The U.S. domestic airline industry is moving toward recovery from the pandemic faster than previously estimated, although changes to route networks will make some destinations more difficult to reach for passengers and cargo shippers, according to analysts and executives.

Consumer eagerness to travel has some carriers predicting they will soon break even from an operating standpoint and some market analysts saying consensus growth projections are too conservative.

A report on Monday from management consulting firm Oliver Wyman said robust leisure travel will pull U.S. operations of domestic airlines back to pre-COVID levels by early 2022, months ahead of its prediction last fall, with lucrative corporate and international business severely lagging.

In mid-March, U.S. travel demand rose to more than 50% of 2019 levels — the highest it has been on a sustained basis since the start of the pandemic. Throughput at U.S. airports has topped 1 million persons per day for four weeks, with a rolling seven-day average of more than 1.4 million. That’s still 35% below the equivalent period in 2019 but double the amount of traffic in January.

The rapidly increasing availability of COVID vaccines — more than 55% of people over the age of 75 have been fully vaccinated in the U.S. with vaccine eligibility for all Americans moved up to April 19 — and relief checks from the $1.9 trillion American Rescue Plan are prompting people to book trips as the popular summer travel season approaches. Oliver Wyman now predicts that the U.S. will reach herd immunity by mid-June to early July — three to six weeks ahead of earlier forecasts.

“A year ago, we would have thought that a full domestic recovery in this timeframe for the U.S. was almost impossible, but the combination of pent-up demand, economic stimulus and access to vaccines is making a difference,” said Tom Stalnaker, a partner and global aviation practice leader at Oliver Wyman, in a statement accompanying the report. “We are still far from a full recovery for the overall industry, but we expect some of the airlines to start turning cash-flow positive in a matter of months, particularly in the U.S.”

The chief executives of Alaska Air Group (NYSE: ALK) and United Airlines (NASDAQ: UAL) said at a virtual aviation summit hosted by the U.S. Chamber of Commerce last week that March was the first time in the past year their airlines were cash-flow positive.

“Advanced bookings are strong, things are looking brighter as long as vaccine distribution continues and there are no big COVID waves again,” new Alaska CEO Ben Minicucci said.

“There’s going to be a jailbreak this summer. People are going to be going everywhere, whether they are driving, flying, taking the train or riding horseback,” said Neel Jones Shah, the head of airfreight for Flexport, an international logistics provider, and a former executive at Delta Air Lines (NYSE: DAL).

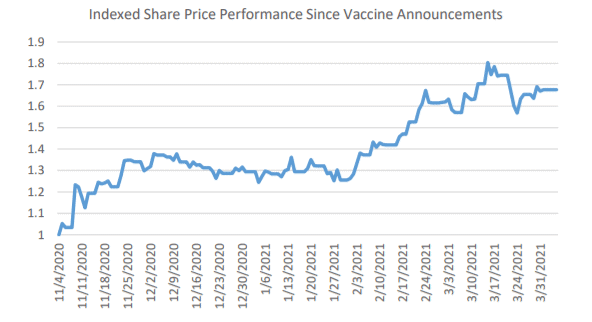

Airline stocks are up nearly 80% since the first COVID vaccines were approved late last year.

Some equity analysts are more bullish on domestic airlines because of the quick rebound in air travel, structural cost savings, accumulated spending power of consumers and the potential for the economy to catapult ahead. Forecasts for U.S. economic growth this year vary between 5% and 8%.

Most analysts see airline traffic returning to 2019 levels and then stabilizing there, but Morgan Stanley equity analyst Ravi Shanker argues the ceiling is actually much higher. He forecasts seat capacity to reach 2019 levels by the end of this year or early 2022 and a potential renaissance in travel similar to that after the1918 Spanish flu and World War II, although to a lesser degree because auto and air transport are more mature modes today.

“A strong consumer balance sheet with $2.3 trillion in excess savings could potentially fund this ‘golden age’ of travel. If consumers’ average 17% spend on transportation holds, that … excess savings could fund about $400 billion in excess revenues, roughly 2 times the entire revenue base of the U.S. airlines in 2019, although the airlines will get only a small portion of this spend,” he wrote in a recent research note.

