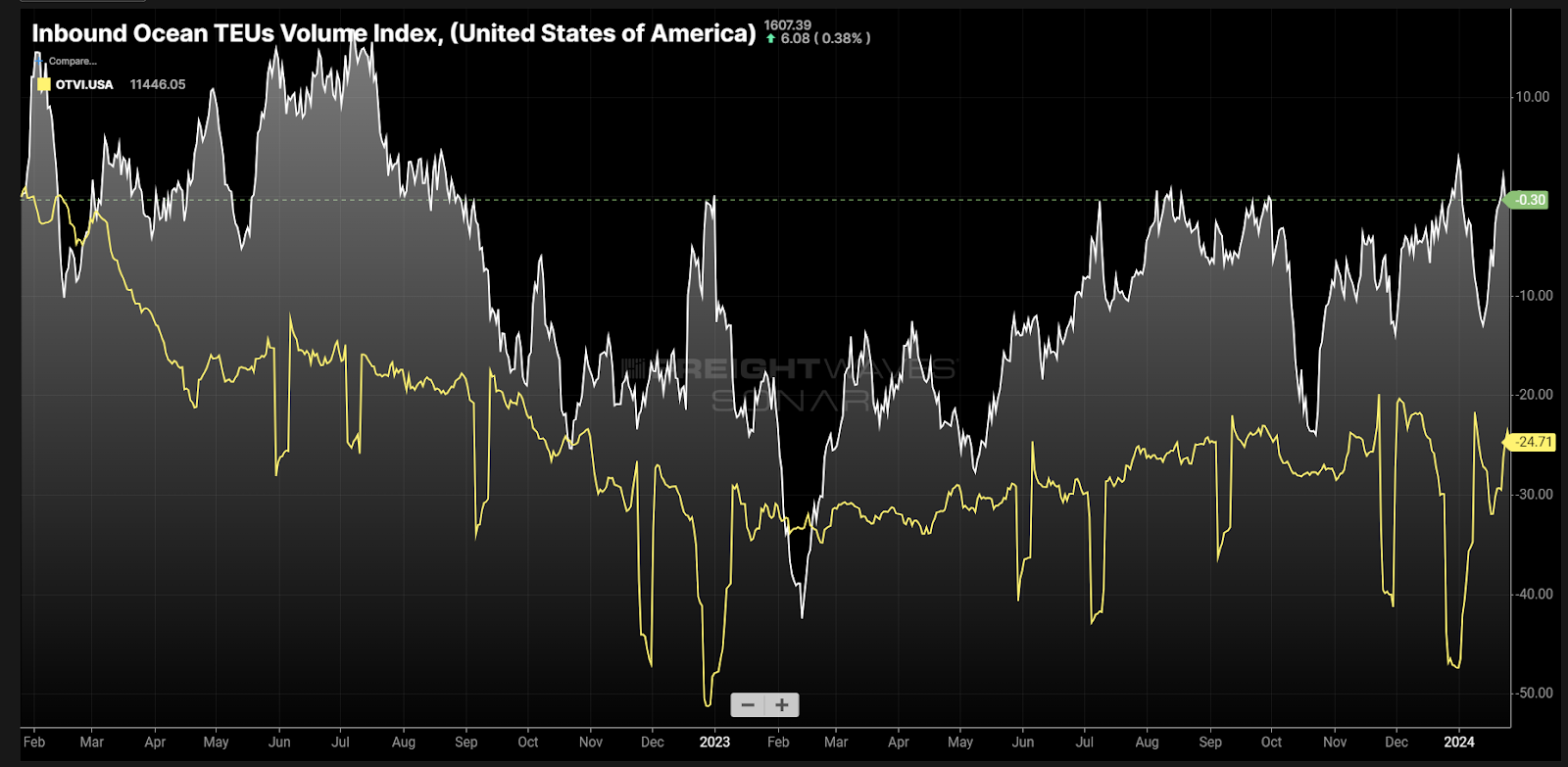

Chart of the Week: Inbound Ocean TEUs Index, Outbound Tender Volume Index – USA SONAR: IOTI.USA, OTVI.USA

Import demand based on bookings of twenty-foot equivalent units heading into the U.S.

(IOTI) remains down compared to two years ago, but only slightly. Truckload tender volumes (OTVI) are down roughly 25% compared to the same period in 2022. These two figures are effective indicators of goods demand in the U.S. This is the perspective of deterioration that many businesses are still coping with even as GDP figures seem strong.

Many sectors of the economy are still adjusting to the fallout from the pandemic-era hypergrowth, making an annual figure less representative of their experience. Transportation has been one of the most significantly impacted.

