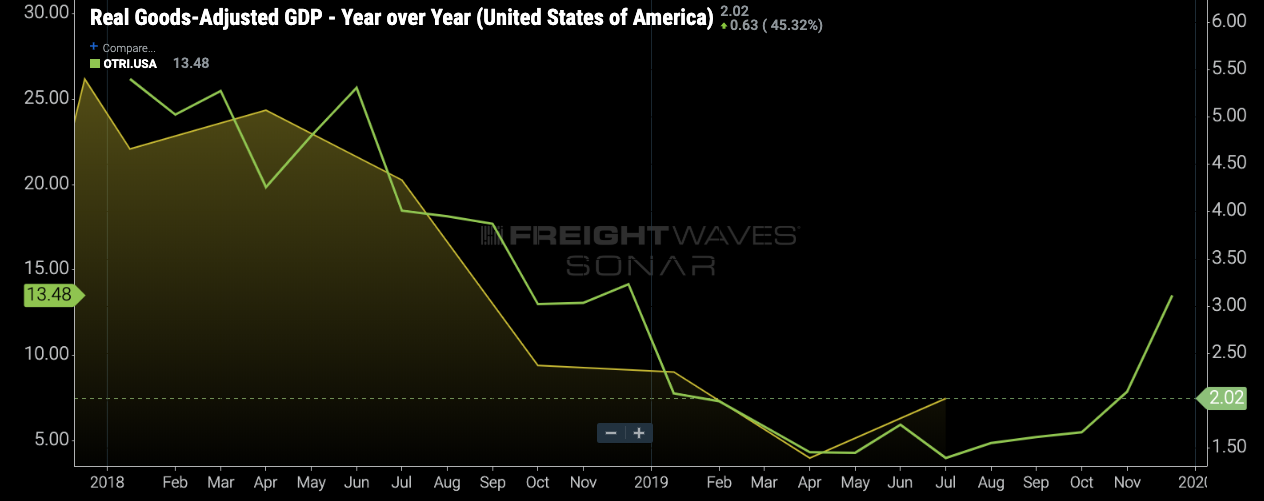

Source: SONAR – OTRI.USA, GAGDPY.USA

Gross domestic product (GDP) is the most commonly referenced metric of economic activity and is tracked by economists, market analysts and politicians to gauge the strength of economies. It measures the final value of all goods and services within an economy in a given period and serves as the broadest measure of total production and output.

Why shouldn’t I use GDP to gauge the freight outlook?

The overall GDP number is not very useful when looking for insight into freight conditions in the economy. The U.S. economy is dominated by the service sector, which includes segments like health care, education and financial services. These areas make up over half of all of the economic activity in the U.S. but do not play a significant role in freight movements in the economy. As a result, as long as the service sector is healthy, the U.S. economy can continue to grow even if the production and transportation of goods is stalling.

How should I interpret the GDP?

Due to the strength of the service sector, the total GDP growth figure is likely to misrepresent the state of the freight economy. That does not mean that the GDP figures should be completely disregarded, however. The details within the GDP release contain valuable information about the flow of goods in the economy, and a breakdown of the components of GDP can help create a better understanding of how the various areas of freight perform during any given quarter.

What components of GDP should I care about?

Goods-adjusted GDP looks at private final goods demand in the economy. It excludes services and non-tangible goods from the calculation and does not exclude imported goods.

Formula: Goods consumption + nonresidential fixed investment in equipment + residential fixed investment + investment expenditure in structures + goods exports.

The broader goods-adjusted GDP values give a better representation of freight activity in the economy by looking at the demand for goods. Other factors should be considered when looking at the freight market, such as inventory trends and government activity. Still, the final demand for goods is a good starting point for understanding freight volumes during any given period. In addition, a look at the various components of goods-adjusted GDP will illustrate what areas of the freight economy are driving overall volume performance.

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post • Chicago, IL Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now

Noble1

More music to my ears ,LOL ! I’m BIG TIIME bearish on the markets and also believe oil will retreat . Oil appears to be a proregressive correction , be vigilant ! In my humble opinion ………

This is going to be another quote:

Fed Quietly Confirms Fears About Stock Market’s $10 Trillion Powder Keg

The Fed’s plans to keep interest rates low in 2020 despite corporate debt bubble fears and “reckless” risk-taking in the stock market.

