Owner-operators and small carriers are known as the lifeblood of the trucking industry, and for good reason. They make up a large portion of the freight market, and without them, the industry would be severely stunted.

As of December 2020, there were 502,626 “very small” registered fleets – operations involving one to six trucks – across the country, according to the Federal Motor Carrier Safety Administration (FMCSA). At the time, this group accounted for 86% of total carriers and almost 20% of total power units in the U.S.

Of carriers that fall in the “very small” category, the Owner-Operator Independent Drivers Association estimated that approximately 350,000 to 400,000 of them are true owner-operators.

While owner-operators continue to move a significant percentage of America’s goods, many of these critical operators are beginning to feel the uncertainty that accompanies shifting market dynamics.

With pandemic-fueled volume surges and severely strained capacity, carriers have had the market cornered for the past two years. Over the past couple months, however, there has been a distinct market turn as volumes balance out and spot rates begin to slip. At the same time, carriers continue to feel the squeeze from rising diesel prices.

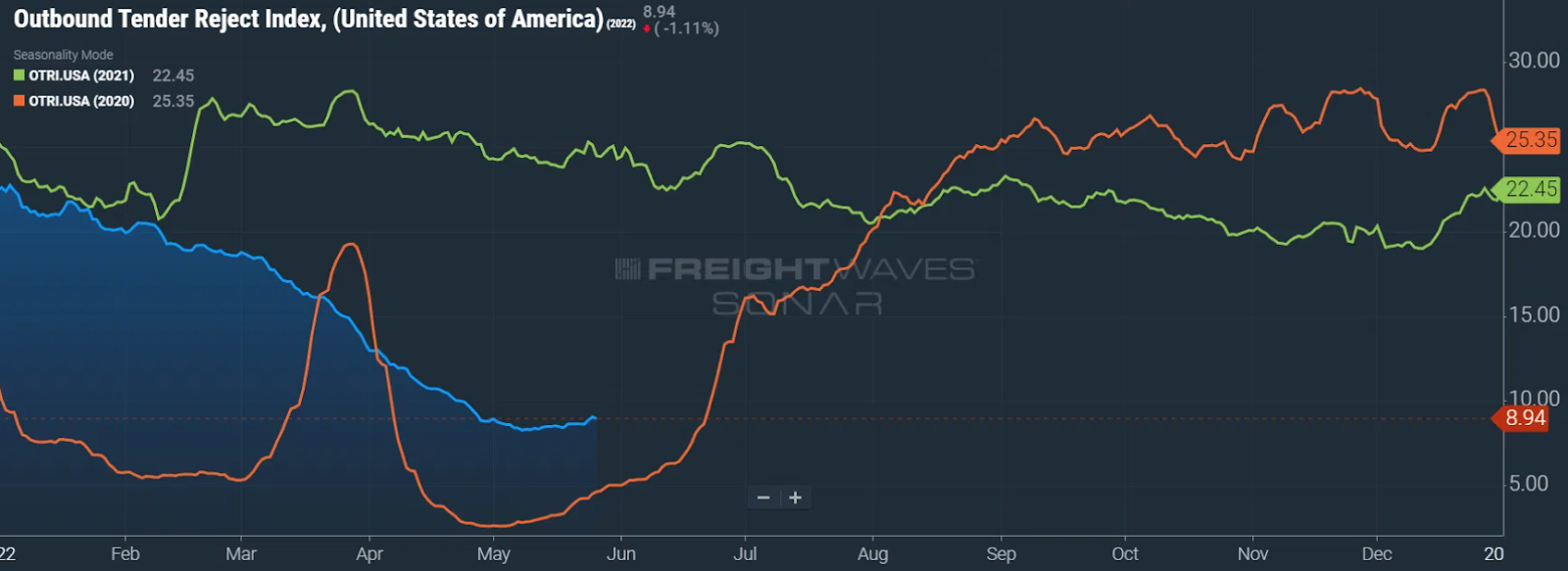

SONAR’s Outbound Tender Rejection Index (OTRI represents the percentage of attempts to book a truck that result in a rejection. As demand outstrips supply, carriers will reject more load requests. As capacity loosens, tender rejections fall.

