Danaos Corporation (NYSE: DAC), a lessor of container ships, has reported a sizable increase in quarterly profits and maintained that escalating trade tensions should not curb chartering demand.

The company, which underwent a major debt restructuring that was concluded in August 2018, reported net income of $33.4 million for the first quarter of 2019, compared to net income of $15 million in the same period in 2018. Adjusted net income, excluding non-cash items, came in at $38.6 million, up 38 percent year-on-year.

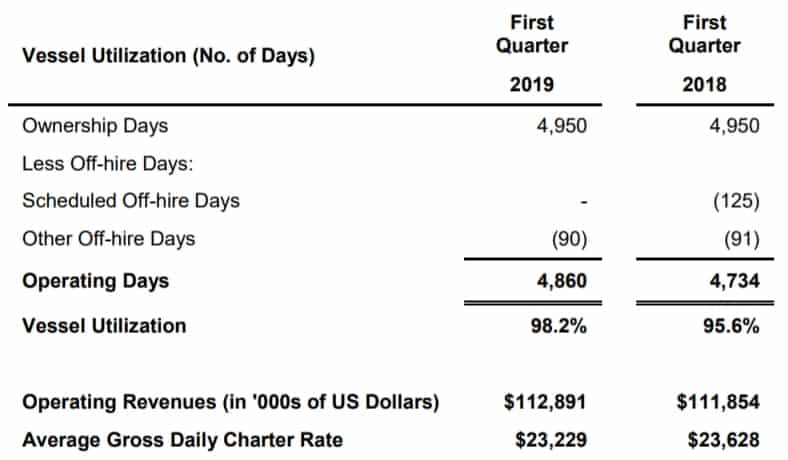

Danaos and its joint venture Gemini Shipholdings own a fleet of 59 container ships with total capacity of 351,614 twenty-foot-equivalent units (TEU). The average gross charter rate it obtained in the first quarter of 2019 was essentially flat year-on-year, at $23,229 per day, with the improvement in adjusted net income largely driven by lower interest costs following the debt restructuring.

Danaos is in the business of employing container ships on a mix of long- and short-term charters with liner companies that deal directly with containerized cargo shippers. Its U.S.-listed peers include Seaspan Corporation (NYSE: SSW), Costamare (NYSE: CMRE) and Global Ship Lease (NYSE: GSL).

During the company’s conference call with analysts on May 14, Danaos chief executive officer John Coustas was asked how the business model of container-ship lessors like Danaos would be affected if there was no trade deal between the U.S. and China in 2019.

“I don’t think we will have any changes,” responded Coustas. “If cargo is sourced from China, at least in the short- and medium-term, I think it will continue to be sourced from there – until an alternative has been located.”

Coustas explained further, “In general, most of the other alternatives to China are also in Asia, so it’s not going to change the actual TEU-miles for that cargo.” TEU-miles and ton-miles are measures of vessel demand calculated by multiplying cargo volume by distance traveled, taking into account that longer trips soak up more ship capacity.

As long as the U.S. keeps sourcing its containerized imports in the Pacific Basin, demand for container vessels, and thus for the chartering product of companies like Danaos, should remain the same. In contrast, charter demand would fall if the U.S. starting supplanting imports from Asia with domestic production.

Coustas acknowledged this risk, but claimed it was unlikely. “I don’t think this will be the case, because everybody knows this issue with the tariffs is a relatively short-term issue. Maybe it will be a year until trade concerns have been resolved. So, no one is going to invest in producing things in the U.S. that are presently made in China,” he opined.

If there is a risk to container-ship charter rates, it may arise from sentiment. When market pessimism is high and charterers fear for the future, they may lower their rate offers even before cargo volumes decline. According to Coustas, “The only thing I think we’ll see [from the trade conflict] is some kind of psychological issue that might reflect on demand, but not the actual traffic.”

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now