Cargill’s announcement last week that it is making a nearly half-billion dollar investment in soybeans caught my attention because it suggests that one of the world’s largest food producers believes that soybeans are poised for sustainable growth and the recent price appreciation and surge in production are not just the result of transient trends. It’s clear to me that growing food segments, such as soy-based dairy alternatives and plant-based meat alternatives, are considered sustainable mega-trends by many of the large food/beverage companies and their investors. Add tremendous near-term demand from China and India and you have a soybean market that is off the charts.

For many CPG companies, this is related to the issue that will make or break 2021 for many: whether they can successfully pass on cost inflation (in ingredients, animal feed, fuel, packaging, transportation, etc.) with price increases.

Cargill’s investment highlights soybean production as a growth area. Last week, Cargill announced it would make a $475 million investment to upgrade its soy processing capabilities. The investment will span seven states and will include modernizing plants, expanding crush operations, speeding up loading and unloading times, increased capacity and improving logistics. The investments are designed to increase the company’s soybean production capacity and get customers faster access to soybean-based ingredients. Cargill’s investment is for both food and fuel (soy biodiesel) and to satisfy both foreign and domestic demand growth.

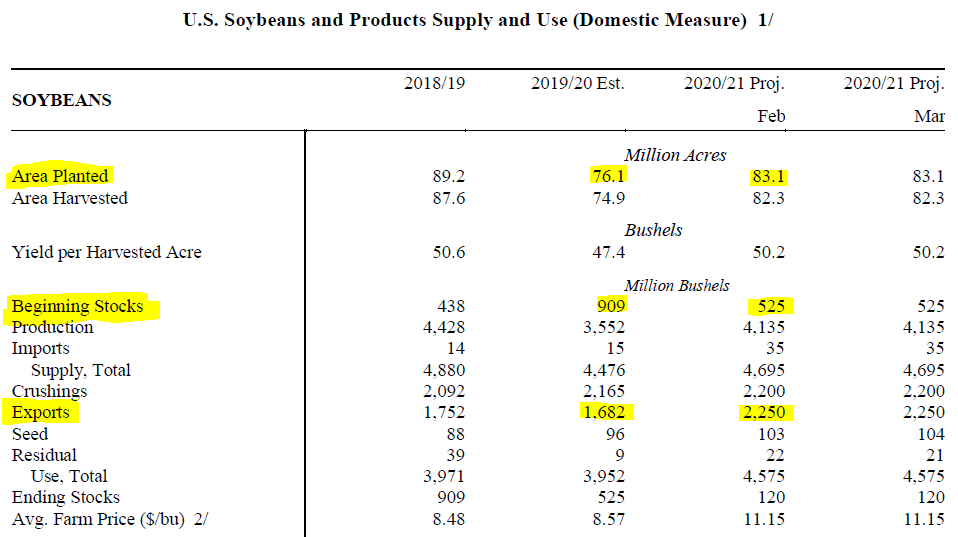

Soybean prices are at their highest level since mid-2014

Soybean prices have surged largely due to overseas demand. Soybean prices are over $14/bushel, up from less than $10/bushel at the beginning of 2020 and are at their highest level since mid-2014. Following the African swine fever debacle that decimated the Chinese hog population, causing the number of Chinese hogs to decline about 40% in 2019, a major push continues in China to replenish the hog population. Replenishing the hog population requires production of feed rations that contain corn and soybean meal. As a result, China is expected to buy 104 million metric tons of soybeans this year and total U.S. soybean exports are expected to rise 34% in the current 2020-21 crop year from the 2019-20 crop year according to the USDA. This comes after a period of weak volumes of U.S. soybean exports to China in 2019/1H20 related to the trade war. As China began buying U.S. soybeans in greater volume last year, soybean yields were below expectations, pushing up prices. Soybean stocks have been constrained ever since and started the 2020-21 crop year 42% below prior year levels.

The resurgence of the African swine fever in China adds a level of uncertainty to the outlook for soybeans. There have been reports of this returning with the sow heard falling 3%-5% each month since September. The major resurgence could cause soybean prices and U.S. exports to fall as the Chinese feed a smaller hog population and soybean meal prices, which have declined since late last year, could be a leading indicator for soybean prices.

But there is a lack of consensus about the impact that African swine fever will have. At a recent investor conference, Archer-Daniels-Midland expressed doubts that there would be a full return of the African swine fever to the degree that was seen earlier, citing improved sanitary conditions at farms. The company also described the heightened crop demand from China to be a “medium-term phenomenon” and expects soybean and corn-related feed prices to continue to increase in the near term.