Inflation-adjusted real GDP growth once again seemed to surprise to the upside with a 3.1% annual growth figure in the fourth quarter of 2023. Many companies did not feel this historically strong growth as they have in the past. It all has to do with adaptation and perspective.

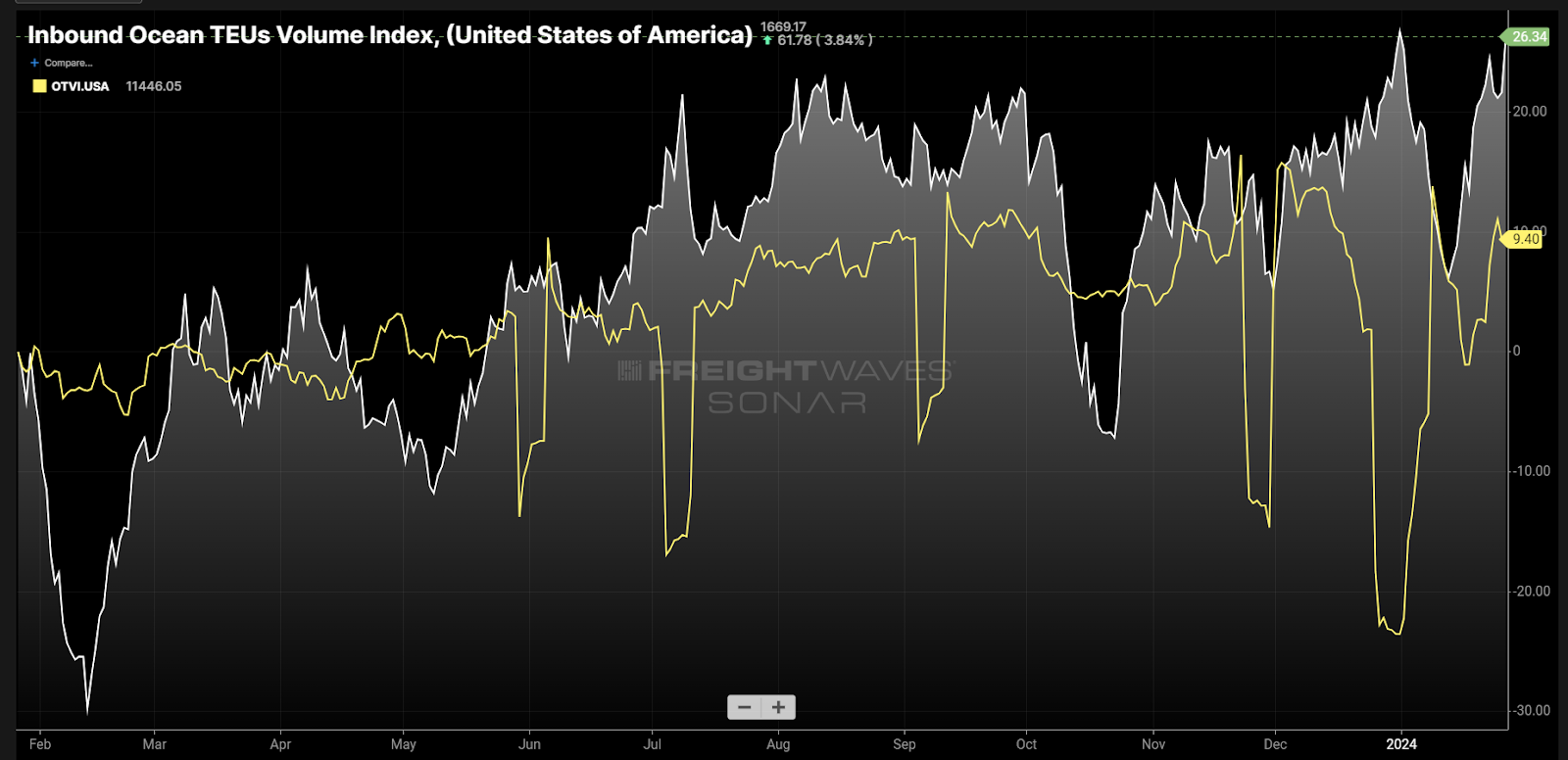

Looking at the same data over the past year the IOTI is up 26% and the OTVI is up 9.4% year over year, somewhat validating the GDP figure. So why are so many companies still struggling?

