Container shipping is having its best year ever and dry bulk shipping its best since pre-financial crisis. Crude-tanker shipping is having its worst year since the 1980s.

Tanker executives speaking on conference calls and analysts writing in client notes continue to highlight the green shoots, yet earnings remain stubbornly and deeply in the red.

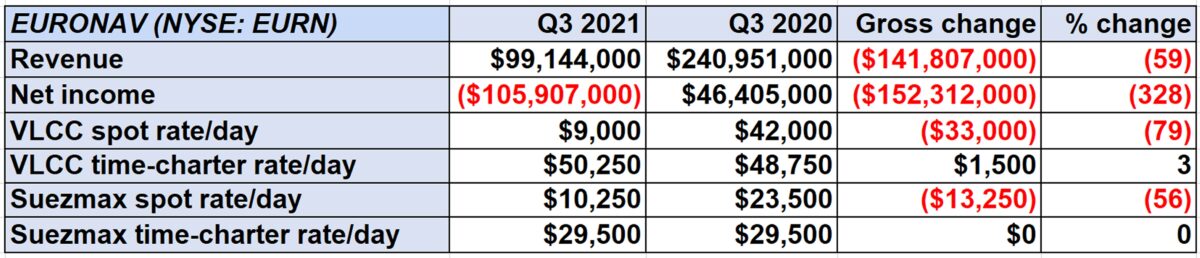

On Wednesday and Thursday, tanker owners reported huge losses for Q3 2021: Euronav (NYSE: EURN) lost $105.9 million, Teekay Tankers (NYSE: TNK) $52.1 million and DHT (NYSE: DHT) $21 million.

The fourth quarter looks like more of the same, albeit less bad. During the past year, multiple analysts had predicted a rebound by now, but the recovery forecast has been pushed back to sometime in 2022.

Timing the recovery

When tanker owners expect a weak quarter, they bring forward drydocking schedules for maintenance and equipment installations and put ships in the yards. Why have tankers in service when they’re not going to earn, and why have them out of service in the future when you think they will earn?

DHT had 85 off-hire days from tanker drydocks in the third quarter. Underscoring a lack of confidence in the current period, off-hire will be even higher in Q4, at 100-125 days. “We have taken advantage of the weak spot market to bring forward drydockings,” said DHT co-CEO Svein Moxnes Harfjeld on the call with analysts.

Teekay Tankers CEO Kevin Mackay said on his company’s call, “To optimize vessel utilization in anticipation of a tanker market recovery [in 2022], we have tactically brought forward four additional drydockings into the fourth quarter.” That brings its total drydockings in Q4 to five, the same as in Q3, a period when rates were historically low.

Evercore ISI analyst Jon Chappell — who admits to calling the recovery too early himself — foresees “decelerating losses” for Euronav. “We still forecast losses, though moderating, for each of the next four quarters, but we now believe the risk is skewed to the upside.”

Stifel analyst Ben Nolan also puts the crude-tanker recovery in late 2022. In a client note on DHT, he maintained that the market “has likely bottomed but is not yet close to the tipping point.” Nolan said that Stifel “is modelling a slow build in rates until about this time next year, when normal seasonality could pair with underlying improvements in supply and demand, resulting in much better tanker rates.”

According to Mackay, recovery timing remains extremely unclear. “I think calling the actual inflection point is futile, because nobody really knows when this thing is going to turn,” he said.

Rates finally rising

“Unlike other industrial and shipping sectors, the late-cycle nature of tanker shipping means that we have yet to regain the pre-COVID levels of consumption that other sectors are already enjoying,” said Brian Gallagher, head of investor relations at Euronav. But he stressed, “There are some very strong fundamentals from 2022 and 2023 onwards.”

Among the green shoots: Spot rates are up for very large crude carriers (VLCCs, tankers that carries 2 million barrels), albeit still below cash breakeven. “There have been single voyages and round-trip voyages being delivered at $20,000-plus a day over the last few days. The [upward] trajectory has continued,” said Gallagher.