Low interest rates helped propel the stock market to new records. But they may also accelerate its demise.

The Fed published its December meeting minutes to little fanfare.

A paragraph within the meeting summary suggests central bankers are becoming uncomfortable with the ballooning corporate debt bubble.

Warnings that the stock market can’t keep marching higher have started to look more credible.

For months, warnings about market bubbles and a potential stock market crash have been ringing throughout Wall Street. Now, the US Federal Reserve has subtly added its voice to the chorus of alarm bells.

The central bank’s most recent meeting minutes suggest that some of its members are becoming concerned that the Fed’s easy-money policies have inflated a dangerous corporate debt bubble. The bank’s decision to keep interest rates low throughout 2020, they warned, could exacerbate the problem.

Fed Minutes Confirm Corporate Debt Bubble Worries

Traders are likely applauding the Fed’s decision to keep interest rates unchanged in December, as well as the bank’s intention to maintain low rates for the remainder of 2020.

But that kind of thinking is exactly what the bank is worried about, according to the summary of its latest meeting.

Some of the Fed’s members expressed concerns about the repercussions of the bank’s easy-money policies. | Source: REUTERS/Jonathan Ernst

According to the Fed’s meeting summary, some from the bank are worried that its own policies will continue fueling the corporate debt bubble and make the next US recession even more severe.

A few participants raised the concern that keeping interest rates low over a long period might encourage excessive risk-taking, which could exacerbate imbalances in the financial sector.

The concerned few also,

remarked that such policies could be inconsistent with sustaining maximum employment, could make the next recession more severe than otherwise, or could strengthen the case for the active use of macroprudential tools to guard against emerging imbalances.

Essentially, the bank has been forced to make a decision— pain now, or pain later. Apparently, the majority of central bankers opted for the latter.

Corporate Debt a $10 Trillion Concern

The Fed isn’t the only one to sound the alarm on the worrying amount of debt US businesses have racked up while interest rates were low.

Corporate debt has risen by 50% since the financial crisis, bringing the grand total to just under $10 trillion. ”

END QUOTE !

Noble1 suggests SMART truck drivers should UNITE & collectively cut out the middlemen picking driver pockets

Quote myself :

“More music to my ears ,LOL ! I’m BIG TIIME bearish on the markets and also believe oil will retreat . Oil appears to be a proregressive correction , be vigilant ! In my humble opinion ……… ”

UPDATE !

January 6 2020 WTI price high was $64.72 , today’s WTI price low was $50.98 !!! A WTI price per barrel dive of $13.74 , -21.2%

YEEEEEEEEEEE HAAAAAAAAAAAA ! Another call right on the money !!! (wink)

Noble1

Awaiting January barometer to confirm market rally is caput(kaput) !

Fib ratio confluence is suggesting it is , along with extreme market sentiment .

Oil price increase also putting pressure on consumer spending .

US attack on Iran will shift consumer sentiment .

Hold on to your hats !

In my humble opinion …………..

Noble1 suggests SMART truck drivers should UNITE & collectively cut out the middlemen reducing driver profits

UPDATE !

JANUARY BAROMETER CONFIRMED AND SMILING ON MY CALL !!!

Quote :

Friday’s massive sell-off ruins ‘January barometer’ market signal

The stock sell-off deepened on the last day of January on concerns that the deadly coronavirus will disrupt the global economy, and in the process ruined an old market indicator that was signaling a positive year.

As goes January, so goes the year — this Wall Street saying from the widely watched “January barometer” suggests a correlation between January’s performance and full-year returns.

Friday’s losses erased all the earlier gains in January for the S&P 500, with the index down about 0.2% on the month. The Dow Jones Industrial Average has turned also red for January, down 1%. Perhaps the indicator now is signaling a volatile year we may have ahead.”

End quote .

YEEEEEEE HAAAAAAA !!!!

In my humble opinion ………….