Europeans and Americans are getting back to work. There are more cars on the roads. Saudi Arabia and other oil producers are hitting the brakes on output. The price of crude oil has doubled. All of which might give the impression that the much-ballyhooed floating-storage tanker trade is dead in the water.

Absolutely not true, according to executives of Euronav (NYSE: EURN) and International Seaways (NYSE: INSW), the latest in a parade of tanker owners reporting blockbuster earnings this week.

“The number of vessels taken in on floating storage continues to creep up every day. It will continue to increase and support our markets,” maintained Euronav CEO Hugo de Stoop, who described how the nature of floating storage has changed while its volume has increased.

“Five or six weeks ago, traders were buying oil, chartering the ship, storing the oil on the ship and hedging themselves on paper,” he explained during the call with analysts. These were “contango” trades in which traders sought to buy oil low and sell it high.

Such deals, which were overwhelmingly six-month time charters with storage options, have waned. “The traders have balance-sheet limits. They’re not just trading oil and it’s not pretty out there,” said De Stoop.

The six-month charters that are now being signed are primarily being done by oil industry players. “The inquiries we’re receiving are from people lacking the space, who say, ‘I don’t know where to put my oil. I need to rent this ship,’” he said.

Storage deals have been inked primarily for very large crude carriers (VLCCs; tankers that hold 2 million barrels of crude oil), but also for an unusually large number of Suezmaxes (tankers that hold 1 million barrels of crude).

There is also high demand for floating storage of refined products, so much so that International Seaways CEO Lois Zabrocky said “there will be newbuilding VLCCs and Suezmaxes storing products.” When a large crude tanker leaves the yard for the first time, it can be used to store or transport products on its initial load before switching to crude.

The caveat is that the level of floating storage depends upon how you define floating storage; different research firms define it differently. In contrast to comments from Euronav executives, who cited Bloomberg data, Clarksons Research reported on Friday that according to its own numbers, floating storage had inched down to 11.4% of the tanker fleet from 11.7% the week prior.

Getting to the peak

Brian Gallagher, Euronav’s head of investor relations, pointed to “the latent amount of [floating] storage that is yet to emerge” involving ships now on their way to loading ports to pick up their storage cargoes. “Shipping doesn’t work in real time,” he noted, citing the delay between contract signing and implementation and highlighting “an ongoing disconnect between production and consumption,” which means that “the impact of floating storage has not yet been fully revealed.”

Euronav conservatively estimates that another 14 million barrels per day will go into storage this month and a further 2 million barrels per day in June. If those estimates prove true, “you could see twice as many VLCCs and twice as many Suezmaxes being taken before the end of June, which would have a positive impact for the ships that are still trading because there’s still a lot of demand for transporting oil and the spot market should reflect the diminishing supply of the world fleet,” said De Stoop.

“We think floating storage could peak sometime in June, but remember, those [charter] contracts are for six months,” he continued. As Gallagher put it, “If this finishes in the middle of June, it’s not like all the [stored] barrels will be redistributed in the third week of June. Shipping doesn’t work that way.”

After the peak

According to Zabrocky, “All of the different refineries around the world and every producing country is trying to calibrate with demand. When refineries are running too high, you see excess refined products [going into storage]. When refineries are running too low and production is still high, you see storage on the crude side.”

De Stoop explained that the eventual unwinding of storage will begin with the consumer of refined products. “When there is a recovery in consumer demand, let’s not forget that there are quite a lot of products stored,” he added.

When the gasoline, diesel and jet fuel stored on land and at sea is drawn down, refinery demand for crude inputs would increase. “And when they need more crude oil, they will first process what they have in storage … and we believe the first oil will be grabbed from land storage near the [refining] facilities … before they touch what is onboard vessels,” he said.

When there finally is demand to unload crude from floating storage, there are two scenarios: the quick drawdown and the slow drawdown. “Many commentators believe the inventory drawdown will be rapid and therefore the impact on shipping will come much quicker, but we find this difficult to envisage,” said Gallagher.

“What is likely to happen is a slow draw,” argued De Stoop, noting that “the last time we had a contango [in 2015-16], it took 12 months for the ships taken on storage to come fully back into the trading fleet.

