Manufacturers’ new orders for durable goods tumbled in April, driven by a reversal in commercial aircraft orders. This is the latest in a series of disappointing releases from manufacturing, and raises some questions about the health of one of the key drivers of freight demand given recent developments in trade policy.

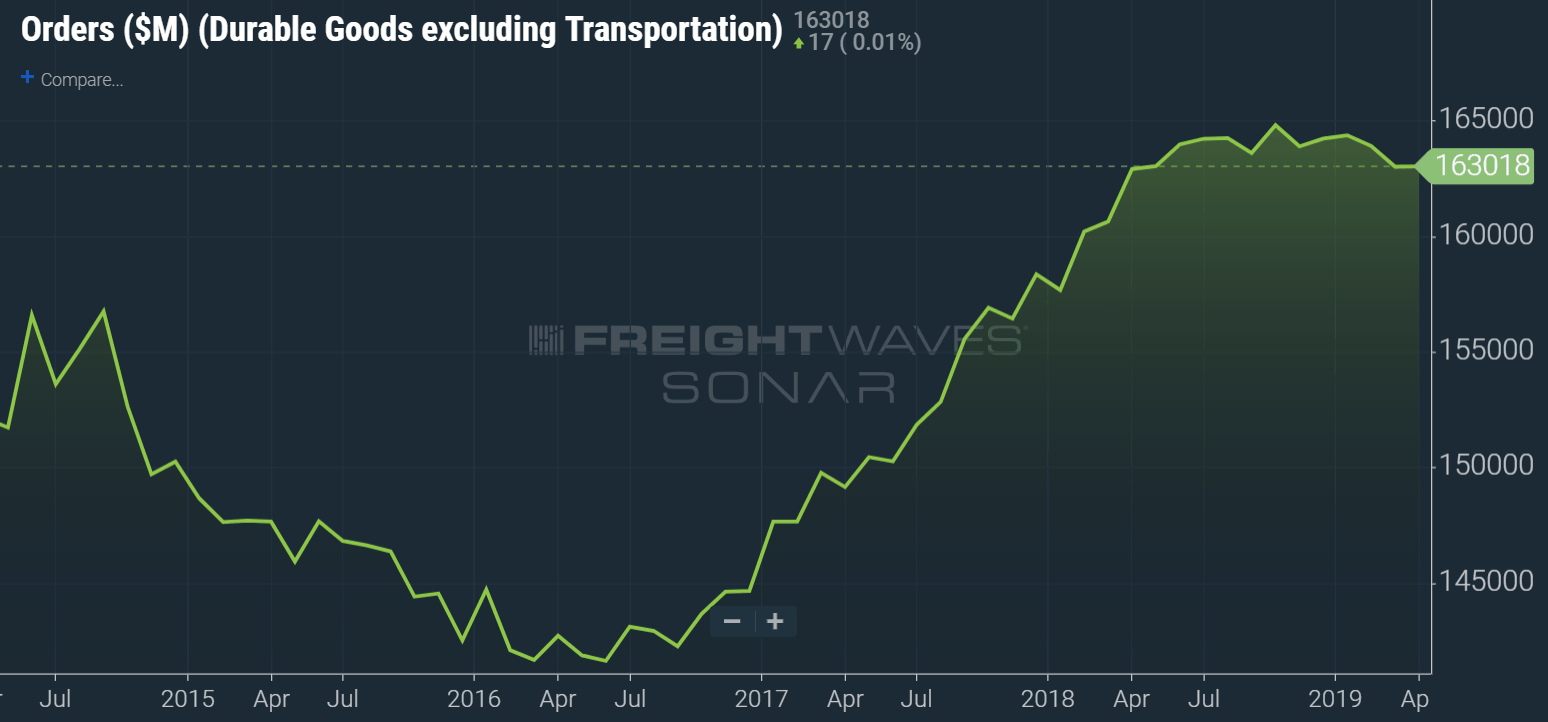

The Census Bureau reported this morning that manufacturers’ new orders for durable goods fell 2.1 percent in April from March’s levels. This reverses the 1.7 percent increase in the previous month and marks the second large decline in the past three months. The wild swings in orders over the past couple of months have been caused by fluctuations in the volatile transportation equipment component, which often experiences non-seasonal surges in aircraft orders. Excluding transportation equipment, durable goods orders actually were essentially flat during the month as year-over-year growth fell to 0.1 percent. Core capital orders, which are a proxy for business investment spending on equipment, fell by 0.9 percent during the month.

