You wouldn’t think investors would race to commit tens of billions more in cash to build even more liquefied natural gas (LNG) export terminals across the globe when the price of the commodity had sunk to extreme lows.

But they are. Massive LNG export investments continue to pile up at historically unprecedented levels, faster than previously expected.

The momentum in LNG export investments has long-term implications for coal, which competes with natural gas in the power-generation sector. In July, Morgan Stanley issued a special report warning that “a long-term structural shift in global commodity markets” had accelerated in favor of LNG at the expense of coal.

The LNG export terminal trend is a negative for U.S. rail transport, given the likelihood that LNG exports will increasingly supplant coal exports over time. Concurrently, low LNG pricing reduces U.S. domestic coal consumption, another headwind for rail carload demand, which has already fallen by 24% over the past five years.

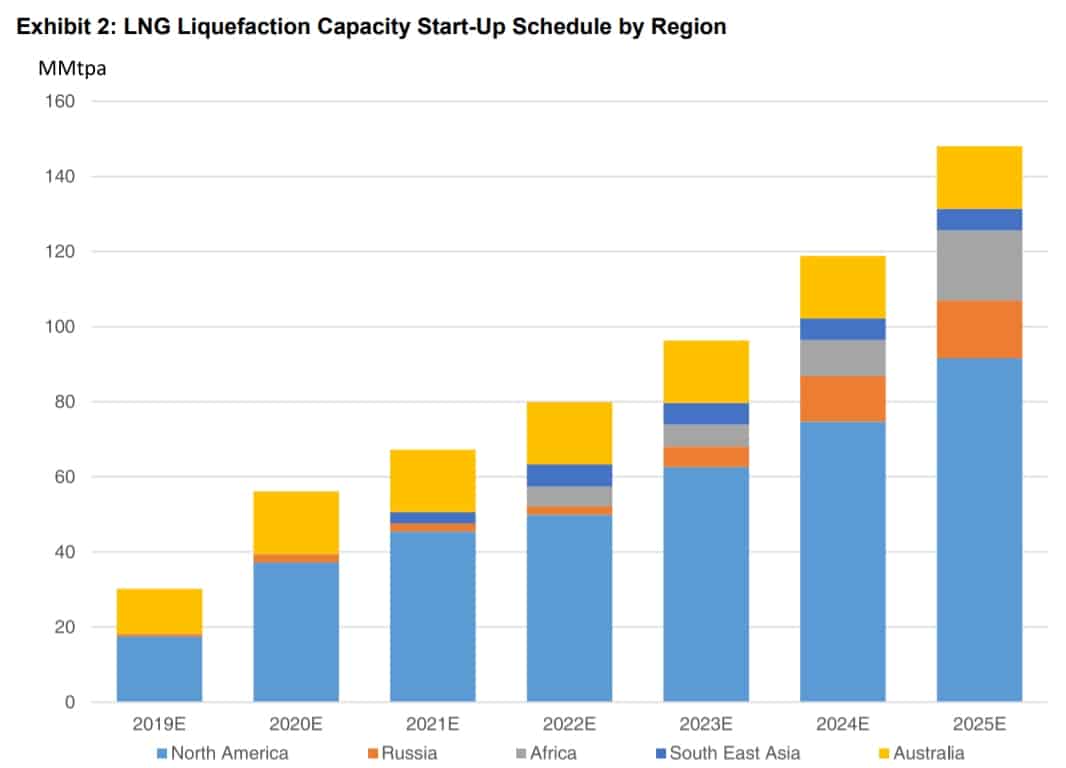

Looking forward, the bellwether to watch is LNG final investment decisions (FIDs). The latest mega-project FID came on Sept. 5 for Russia’s $21.3 billion, 19.8 million tons per annum (mtpa) Arctic LNG 2 project, a development that was not expected to reach FID this soon. Following that announcement, Stifel analyst Ben Nolan proclaimed 2019 to be “the year of the FID” and cited “a dramatic increase in new LNG project sanctioning.”

Deutsche Bank analyst Chris Snyder asserted that “industry-wide FIDs have accelerated sharply, with 2019 now by far the strongest year on record for global LNG project sanctioning. The industry has now sanctioned 64 mtpa of LNG projects in 2019, 20% more than the previous four years combined.” This year’s tally has “smashed” the previous record, he said.

There’s little debate on the growth potential of LNG; the outlook is unanimously bullish. However, predicting the balance between natural gas and coal in the power-generation market is complicated. It’s far too simplistic to say more LNG FIDs equals less coal equals less coal transport. There are major variables in terms of the time it will take and in which markets it will happen.

For perspective, FreightWaves interviewed Madeline Jowdy, senior director of global gas and LNG at S&P Global Platts. She explained why the conversion from coal to natural gas, at least in Asia, is not going to transpire overnight, despite currently very low gas prices and the latest wave of export project FIDs.

Why cheap LNG doesn’t halt FIDs

Jowdy offered two reasons why very inexpensive LNG commodity pricing has not stopped the FID parade.

First, developers have an inherently long-term pricing perspective. “It’s true that prices are very low and our outlook is for prices to remain low through the third quarter of next year. But the projects making FID this year – these have been in the works for the past five years,” she said. The developers are not focused on current pricing, but rather, “they’re eyeing the next period of tightness when demand catches up to supply.

“Just because the prices are so low now doesn’t mean they’ll be low forever. Don’t forget, less than a year ago the price in Japan was around $15 per MMBtu [million British thermal units; the latest price is around $4.40 MMBtu].”