Shanker projected passenger traffic could grow well above the normal 3% to 5% rate for several years — perhaps as much as 10% to 15%.

Corporate, international less rosy

But corporate and international travel levels are still more than 80% below normal, airlines report, and are not expected to bounce back until at least 2023. As of March, international capacity was still at only 29% of 2019 levels.

That’s a problem for air cargo shippers because more than half of available transport comes in the lower deck of passenger planes, especially large jets that crisscross oceans. Companies are experiencing a severe supply shortage at the same time orders for retail, manufactured and agricultural products are stronger than ever.

Globally, the airline industry lost $118.5 billion in 2020, with revenues down 40% to $328 billion. The International Air Transport Association projects that core operations won’t become cash-positive for the sector until next year because of new waves of infection in some parts of the world and government travel restrictions.

IATA on Wednesday reported passenger traffic in February fell three-quarters by comparison to 2019 and was even 2.5 points worse than in January. On the international side, passenger demand fell 88.7% from two years ago — a three-point deterioration from January and the worst performance since last July.

The lack of progress distributing vaccines outside the U.S., Israel, Chile, the United Arab Emirates, Serbia and the U.K. is expected to be a drag on international travel, experts say. Countries will reach herd immunity on different timetables and could negotiate relaxed restrictions on a bilateral basis. Analysts, including Oliver Wyman, expect normalization of international travel to 2019 levels to take until 2023 or 2024, depending on the destination.

United, Delta Air Lines and Hawaiian Airlines (NASDAQ: HA) are particularly exposed to countries with poor vaccination rates, but if an internationally recognized vaccine passport is approved it would accelerate recovery of cross-border travel, Cowen analyst Helane Becker said in a client note.

Oliver Wyman predicts companies will be slow to ramp up intracompany travel because of the success of videoconferencing and other remote work tools. In a recent survey, 58% of 1,000 U.S. respondents said they expected to continue to use videoconferencing as much post-pandemic as they did during COVID-19. Corporate travel budgets in the second half will be 45% lower versus 2019 and 15.5% lower in 2022, according to a Morgan Stanley survey. The shift to virtual work could reduce travel volumes by 25% next year, with respondents expecting 27% of meetings to be held in the virtual environment. McKinsey & Co. forecasts business travel will only recover to 80% of pre-pandemic levels by 2024.

Still, Shanker said that even if some portion of international and corporate travel is impaired long term, they only represent about 45% of unit capacity. Even a 20% permanent loss of business will only cost the industry 4% of international and 5% of corporate seat miles, and doesn’t account for new types of travel, such as remote employees having to travel to corporate headquarters on a regular basis.

Adapting to change

Worldwide, airlines have added domestic capacity at a much greater rate than international capacity as travel between countries remains relatively restricted. Airlines with large domestic markets, such as the U.S. and China, have benefited. In Europe, most domestic and nearby-international travel is done by train, bus or car.

Schedule data indicates U.S. airlines might be getting more aggressive about adding back international capacity, anticipating a return to foreign travel with the proliferation of vaccines. However, if precedents hold, the advance schedules will likely be reduced the closer they get to departure dates, given how airlines have been managing close‑in capacity for the past 12 months, Oliver Wyman said. Matching capacity to uncertain demand during COVID is very challenging, but U.S. airlines are getting better at anticipating COVID-19 conditions. Capacity for schedules in mid-December, for example, only had to be reduced 9.6% compared to 56% in mid-June.

The loss of revenue from high-yield customer segments — representing more than half of profits and a third of revenues — has full-service airlines copying low-cost carriers to compete for more of the leisure market. These airlines are starting to sell more services a la carte and offer similar fare structures to reach a broader customer base that is less willing to pay a premium, according to the consulting firm.

“While all types of carriers will face shrinking margins for the next several years, pressure will be the greatest on full-service carriers and international carriers. With the market unable to quickly make up for lost growth, these network airlines will be increasingly forced to shift their strategies toward those of value carriers by appealing to more price-sensitive customers looking for deals,” the report said.