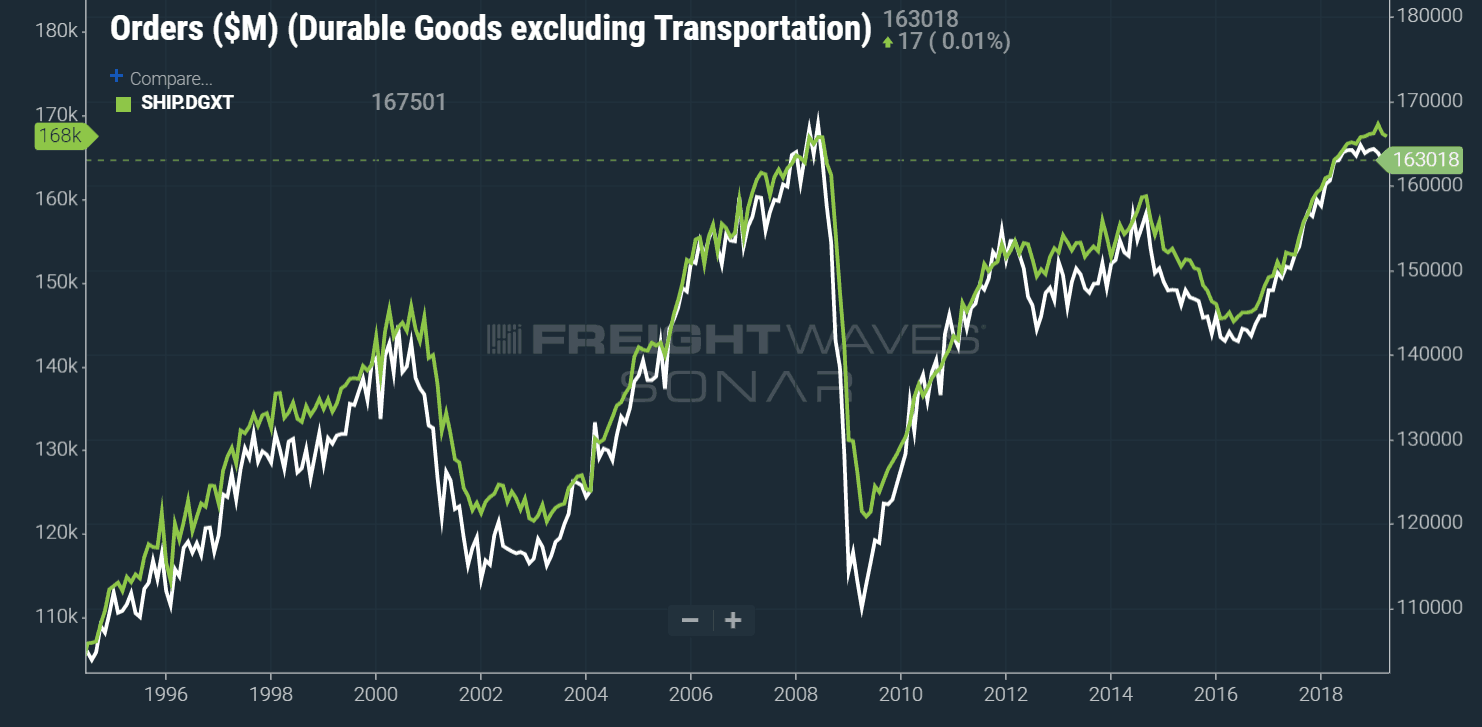

Durable goods orders serve as a useful leading indicator of future durable goods shipments, typically leading shipments in the economy by one to two months. Orders excluding transportation have essentially flatlined since the second half of 2018, heightening concerns over the future strength of manufacturing activity. Durable goods manufacturing was one of the standout areas in terms of industrial output throughout most of 2017 and the first half of 2018, and the recent slowdown in durable goods production has been one of the causes of the overall sluggishness in manufacturing in recent months.

More manufacturing softness

The results from durable goods orders are just the latest in a string of weak results emerging from the manufacturing sector over the past couple of weeks. The industrial production release on May 15 revealed that manufacturing production growth dipped into negative territory year-over-year for the first time since 2016.

Early signs from May have been mixed. Last week, the New York and Philadelphia Federal Reserve banks released their regional manufacturing surveys, both showing that manufacturing growth rebounded nicely in May. It is worth noting, however, that these surveys were conducted before the latest round of tariff hikes on goods imported from China. Preliminary purchasing managers’ index data, which is collected later in the month, showed a significantly slower pace of growth in the manufacturing sector, hitting the lowest point in over nine years.

All of this suggests a weak environment for manufacturing. While some of the early-year softness in manufacturing could be chalked up to any number of temporary events such as weather, the re-escalation of trade tensions with China serves as a significant risk to that manufacturing outlook. Domestically manufactured goods serve as the origination point for much of the freight that moves through the U.S. economy, and if production begins to decline, freight volumes are likely to follow.

Behind the numbers

The headline number this morning showed a pretty severe decline, but it was largely expected given the surge in aircraft orders in March. Much of the decline in aircraft orders in April is probably tied to Boeing’s struggles after the second crash of its 737 MAX airline in March.

The details of this report were far more concerning in terms of the outlook for freight. Part of the reason why orders began to stall in the third quarter of 2018 is because of the tariffs that the U.S. and China implemented in July 2018. April results mark the last month of data before the most recent tariff increase, and there are real questions about whether concerns over trade policy will be enough to turn the trend in orders negative.

So far, trends in orders, shipments and production in the manufacturing sector have yet to experience the same sort of decline that they went though in 2015 and 2016 during the last freight recession. However, the risk of a freight recession is now very real, and the longer the trade dispute with China lasts, the larger the risk of a downturn.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now