Oil prices are continuing their enormous decline on the gradual reopening of the Strait of Hormuz and other policy changes, with possible setbacks in those occurrences making little impact on the pace of the slide.

The fall in futures prices led up to the release Tuesday, price effective Monday, of a decline in the weekly average retail diesel price published by the Department of Energy/Energy Information Administration. The latest price is $4.832/gallon, a decline of 22.7 cts/g from a week earlier.

That price is the basis for most fuel surcharges.

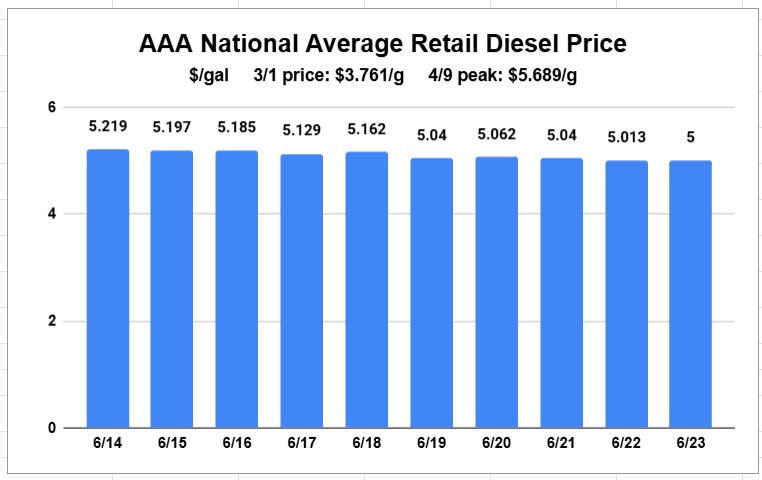

(There remains a significant inconsistency between the DOE/EIA price and that of the AAA. The vehicle owner-oriented group reported an average retail diesel price Tuesday of exactly $5.)

The latest DOE/EIEA price is the first one less than $5/g since March 9, which was also the initial number to show the impact of the Iran war. It’s also the seventh consecutive decline. The slide during that period is 80.8 cts/g.

But the benchmark price is still up about 94 cts/g from where it was before the war started.

The decline in retail prices, as usual, is chasing the fall in futures prices.

With a settlement Monday of $3.0931/g on the CME commodity exchange, ultra low sulfur diesel (ULSD) has fallen almost 52 cts/g since a recent high settlement on June 10 of $3.6126/g. At approximately 9:40 a.m. EDT Tuesday, ULSD was down just over 4 cts/g to $3.0530/g, a drop of 1.3%.

Since the start of fighting on February 28 into March 1, ULSD has settled less than $3/g just once: the first trading day after that weekend when the shooting began.

The highest settlement since the start of military action against Iran by the U.S. and Israel was $4.6084/g on March 20.

Market not swayed by uncertainty

Even news over the weekend that looked like the peace deal that would reopen the Strait of Hormuz might be in trouble had little impact on the trend of falling prices. After a brief surge when futures trading began Sunday night U.S. time, ULSD and the entire oil complex went back to lower numbers.

While there are still strong voices cautioning that the loss in supply through the Strait for all those months will eventually come back to haunt buyers in the form of higher prices, those that buy and sell oil do not seem concerned.

A lower forecast at BOA

Nor do Wall Street analysts. For example, the commodities research team at Bank of America Merrill Lynch (BOA) recentlyreduced its forecast for the average price of Brent, the world’s crude benchmark, to $82/barrel. It had been $93/b.

But even that report didn’t sound completely convinced higher prices may not be a possibility.

With an average Brent price of about $90/b in the first half of the year so far, according to the BOA report, “this means that Brent would likely have to trade in the $70-80/bbl range for most of 2H26, but but volumes lost over 100+ days top 1.3 billion barrels.”

“Clearing mines and restoring flows to normal levels is likely to take months, not days, given the logistical challenges, implying that oil markets could remain in deficit until 4Q26,” the report said. “We estimate that production losses since the start of the war have averaged 11–14 mn b/d, with the supply gap being covered by demand rationing and inventory draws. These losses have made the Iran war the largest supply disruption on record, exceeding the Iranian Revolution in 1979 and the first Gulf War in 1991.”

But even with those facts and other bullish factors like the need to restock inventories, a tighter market in 2027 would still see Brent average $70/b, BOA said, “if the peace holds.”

The research team echoed a recent International Energy Agency report that said the surplus that was to be in effect this year before the war will reemerge next year to the tune of about 1 million b/d. The restocking needs will help keep the price about $70 even though that surplus would otherwise push prices lower, according to the BOA analysis.

The road to more supplies coming on to the market, volatile already because of the lack of consistency so far in keeping the Strait of Hormuz open, is likely to be up and down for some amount of time.

A flood of Iranian crude

For example, Bloomberg reported Monday that Iranian crude has been “flooding on to the global market again.” It’s been able to have those supplies rise because of the end of the U.S. blockade on exports, and is likely to get a boost also from the end of various U.S. sanctions on exports.

“More than 30 million barrels departed for Asia in the past week — a mix of crude that had been blockaded by the US, and exports from Kharg Island, the nation’s top export facility in the northern Persian Gulf,” Bloomberg reported Monday.

But as an example of the inconsistency that could make the road to normalcy far from easy, Bloomberg also reported that “ultimately, because the gush mostly reflects a clear-out of cargoes that were blockaded, the export rate will drop again. Shipping rates of 2 million barrels a day are high for Iran in recent years.”

More articles by John Kingston

One crash, 3 trucking firms found liable in California nuclear verdict

Wabash stock soars as analyst cites management bullishness

After a five-year wait, C.H. Robinson makes a broker acquisition

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now