The two-year bull market for air cargo could be headed for a downturn. Freight volumes moved by passenger and cargo airlines contracted in March and April as manufacturing and supply chains faltered in the face of war and COVID headwinds, according to figures from a major airline trade group and independent analysts.

The International Air Transport Association said Tuesday air freight demand in March fell 5.2% year-over-year and that seasonally adjusted volumes reached a 16-month low. On Wednesday, Clive Data Services reported that global air cargo volumes in April declined 8% from 2021 after it previously reported a 4.5% drop for March.

IATA’s reporting lags Clive Data, which benchmarks air freight supply and demand using a different methodology and current transaction information instead of monthly weight-based statistics from airlines.

Both organizations attributed the air cargo slowdown to the conflict in Ukraine, COVID isolation measures in China that limited factory output and airport access, airport processing delays due to warehouse staffing shortages, and high inflation that is dampening consumer demand for goods.

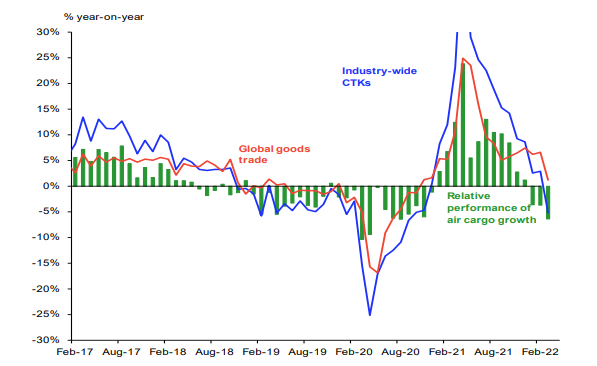

In its monthly report, IATA said the air cargo market appears to be heading for a downturn after growth decelerated from 6.9% in 2021 to 2.7% in January and February, with demand tracking below 2019 levels year-to-date. Cargo-ton kilometers this year have declined more than the drop in overall global trade.

Clive said April cargo throughput contracted 5% versus April 2019.

New export orders, a leading indicator of cargo demand, are shrinking in all markets except the U.S. The Purchasing Managers’ Index tracking global new export orders fell to 48.2 in March, the lowest point since July 2020. Export orders during the first quarter fell in Germany, Japan and South Korea, and shrank in China. The inventory restocking cycle that had started during the initial rebound from the pandemic in late-2020, and that led to businesses turning to air freight to rapidly meet demand, seems to have come to an end, IATA said. And economists are forecasting China’s economy will only grow 4% to 4.5% this year compared with 8% a year ago.

“The combination of war in Ukraine and the spread of the omicron variant in Asia have led to rising energy costs, exacerbated supply chain disruptions and fed inflationary pressure. As a result, compared to a year ago, there are fewer goods being shipped — including by air,” said IATA Director General Willie Walsh. “Peace in Ukraine and a shift in China’s COVID-19 policy would do much to ease the industry’s headwinds. As neither appears likely in the short term, we can expect growing challenges for air cargo just as passenger markets are accelerating their recovery.”

IATA said passenger traffic increased 76% in March from a year ago and is now down 41% from the pre-COVID level. International volume, which supports widebody aircraft that can also carry large amounts of cargo, grew 285%.

The dynamic load factor, which measures how much a plane’s payload capacity is filled by volume and weight, fell 9 points to 62% last month, Clive Data said. The load factor faced a difficult comparison because the 71% fill rate a year ago was exceptionally high.

Despite a 1% uptick in cargo space, the market remains at a 13% capacity deficit relative to pre-pandemic times, said Clive Data. Russia’s invasion of Ukraine led to a reduced supply of freighters serving Europe when Russian carriers were sanctioned by Western countries and Ukrainian cargo jets were destroyed or reallocated for humanitarian missions.

IATA measured the March cargo load factor in available tonnage at 54.9%, a 3.7 point decrease from a year ago. It follows a 4.9 point drop in February and highlights how weakening demand is chipping away at cargo yields. The trade association said interest in utilizing passenger aircraft for dedicated cargo service, common when passenger flying stopped because of the pandemic, has diminished in recent months in the face of weaker demand.

Capacity constraints support high rates

Lower volumes last month did not lead to lower overall air freight rates. April spot rates were nearly 2.5 times greater than in 2019 and even edged up from March. Air cargo prices were 26% more than the prior year, according to Clive.

The disconnect between demand, supply and pricing is well illustrated by the trade lane between North America and Northern Europe. Flight delays due to airport backlogs reduced effective capacity on the trans-Atlantic corridor despite an influx of more passenger aircraft for the busy summer travel season as airlines put COVID in the rearview mirror. Outsourced logistics providers say it can take more than 10 days in Europe between the time a shipment is booked and can get loaded on an aircraft. As reported on Wednesday, the combination of logistics snarls and airlines passing rising jet fuel costs to customers partially offset the lower-price environment due to looser market conditions.

Air cargo demand skyrocketed in the second half of 2020 as the global economy worked to recalibrate from pandemic shutdowns, but it leveled off for the better part of last year as measured by seasonally adjusted cargo-ton-kilometers. Now the sector appears to be contracting, according to IATA.

But there could be another explanation. Logistics managers say there is still substantial airfreight demand in many markets, including Singapore and the trans-Atlantic. That suggests freight bookings are strong relative to 2019 but aren’t getting measured in a timely way because of supply chain disruptions and airport backlogs that are squeezing what is actually carried on aircraft.

Glyn Hughes, director general of The International Air Cargo Association, said on The Loadstar podcast that high interest rates associated with inflation could actually benefit air cargo because companies that financed or prepaid orders may want to accelerate shipments so products don’t lose value stuck on the ocean, where transit times have doubled and tripled in the past 18 months.

European carriers reported the largest decrease of any region in March, with volumes down 11.1% vs. March 2021. The domestic market plummeted 19.7% due to the war in Ukraine. Labor shortages and lower manufacturing activity in Asia due to COVID outbreaks also affected demand, IATA said.

Demand among North American carriers dipped 0.7%. The trans-Pacific market declined significantly with seasonally adjusted volumes falling by 9.2% while capacity increased 6.7%. Middle Eastern carriers experienced a 9.7% year-over-year decrease in cargo volumes as the expected benefit of traffic rerouting south to avoid flying over Russia failed to materialize., according to the trade group.

Click here for more FreightWaves/American Shipper stories by Eric Kulisch.

RECOMMENDED READING:

Airport congestion masks softening in trans-Atlantic air cargo

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now