The second reason the FID pace has been generally unscathed by low LNG pricing relates to who is greenlighting these projects. In the past, developers were largely independent companies that required long-term sale and purchase agreements (SPAs) for the LNG export volumes to obtain project financing.

Low pricing makes getting SPAs more difficult. As Nolan noted, “With so many projects scheduled to come online, including many internationally – and as a consequence, market expectations for temperate LNG pricing – the buyers have lost urgency in committing to long-term purchase agreements.”

But now, the developers making FIDs are increasingly oil majors who do not need SPAs to get financing. According to Jowdy, “We’re in a very different world now from the traditional world where you had to have your SPAs and long-term contracts to get the financing. That was the conventional way that things worked and is still the case for a lot of the projects being planned, including most of them in the U.S.

“If you look at the FIDs we’re getting now, including Canada LNG and Golden Pass and Arctic LNG 2, you’re seeing more of a play by the international oil companies and state oil companies who are essentially trying to regain market share they’ve kind of lost over the years to companies like Cheniere.

“We now live in an emissions-reduction world where oil companies are seen as pariahs, so they’re moving toward gas. They want to be energy companies, not oil companies, and they want to de-emphasize fossil fuels and gas is seen as the lesser of two evils. Companies like Exxon, Shell and Total are willing to take a lower rate of return from these gas projects, because they’re basically financing the next generation of energy.”

LNG prices vs coal prices

Asked by FreightWaves about the expected trend in LNG pricing and how it could compare to coal pricing, Jowdy responded, “If we are in a world where companies are making FIDs without having long-term associated contracts – and it appears we are – then these companies are ultimately putting LNG in the market that doesn’t necessarily have a buyer, which would probably depress prices.”

Nevertheless, coal is still cheaper, she explained. “What we’re talking about is LNG becoming more competitive with coal, but we’re still not at the point where it will be competitive based purely on cost. You still need some sort of policy measures or carbon pricing.

“LNG is still the premium fuel and the biggest challenge is you have to transport it and you have to liquefy it [to allow it to be transported] and that costs money,” said Jowdy.

There are also political, business and labor interests that support coal consumption even when LNG would be more effective. “We [at S&P Global Platts] spend a lot of time looking at the coal-to-gas question and we have seen examples where it should have happened and it hasn’t. The problem is that there are entrenched interests [supporting coal], including labor, that need to be kept happy.”

European coal-to-gas conversion

One market where coal-to-gas conversion has already occurred in a big way is Europe. This trend is particularly important to the U.S. coal industry and its transport partners, because Europe has traditionally been a major buyer of U.S. thermal coal exports.

“In Europe, there is policy [support], which began in Germany and filtered out from there, and you also had this immediate effect when the price of global LNG collapsed starting in October 2018. After that you saw Europe switch from coal to the point where there’s not a whole lot of coal left to be substituted for.

“Europe hasn’t switched 100% to coal but basically, it has for the least-efficient coal. All of the low-hanging fruit is gone and even some of the harder, more intractable, politically sensitive coal [has been substituted],” Jowdy said.

There remain pockets of resistance. For example, there are challenges to LNG volume growth in Eastern Europe due to a lack of import infrastructure in countries such as Poland, as well as a general aversion to Russian gas, which is supplied by both pipeline and as LNG from Russia’s Yamal project. “Eastern European countries have a strong desire to wean themselves off their dependence on Russian gas,” she noted.

Asia coal-to-gas conversion

From a volume perspective, the real game-changer for natural gas and coal demand would be power-generation substitution in Asia.

So far, Jowdy sees relatively limited government policy support in Asia to facilitate the shift to natural gas. “There are some policy mandates in China, but the only place in Asia where you have carbon pricing is South Korea, and even though there’s a coal tax in South Korea, you still don’t see coal-to-gas substitution.”

Two factors are likely to slow the coal-to-gas timetable in Asia. First, the cost of building out the necessary infrastructure to replace coal with natural gas is very high. “The fact is, renewable pricing has come down so much that in a lot of these countries, they might just go right [from coal] to renewables. If you are a policy maker and you have to build out all your infrastructure, the investment in renewable technology could be more competitive given the cost of building out all the pipelines and securing land rights and all those sorts of things [to accommodate LNG].”

The second hindrance is that many Asian countries do not have the same perspective on environmental policy as European countries, given the less developed nature of Asian economies. As Jowdy put it, “A lot of these countries have their own coal and in places like India, Indonesia, Malaysia and China, people say, ‘We just want electricity and we’re not going to pay a premium for gas to get it. We’re electrifying here. We’re moving out of poverty. We just want to have the lights on so we can study and cook.’”

Tempered transition timetable

The key takeaway is that the relatively swift, policy-supported transition from coal to natural gas in Europe will not follow the same course in Asia.

“I think we could see that [in Asia], but you are talking 5-10 years out as opposed to next year,” she said. “In general, we see LNG becoming a bigger part of overall natural gas growth, but because of all of these competitive factors and other factors, when you look at the bigger energy picture, we think gas growth in the longer term will be slower and steadier.”

The outlook for coal remains daunting and this year’s surge in LNG FIDs, including the most recent mega-project approval in the Russian Arctic, is clearly a negative. Yet the demise of coal will take longer than some believe. Jowdy noted, “The focus of many of these countries in Asia is on just getting electrified, and if you look at power-plant construction plans globally, only about 40% of them are for natural gas – 60% of them are still for coal.” More FreightWaves/American Shipper articles by Greg Miller

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now