“There’s a reason for that. If tomorrow all the oil that had been stored somehow came back to the market, obviously the oil price would be negatively impacted by the draw on the inventory. That means a contango would be created, because when you draw down the oil, the price will be higher [in the forward contract], creating the contango curve, and when you create the contango curve, you’re obviously asking more ships to play that game and to store the oil for that contango story.”

Even if floating storage peaks next month, Euronav executives don’t foresee a full unwind until later this year at the earliest. Zabrocky said it could be “maybe in 2021.” And assuming the pace of the storage unwind is slow, “it will not be a catastrophe,” maintained De Stoop.

More concerns on false expectations

Beyond floating storage, another important topic on the Euronav call involved artificially inflated investor expectations. It marked the third day in a row that tanker executives had publicly commented on the gap between actual rates and the rates implied by indexes and shipbroker reports.

When a spot “fixture” deal is first reported, it is “on subjects,” which means the charterer has a period of time to vet the ship before “lifting subjects” and closing the deal, after which it is “fully fixed.” Sometimes, particularly in frothy markets, the charterer does not lift subjects and the fixture fails.

According to De Stoop, “One of the reasons why the indexes are probably ahead of the physical market when it comes to time-charter equivalent [TCE rates] is because there has clearly been an abuse of subjects, certainly in the last three months.

“When you fix a vessel, subjects are a concept invented to make sure the vessel is technically acceptable to perform a contract. It is certainly not to be treated as an option, to keep the vessel for two or three days and if you see the market go up, you take the ship, and if you see the market go down, you let it go. That’s a clear abuse.

“Subjects are there because the vessel cannot be inspected physically or the vetting reports cannot be done at the time the rate was negotiated, or the terminal needs to accept the vessel. You need to check a number of things. But there’s absolutely no reason why the fixture should fail if all your papers are in order and you had agreed to a rate. Unfortunately, that’s not what’s happening. It [the practice] is something that has increased … as the market has become more volatile.”

This is not just a problem for shipowners, he warned. “The indexes are much more geared towards the ships on subs than the ships that are fully fixed. So, what you see is the ships on subs, and there have been a lot of fixture failures, more than usual, simply because there is a lot of volatility. That creates a distortion, because it has created false expectations that rates are even higher than they are.

“There’s very little we at Euronav can do to address it,” said De Stoop. “This is something that we as an industry should address.”

Record quarterly results

This week’s announcements on record quarters for U.S.-listed tanker companies are beginning to sound like a broken record. The strong results posted by Euronav and International Seaways on Thursday were no exception.