Despite rising slightly over the past week due to Memorial Day, OTRI remains 1,554 basis points below year-ago levels as a return to double-digit percentages seems unlikely. This trend indicates that carriers are rejecting significantly fewer loads than they were this time last year, supporting the notion that the market is softening.

OTRI includes data from all regions, markets and equipment types. While some segments of the industry – like flatbed carriers – are currently outperforming the overall market, larger market trends can help carriers resting in stronger positions prepare for potential shifts in the coming weeks and months.

Carriers of all sizes are feeling these shifts, but owner-operators are especially vulnerable to market upsets due to their inability to absorb significant financial losses and relative lack of expendable income.

“Owner-operators are running their business like any other carrier, but they are more dependent on spot market rates,” PGT Trucking Chief Innovation Officer Paul Martin said. “The spot market is currently declining while other costs continue to soar.”

For many owner-operators, current market shifts could be challenging enough to sideline their operations. Joining larger fleets as independent contractors could provide these drivers with the support they need to weather volume changes and rate decreases while simultaneously coping with rising fuel and operational costs.

“By driving with PGT, owner-operators get to do what they love: they have the freedom to drive their trucks and know they’re still going to be taken care of when the market shifts. They have the security to keep their business running into the future,” Martin said. “I think security is the biggest thing we offer our owner-operators.”

Flatbed carrier PGT Trucking offers an independent contractor program that enables owner-operators to keep their trucks loaded and moving at the best rates possible, regardless of market condition. When partnering with PGT, owner-operators earn 75% of linehaul revenue, as well as 100% of fuel surcharges. This pay structure – coupled with increased access to freight – often allows these drivers to earn more than ever before, all while benefiting from the reputation and back office support of a major carrier.

Additionally, partnering with PGT gives owner-operators access to cost-saving perks like affordable insurance programs, maintenance discounts and equipment rentals. According to OOIDA, the average owner-operator is still driving a 2008 model year truck, increasing the value of these benefits. These perks can bring down the costs associated with aging equipment, including extra maintenance and higher insurance premiums due to a lack of modern safety equipment.

Programs like PGT’s offer a highly valuable solution for owner-operators because, while dry van trailers are far more common in the overall market, the majority of owner-operators pull flatbed or reefer trailers, according to OOIDA. When partnering up with PGT, independent contractors used to driving flatbeds do not have to sacrifice their preferred equipment type for more common options.

While independent contractors have a lot to gain from partnering with more established fleets, the larger companies also benefit from adding these owner-operators to their teams. On average, these drivers tend to be more experienced and have better safety records than other drivers on the road.

According to an OOIDA research report, the typical owner-operator averages approximately 2.9 million miles of driving during their career, most of which are without a Department of Transportation reportable accident.

Not only are owner-operators often safer drivers, but they also bring a plethora of experience with them. The average owner-operator has also been driving for more than 20 years, and 34% of them report serving in the military, according to the association.

When these highly qualified operators seek to partner with larger companies, it is important for them to consider what each company brings to the table, as well as their reputation and relative stability in the industry.

“The longevity of PGT speaks volumes. We’ve been in business for more than 41 years,” Martin said. “Some of the carriers who haven’t been in business as long might be riding the high, but are they going to be able to stay in business when it hits the low? PGT can provide owner-operators the stability that they need in today’s market.”

PGT has a long history of working with owner-operators. The company was started by an independent contractor, and today, owner-operators still make up a significant portion of the company’s driving force. PGT offers several customized programs for independent contractors, including above average compensation and incentives, access to 24/7 resources, and quality equipment.

“Our leadership knows the importance of an independent contractor,” Martin said. “We really work to build those relationships.”

Ultimately, PGT’s independent contractor programs provide an ideal solution for owner-operators who find they need a little more support to keep their wheels rolling or grow their businesses. From back office support to helping operators create their own full-fledged fleets, PGT provides guidance and assistance without asking owners to fully hand over their autonomy.

Click here to learn more about becoming an independent contractor with PGT.