Economic data from the goods side of the economy continued to underperform in April, as both retail sales and industrial production unexpectedly declined during the month

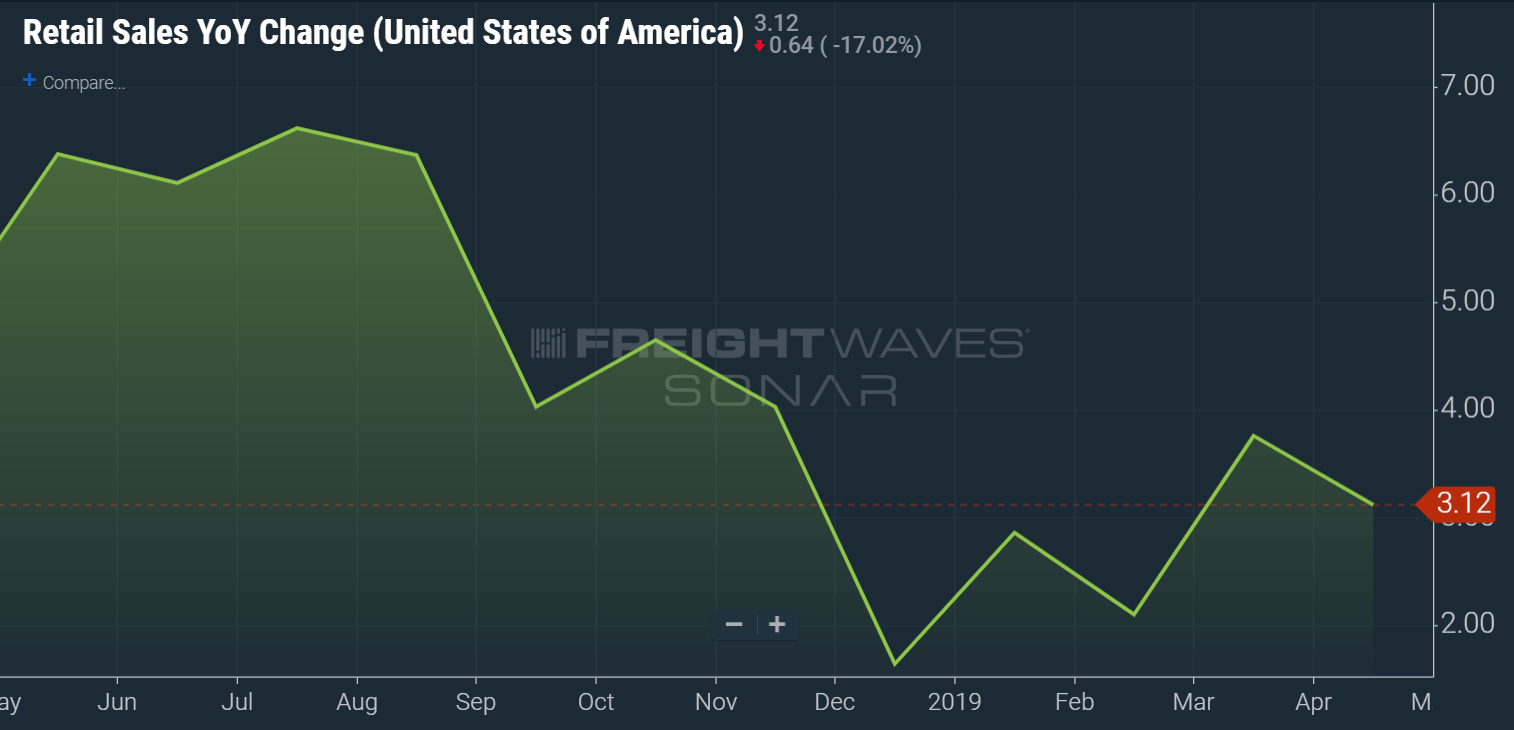

The Census Bureau reported that total retail sales fell 0.2 percent in April from March’s levels. This fell short of consensus estimates of a 0.1 percent gain, and marks the second monthly decline in the last three months . Year-over-year growth in the retail sector slipped to 3.1 percent as a result, down from 3.8 percent in March.

Retail activity struggled across a variety of industries during the month, as sales in seven of the 13 major industries in the sector either declined or were flat in April. Large drops in building materials, autos and electronics & appliances weighed overall sales during the month, though this was partially offset by a 1.8 percent increase in gasoline sales. Core retail sales, which excludes autos and gasoline from the total, also fell 0.2 in April with year-over-year growth falling to 3.2 percent.

This serves as disappointing news for trucking and parcel demand in the economy, as most of the goods movements between warehouses and retail locations occurs by either truckload, less- than-truckload, or parcel shipments. Consumer spending on goods was one of the many areas of weakness in the freight economy in early 2019, and April results suggest that activity remained subdued at the start of the second quarter.

Factory output continues to sputter

In the industrial sector, total production also unexpectedly struggled in April, falling 0.5 percent from March’s levels. This was the third drop in total factory output in the last four months, pushing year-over-year growth below 1 percent for the first time since early 2017. Manufacturing industrial production, which makes up approximately 70 to 75 percent of the total, also declined 0.5 percent in April, with yearly growth tumbling into negative territory at -0.2 percent.

As with retail, there was plenty of weakness to go around in the April manufacturing results, with more than half of the major industries in the sector reporting declining output. Durable goods industries performed particularly poorly during the month, led by 2.6 percent drops in both machinery and motor vehicle production. Nondurable manufacturing production also declined in April, but fell by a more modest 0.1 percent.

The manufacturing sector continues to be hamstrung by poor business investment demand and sluggish global growth. This also is not a good sign for freight demand as it suggests that there will be fewer goods flowing through the economy

Behind the numbers

On the retail side, the numbers were certainly disappointing, but are not necessarily a cause for immediate concern. Retail has been choppy in general thus far in 2019, with large gains in January and March followed by retreats in February and April. Abnormal weather during the early part of the year likely played a role in some of the erratic spending behavior, as did a disappointing tax return season. However, job growth remains strong in the economy and wages continue to advance at a solid pace. This combination should provide a solid foundation for retail spending going forward.

The struggles in the manufacturing sector are a significant source of concern, however. Manufacturing production has not had a positive month of growth yet in 2019 as is now below where it was at this point last year. It is hard to envision a situation where manufacturing is performing poorly but freight demand overall is growing at a solid pace, and evidence from industry metrics such as the Cass Freight Shipments index suggest that freight activity is also struggling in this environment.

Moreover, the recent re-escalation in trade tensions between the U.S. and China will likely only make matters worse. For consumers, job and income growth is healthy, but the tariff hike is certain to knock the wind out of the sails of the stock market. Consumer confidence often responds to significant swings in stock market performance, and it will be interesting to see whether this plays out in consumer spending behavior. If these tariffs remain in place for an extended period of time or are expanded to include more goods from China, it could lead to higher prices in the economy and further stunt consumer spending

For the manufacturing sector, the recent tariff hikes were a reversal in policy after most had assumed that a trade deal was imminent between the U.S. and China. Manufacturing orders essentially stalled starting in the middle of last year when the trade rift between the two nations escalated in earnest, and renewed trade tensions will only serve to make the domestic manufacturing environment tougher for most industries in the sector.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now