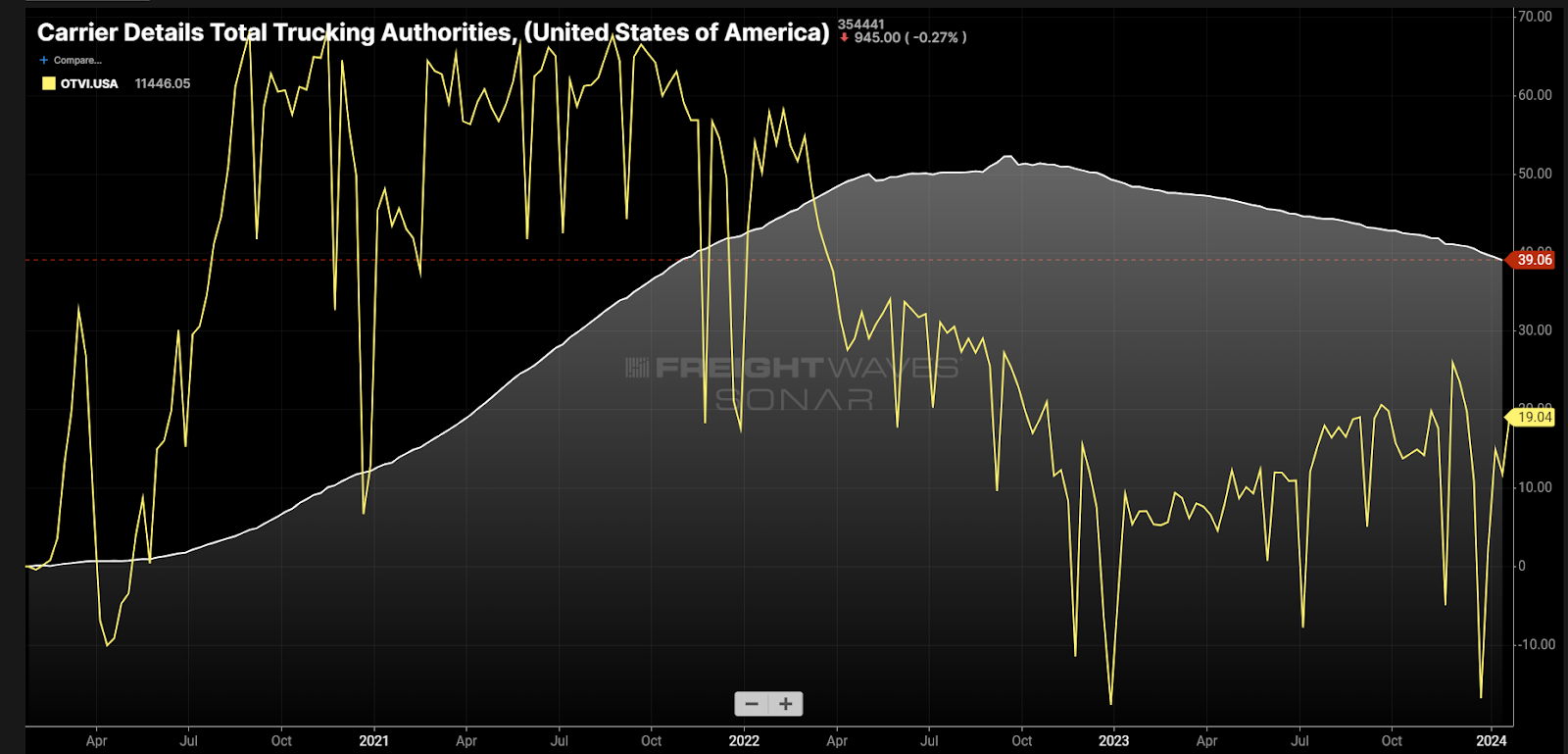

For transportation the answer is simple — oversupply. Not just standard oversupply, but capacity growth in nearly direct proportion to the demand growth in 2020-21.

Trucking operating authorities grew about 33% from January 2015 to January 2020. From June 2020 to June 2022, authorities grew 50%, nearly quintupling the previous five-year annual growth rate. Demand is down about 30% from 2021 highs.

This is analogous with many other industries that overbuilt or overadjusted their infrastructure to pandemic conditions. Solutions were created for temporary problems that no longer needed the same level of attention. Demand forecasts in many cases remain broken due to the noise created by one of the biggest black swan events in modern times.

In short, infrastructure — which in this case includes jobs and processes — changes much slower than demand, which has become less understood.

Yin and yang

The uneven distribution of positive and negative experiences has also helped make this economic environment so confusing. The services sector, which typically represents the majority of the GDP figure, had a booming 2022 as “revenge travel” hit. Subsequently, spending on goods waned.