Soybeans ⸺ acres planted/harvested ↑, stocks ↓, exports ↑

High soybean prices are having impacts on other U.S. crops. U.S. corn exports are expected to be higher by 46% y/y. Soybeans are more profitable for farmers than corn, particularly at recent prices, which has caused farmers to increase their soybean acreage by about 7 million acres, or 9%, from last year. Corn competes for the same acreage and, as a result, there has been less acreage available to produce corn. The USDA expects corn to be up a somewhat more modest 4% y/y during the 2020-21 crop year. Plus, it seems likely that there will be another significant increase in soybean planting acreage this summer. As a result, corn prices have also risen sharply, up nearly 50% in the past 12 months. Rising crop prices can be seen in other crops as well, such as canola, and rising ingredient prices have led most CPG companies to say they expect cost increases in at least the low single digits, which I believe may be understating how much their costs may actually rise.

The Canadian Class I railroads have been hitting new monthly records for grain carloads.

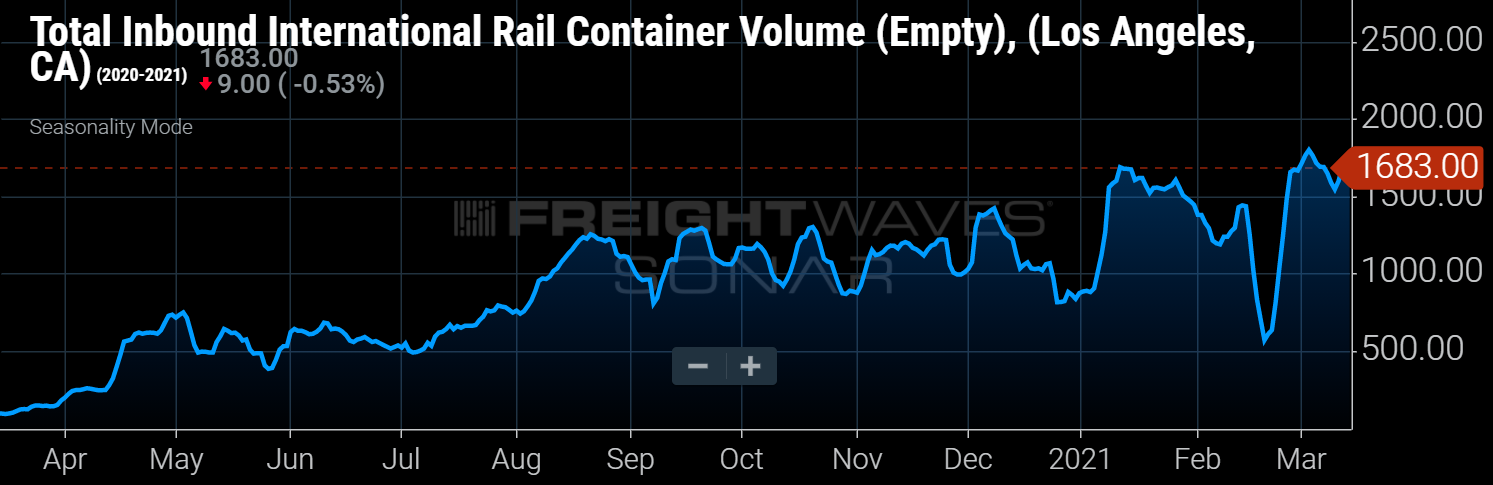

Meanwhile, tight transportation markets have made getting soybeans to market more difficult. Grain produced in the U.S. and Canada for export generally move via rail or barge, but a significant portion (5%-7% of U.S. soybeans exports) move in international shipping containers that are being repositioned back to the West Coast ports. The recent tightness in the international container market has caused the container ship companies, which own or lease the international containers, to demand that those containers return quickly without being reloaded with grain on the backhaul routes, something that has never been a major profit center for the shipping lines.

The number of empty international (primarily 40-foot) containers heading back empty to the ports of LA and Long Beach have steadily risen in the past year.

Meanwhile, competition is increasing from Brazilian exporters of soybeans. The USDA estimates that Brazil corn and soybean exports could reach record levels, which may put upward pressure on ocean freight rates for bulk grain. However, soybeans leaving Brazil have a natural disadvantage because it takes 45 days for shipments leaving Brazil to reach ports in China versus closer to two to three weeks for shipments leaving the U.S. or Canadian Pacific coast.

Do you think rising ingredient prices will get in the way of CPG companies’ results? Let me know at mbaudendistel@www.freightwaves.com.

If you would like to receive this newsletter, please join us here: https://web.www.freightwaves.com/thestockout

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now