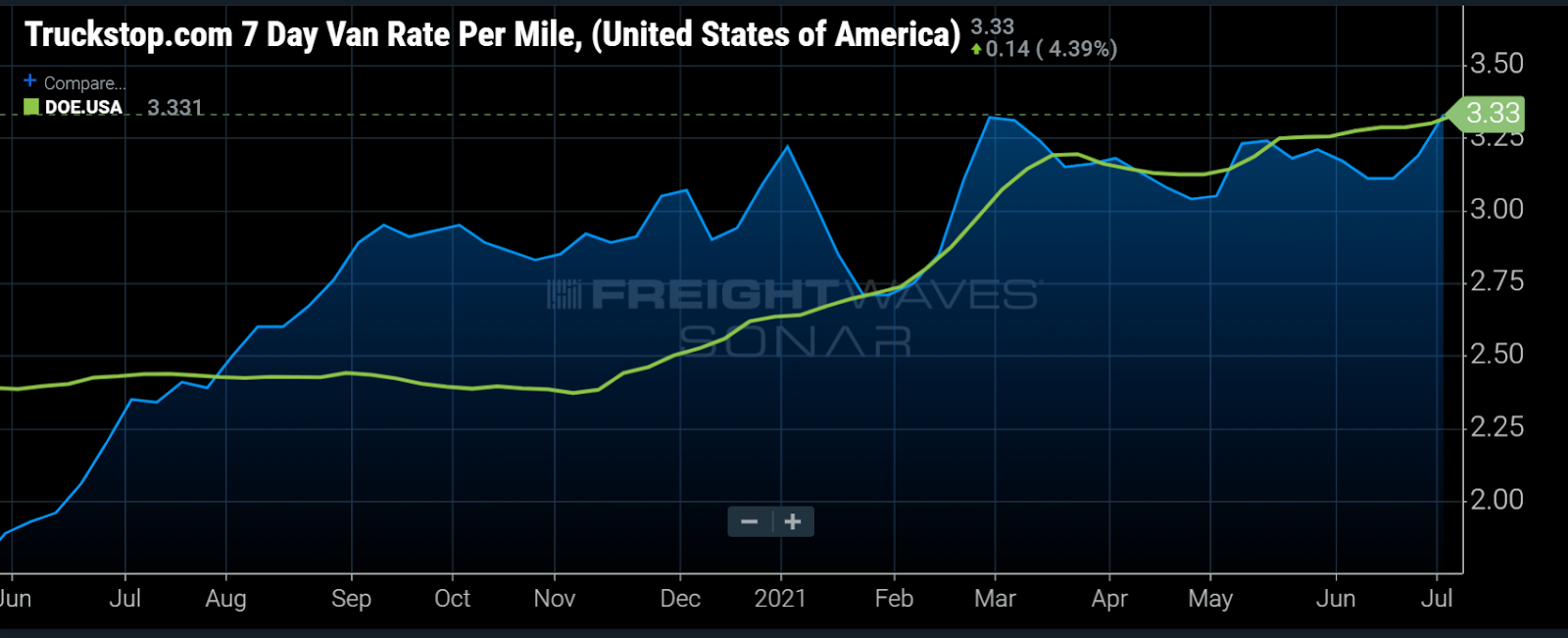

Chart of the Week: Truckstop.com 7-day Van Rate per Mile, Department of Energy average retail price of diesel – USA SONAR: TSTOPVRPM.USA, DOE.USA

Truckload spot rates continue to trend higher in 2021, averaging $3.18/mile over the past two months compared to $2.96/mile (7.4%) from November to December of last year, according to Truckstop.com’s average top 100 lanes. What can get lost in the cost of transportation is the rising underlying costs such as maintenance, insurance and the most easily tracked — fuel.

Since Nov. 1, the average retail price of diesel fuel as reported by the DOE has risen nearly 40%, which has made the freight market appear to be tightening faster than it is.

Over the past decade, spot rates have been used for measuring and understanding truckload capacity and supply and demand conditions in truckload transportation. One of the many problems with this is the fact rates are a sum of multiple variables, many of which have nothing to do with the balance of supply and demand in the market. Most of these factors like the ones mentioned above are invisible, but fuel is not.

Many loads that move on the spot market do not show fuel surcharges as a portion of the cost, unlike most of the contracted loads. Contracted rate agreements typically have fuel surcharge tables appended to the agreement to account for the wild fluctuations in fuel prices so that rates do not have to be adjusted constantly. See the above chart where fuel prices have increased 40% over the past eight months.

Fuel costs account for 5-15% of the cost of transportation on average and carriers have to make this a variable cost to ensure they are not overly exposed to this fluctuation. They may not overtly show it in some of the spot rates, but it is most definitely there. So how much has fuel moved the perceived market over the past six months?

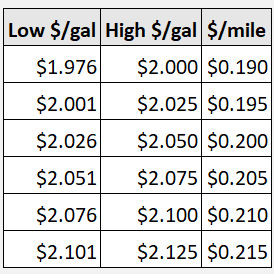

Using a relatively standard carrier fuel surcharge table that assigns a cost per mile based on the DOE national average we can estimate its impact on spot rates over the past several months. The fuel table used in this exercise moves the rate per mile 0.5 cents for every 0.025 cent increase in fuel.

Backing out estimated fuel surcharges from November to December yields an average rate of $2.67/mile, while the past two months show a $2.74/mile average or a 2.6% increase.

While this is not a perfect way to measure the changing conditions of the market, fuel has played a big role in moving rates higher and faster and should not be ignored.

Looking at tender data — which largely measures contracted freight and roughly 80% of the for-hire freight market — rejection rates in November and December averaged 26.2% versus 24% in May and June. Tender volumes have averaged 10% higher in the spring versus last fall. FreightWaves contract invoice data for van truckloads has risen 12% since November — slightly more compliance at a much higher rate.

All signs point to demand simply being more than current capacity can handle and increasing input costs will likely help sustain transportation spot rates throughout the year as contract rates slowly come into alignment with them.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new data sets each week and enhancing the client experience.

To request a SONAR demo, click here.

Freight Fraud Symposium

Double brokering. AI deepfakes. Identity theft. Freight fraud is an existential threat to the industry. Get ahead of it.

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

Future of Rail Symposium

Reshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

Double brokering. AI deepfakes. Identity theft. Freight fraud is an existential threat to the industry. Get ahead of it.

Rock & Roll Hall of Fame • Cleveland, OH Register NowPast the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post Office • Chicago, IL Register NowReshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now