Citing the same rate levels, DHT’s Harfjeld said, “At this pace, you will have profitable levels not too far out.” Cash breakeven levels vary from company to company; Clarksons Platou Securities puts the all-in cash breakeven rate for a 5-year-old VLCC at $32,000 per day.

There is also more inquiries for time charters, a positive bellwether. “There is definitely more interest on the time-charter front,” reported Harfjeld. “Whether it’s traders or end users … I think this is simply a reflection of their view on the market and the expected activity they will have. And I think that [time-charter interest] is a leading indicator.”

Restocking inventories

Another positive indicator: Oil inventory levels are now well below normal.

Teekay’s Mackay said that a key reason for historically bad tanker spot rates in 2021 is that “global oil production has trailed demand for most of the year, resulting in a large drawdown of global oil inventories. The tanker market is linked to the oil inventory cycle, as drawdowns essentially displace oil imports.”

According to Gallagher, “Global oil inventory is now way below the five-year average to the end of 2019. At some point, the inventory build will have to begin and inventory builds have strictly been very positive for tanker markets.”

OPEC+ production gains

Yet another green shoot: OPEC+ production cuts continue to slowly unwind and are increasingly translating into tanker volume.

“It has been frustrating that production rises in global crude have not always translated into like-for-like increases in export barrels, but this feature has started to change,” said Gallagher. He noted that crude exports from the Persian Gulf increased to 550,000 barrels per day in September, then to 700,000 in October.

Vessel supply upside

The next piece of the recovery puzzle is on the vessel supply side.

Another reason rates fell to near or even below zero this year was that previously ordered newbuilds continued to deliver at the same time inventories were drawn down and demolition (scrapping) of older tankers declined.

“During this period, we have seen the fleet grow,” said Harfjeld. “We have more ships today than we had pre-COVID, so there is an imbalance in the market, and scrapping has been very, very minimal, as quite a lot of the older ships have been engaged in the shadier trades.” (By shadier trades, he is referring to the use of tankers to move sanctioned oil, primarily from Iran to China via ship-to-ship transfers off Malaysia.)

But the tide is turning. Orders of new tankers have collapsed. “New tanker ordering ground to a virtual halt in the third quarter with just 0.8 million deadweight tons of orders placed, the lowest quarterly total since the second quarter of 2009,” said Mackay.

“Elevated newbuilding prices, which are currently the highest since 2009, are expected to limit further newbuild orders in the near term. Meanwhile, shipyard availability is becoming increasingly scarce, as record container-ship ordering has filled shipyard capacity well into 2024.”

There is also good news regarding the “shadier trades,” meaning that more VLCCs are finally going for scrap.

According to Euronav CEO Hugo de Stoop, scrapping decisions have been “polluted by the fact that people were willing to pay a premium for very old tonnage” — a premium of $1 million-$3 million over scrap value — “to transport Iranian oil.” Sanctioned oil is sold at a discount and earns premium shipping rates to compensate for the risk.

De Stoop said that “there has been so much tonnage bought for this trade that it is now oversupplied. With the last couple of ships we have seen presented for either scrapping or for sale, there were no bids beating the scrap price, and therefore they went for scrap, which is a signal that the appetite for these ships from these [sanctioned oil] traders has vanished.”

Put all of these green shoots together and the message from the DHT, Teekay and Euronav calls was unanimous: Q3 2021 was the trough and, knock on wood, the worst is behind us.

Tanker earnings roundup:

Click for more articles by Greg Miller

Related articles:

- Shipping shares in sea of red as broader stock market rises

- Why this tanker shipping depression is different from past slumps

- Yet another worry: Price of ship fuel is now highest since 2014

- What is the shipping cycle — and can it ever be tamed?

- Minus $7,400 a day? How can shipping rates fall below zero?

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now