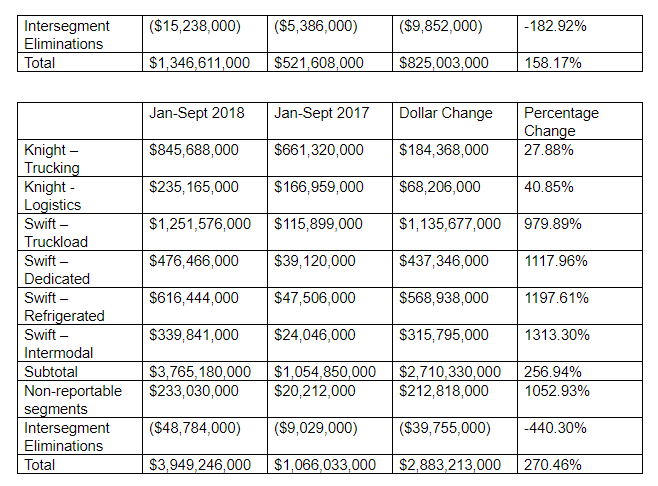

Knight-Swift Operating Ratio Performance

History

Knight Transportation was founded in 1990 by four cousins: brothers Randy and Gary Knight and brothers Kevin and Keith Knight. The four had previously worked in executive positions for Swift Transportation, also based in Phoenix. Randy was a part-owner in Swift when Jerry Moyes bought out his interest. Knight started hauling general commodities from Phoenix, AZ to Los Angeles, CA with just a handful of trucks and a service center in Phoenix. Knight became a publicly traded company in 1994, listing on the NYSE.

Swift is the older of the two companies. Carl Moyes started a small trucking company in Plain City, UT, called B&C Truck Leasing (named after himself and his wife Betty) in the late 1950’s. The company moved to Phoenix in 1966 after their son, Jerry, graduated from Weber State University. The company was renamed Common Market after this move. The name Swift Transportation was purchased from a descendant of the Swift Meat Packing family, when the Moyes family bought the trucking assets of Swift & Company. Jerry Moyes became president, chairman and CEO in 1984 and when Carl passed away in 1985, Jerry bought out the other two partners – his brother Ronald and Randy Knight. Swift went public for the first time in 1990, trading on the NASDAQ exchange. The company went back to private in 2006 when Jerry Moyes offered to purchase the outstanding publics shares that the family did not own. Swift then went back to being a public company in December of 2010 when it listed on the NYSE.

The two companies merged in September 2017, however they still operate as separate entities. Knight was designated as the Accounting Acquirer while Swift was the acquirer for legal purposes. This resulted in Knight’s historical results of operations replacing Swift’s for all periods prior to the 2017 merger. The 2017 Annual Report provided an estimate of $150 million in synergies that are expected to be realized by 2019. The merger resulted in 46% of the new stock held by former Knight shareholders and 54% by former Swift shareholders. The new stock began trading on the NYSE on September 11, 2017.

Operating Attributes

Knight Transportation operates 30 service centers in the United States. The trucking segment offers Dry Van, Refrigerated, Dedicated, Port & Rail Services and Intermodal services. The Logistics segment offers Brokerage services. Knight Truck & Trailer Sales is a wholly owned subsidiary to market equipment that has been identified for disposal.

Swift operates 42 service centers – 31 in the United States and 11 in Mexico. There are an additional 5 secured yards in Canada. Swift Truckload segment offers Dry Van, Flatbed, Refrigerated and Cross Border services into both Canada and Mexico. Mexican service is through Trans-Mex, the only major Mexican Carrier that is 100% owned by a U.S. Carrier. Heavy Haul and Expedited services are also available in this segment. The Dedicated segment is the outsourcing of a company’s internal fleet, meaning that a certain amount of equipment and drivers are dedicated for that customer’s use. It additionally offers the ability to bring in more equipment and drivers on a temporary basis to handle seasonal fluctuations. The refrigerated segment is one of the largest temperature-controlled fleets in the industry, providing service to national customers such as Wal-Mart, Costco and Target. The Intermodal segment handles drayage of customer-owned or leased containers, container on flat car service for door-to-door service throughout North America, trailer on flat car, as well as cross-border container moves into and out of Canada and Mexico.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now