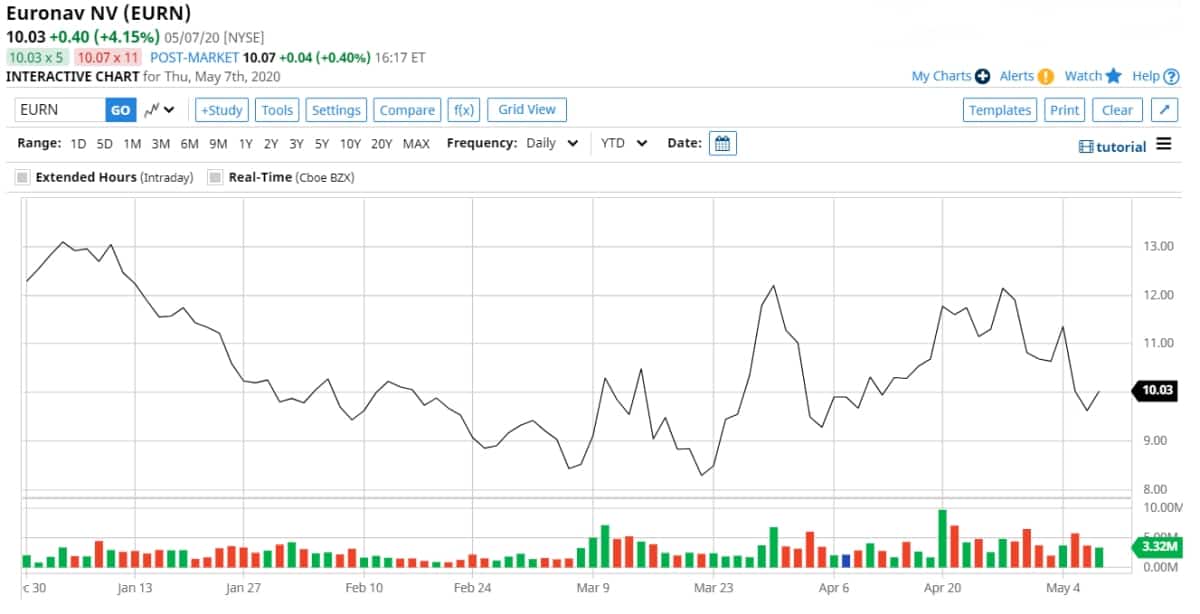

Euronav, which owns crude tankers, reported net income of $225.6 million for the first quarter of 2020, more than 10 times net income of $19.5 million in the first quarter of 2019. Adjusted earnings of $1.01 per share handily topped the consensus forecast of 77 cents a share.

The company’s spot-trading VLCCs earned $72,750 per day in the first quarter and its spot Suezmaxes $59,240 per day. So far in the second quarter, its VLCCs are earning $95,000 per day and its Suezmaxes $65,000 per day.

Euronav’s stock rose 4% on Thursday but is still down 22% year to date. Joking about the relative lack of stock appreciation given its earnings, Stifel analyst Ben Nolan wrote, “If a tree falls in the forest … Euronav is making a fortune.”

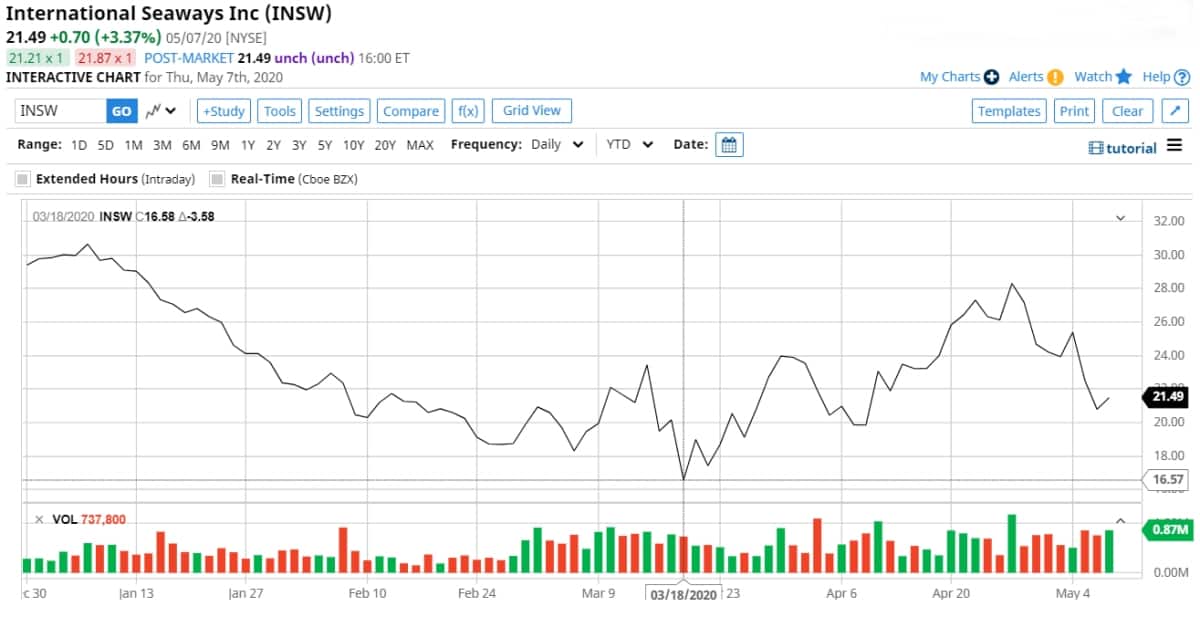

International Seaways, which owns both crude and product tankers, reported net income of $33 million for the first quarter of 2020 compared to $10.9 million in the same period last year. Adjusted earnings of $1.49 per share, while the highest in the company’s history as a public entity, came in below the consensus forecast for $1.64 per share.

International Seaways’ spot VLCCs earned $63,800 per day in the first quarter, and its Suezmaxes $42,800 per day. It has fixed 71% of its available second-quarter VLCC spot days at $87,900 per day and 58% of its available second-quarter Suezmax spot days at $63,100 per day.

The company’s shares closed up 3% on Tuesday but are still down 28% year to date. More FreightWaves/American Shipper articles by Greg Miller

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now