To cut overhead and improve efficiency, airlines will have to adjust schedules, reduce unprofitable routes and shrink the overall size of networks, it added. More savings could be had if airlines reduce ground time between flights, which will be possible with less airport congestion.

Other experts say airlines will need to adjust pricing strategies for business and premium seating to target more leisure travelers.

Airlines removed half the global fleet from service at the height of the pandemic and are mostly returning narrowbody aircraft because of travel constraints. There will be fewer widebody aircraft available for the near future, which will reduce cargo capacity for international trade. With the increase in widebody retirements and storage, the share of narrowbody aircraft has increased two points — significantly more than in a typical year, Oliver Wyman said. Widebodies have maintained a consistent fleet share of close to 20% over the past decade, but that is expected to drop about two points over the next decade, with average annual growth of just 1.6%.

Lower business travel may require the use of larger aircraft, such as the Boeing 777 or the Airbus A350 — flying less frequently compared to the earlier trend of using small-size widebodies like the Boeing 787 to fly between hubs and smaller cities, the McKinsey analysts said.

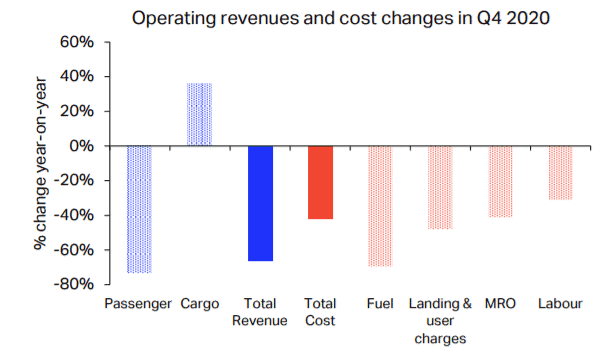

The 11 domestic carriers in the Oliver Wyman study slashed costs by 41% last year, mostly because reduced flying meant lower fuel consumption and maintenance, but unit costs increased significantly — 127% for network carriers — because it was difficult to remove enough overhead to match lower capacity.

Airlines also furloughed thousands of employees, but now there are questions about whether airlines will be able to staff up fast enough to take advantage of the return in demand. Delta, for example, on Sunday had to cancel 100 flights because of staff shortages.

Domestic demand could outpace near-term supply as airlines work to bring back aircraft and crews, which could result in higher short-term prices, McKinsey said.

Beyond the U.S., domestic travel has also recovered in China, South Korea and Vietnam because of aggressive COVID health measures that contained the virus.

Debt drag

The good news on travel and cash flow for airlines is tempered by the fact that they borrowed heavily to stay afloat last year. The industry collectively amassed $180 billion in debt, including nearly $60 billion in financing by U.S. carriers, according to airline trade associations. They will have to use that cash to pay off debt and could feel pressure to maintain greater cash reserves for a rainy day, which will put pressure on margins for several years and limit ability to invest in growth opportunities, airline officials and analysts say.

Repaying loans is made even more difficult by worsening credit ratings and higher financing costs. McKinsey says airlines will raise ticket prices 3% to help cover that debt.

And airlines will continue to burn cash this year, with extra costs associated with retraining pilots who have not flown for a considerable time and getting aircraft flight-worthy after storage, Alex Dichter, McKinsey’s senior practice leader for travel, logistics and infrastructure, said in a separate presentation. By 2024 the industry could have used between $870 billion and $1.1 trillion in cash.

Low passenger load factors make it difficult to cover the full cost of operating an aircraft and rising jet fuel prices mean airlines will continue to burn cash even as the industry starts to recover, new IATA Director General Willie Walsh said Wednesday during a news briefing.

Click here for more FreightWaves/American Shipper stories by Eric Kulisch.

RECOMMENDED READING:

Airlines, pilots plead for more federal aid to retain workers

$1,400 COVID relief checks to stimulate surge in e-commerce shipments

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now