Uber Technologies, Inc. (NYSE: UBER) reported a net adjusted loss of 64 cents per share, 4 cents better than the consensus estimate. Consolidated adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) was a loss of $615 million, a more than $200 million improvement year-over-year.

Uber pulled forward its profit guidance, which now calls for its first quarter of adjusted EBITDA profitability to occur in the fourth quarter versus the prior guide of during 2021.

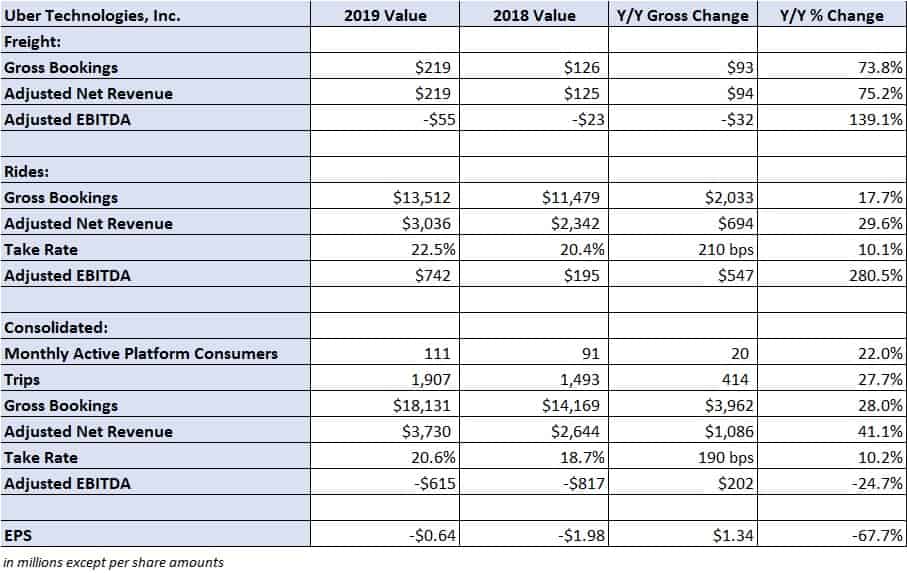

Uber Freight results

The company’s digital freight brokerage division, Uber Freight, reported a 74% year-over-year increase in gross bookings to $219 million. Gross bookings declined $4 million sequentially from the third quarter. Loads in the freight division increased by 89% year-over-year, although the actual number of transacted loads on its platform was not disclosed.

Adjusted net revenue in freight increased 75% year-over-year to $219 million, but only $1 million higher sequentially in the period. It was the lowest quarter-over-quarter growth rate in adjusted net revenue for the freight division since the company began disclosing the division’s results.

Adjusted EBITDA was a loss of $55 million in the quarter, $32 million worse on a year-over-year basis. However, adjusted EBITDA was $26 million better than the third quarter of 2019 on a similar level of gross bookings. Management noted lower truck pricing in the quarter.

The web portal designed for web-based carriers, which launched in the third quarter, accounted for 10% of the freight group’s overall capacity during the period. The company said that freight’s in-app bundles that allow carriers to book multiple loads at once “have reduced empty miles versus non-Uber Freight matched bundles.”

Management was measured in discussing future expansion for the freight division. It said the company will pursue “responsible expansion” and noted a “heavy focus on unit economics.”

“We recognize that the era of growth at all costs is over. In a world where investors increasingly demand not just growth, but profitable growth, we are well-positioned to win through continuous innovation, excellent execution, and the unrivaled scale of our global platform,” Uber CEO Dara Khosrowshahi said about the company’s overall growth strategy.

UBS recently initiated coverage with a “buy” rating. In a note to investors, equity research analyst Eric Sheridan said that he believes Uber Freight could see $6 billion in annual revenue in the future.

“Going forward, we forecast Freight scaling to a $6bn+ annual revenue segment by 2024E as Uber continues to invest behind the further buildout of its logistics network and demand generation domestically as well as potential geographic expansion (incl. announced plans to launch in Germany),” stated Sheridan.

Consolidated and Rides

Uber reported that monthly active platform consumers increased by 20 million to 111 million users with total trips increasing 28% year-over-year. Gross bookings increased 18% in Rides with a 30% increase in adjusted net revenue. Adjusted EBITDA in the division increased nearly $550 million in the period to $742 million.

Shares of UBER are up more than 3% in after hours trading.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now