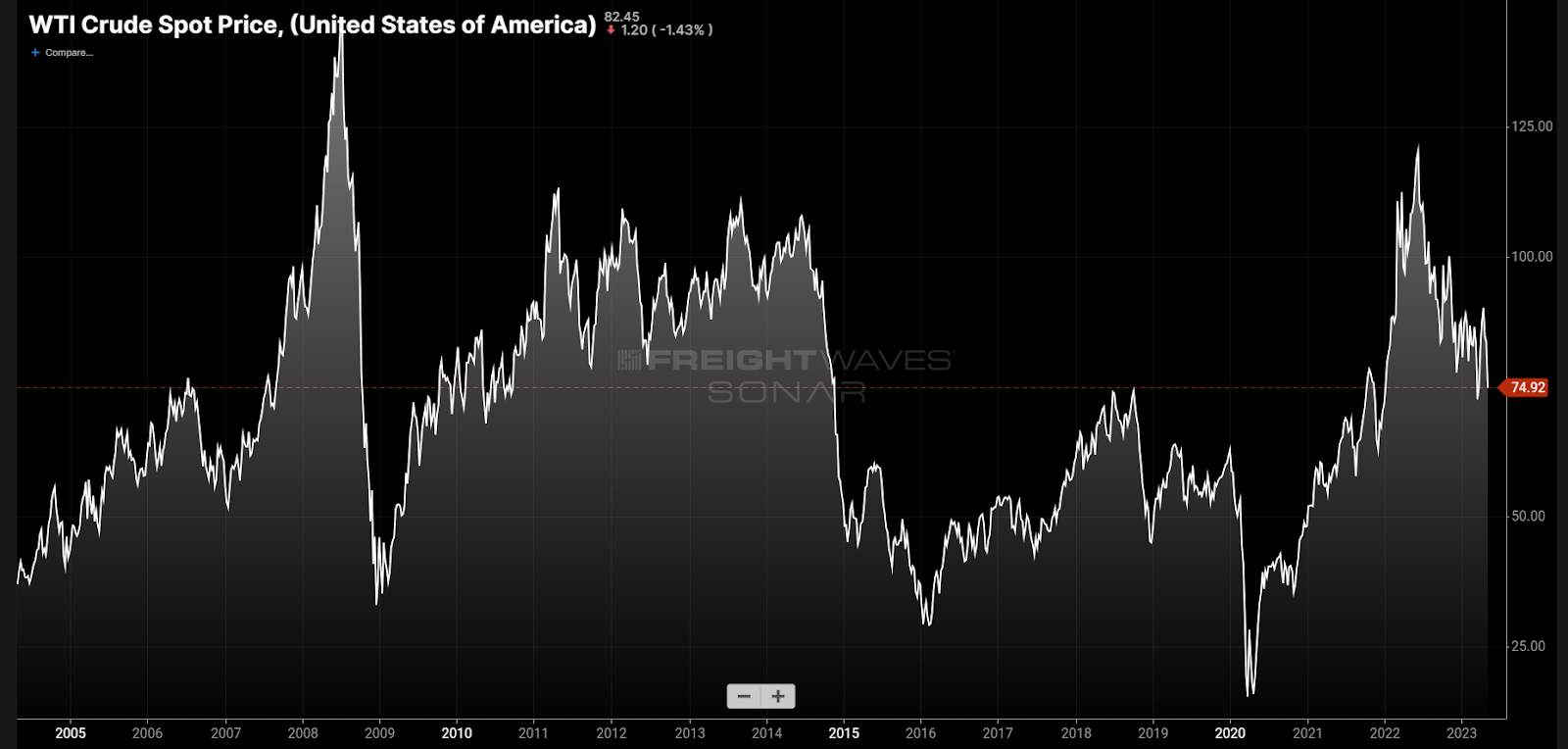

The automotive and energy sectors also felt a lagging response as their demand waned in 2020-21 but returned in force once people were set free. Recall the futures price for barrels of crude went negative in April 2020. The West Texas Intermediate crude spot price averaged just under $40 in 2020. It has averaged above $90 since 2022.

Before the pandemic, many of these sectors had well-defined relationships, which for the moment have been broken.

The positive takeaway is that the economy does appear to be stabilizing, though many sectors are still in distress. The steady demand growth over the past year in imports and truckload volumes bodes well for most sectors in 2024. The U.S. economy is driven by a healthy consumer.

Import bookings are a strong leading indicator as orders are placed weeks in front of expected fulfillment. Their weakness is in how long the goods stay in warehouses, but combined with tender volumes, that answer can be derived from how effectively that demand has been anticipated.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

To request a SONAR demo, click here.

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

Future of Rail Symposium

Reshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post • Chicago, IL Register NowReshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

The Signal at Chattanooga Choo Choo • Chattanooga TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now

Gary

Great read. As an independent O/O who’s been in this business for over 50 years, I was wondering how many of those Authorities are still active. I live in Indiana and see new startups gone in 6 months. I think people think this is an easy business and learn a quick lesson.