Crude-tanker spot rates remain in “Twilight Zone” territory, hovering near a modern-day record as if the rules of gravity no longer apply.

“Last done” rates for very large crude carriers (VLCCs, tankers that can carry 2 million barrels of crude oil) were still in the vicinity of $300,000 per day on Oct. 14, more than 10 times the ships’ breakeven rate, creating a massive spike in cash flow for owners. Rates pulled back toward $200,000 per day on Oct. 15.

The transport cost for crude oil has shot up to around 12% of the value of the cargo versus around 3% normally, but ocean shipping rates are extremely elastic, have no regulated upper limit. To put current VLCC freight costs into perspective, when dry bulk rates reached their epic peak in the 2004-2008 shipping boom, they equated to 50% of cargo value – and those cargoes still moved.

Shipping analysts are breaking out their thesauruses to find new synonyms and exclamatory phrases to describe the tanker space. Stifel’s Ben Nolan: “Bonkers.” Clarkson’s Platou Securities’ Frode Morkedal: “Fantasy earnings coming true.” Deutsche Bank’s Amit Mehrotra: “Blockbuster cash windfall.” Evercore ISI’s Jon Chappell: “Unprecedented … unbelievable … beyond your wildest dreams … a blowtorch to a mountain of oily rags.”

Amidst all this frothy talk, however, it’s worth remembering that today’s VLCC spot rates are much higher than what public companies will report as their average time-charter-equivalent (TCE) rates for the fourth quarter and that earnings will be affected by fuel cost.

Caveat 1: Limits to spot-rate exposure

The first caveat is that the global VLCC fleet, numbering almost 800 vessels, is not on permanent index-linked time-charter contracts. Owner income does not move up and down every day in lockstep with spot rates. Far from it.

A portion of the fleet is on long-term time charter (with or without profit-sharing clauses) and will therefore miss out on some or all of the rate spike. Furthermore, the majority of VLCCs not tied up on time charters are not actually available to bid on today’s highly lucrative spot employment contracts. Most of them are currently sailing on the fronthaul or the backhaul of spot contracts that were signed before rates skyrocketed.

It can take 50 days to sail from the Middle East to Asia and back. It can take a month and a half – each way – to sail between the U.S. Gulf and Asia (via the Cape of Good Hope). The only VLCCs that can bid on cargo auctions in loading ports in the Middle East, U.S. Gulf and West Africa are those that happen to be empty and close enough to make a bid.

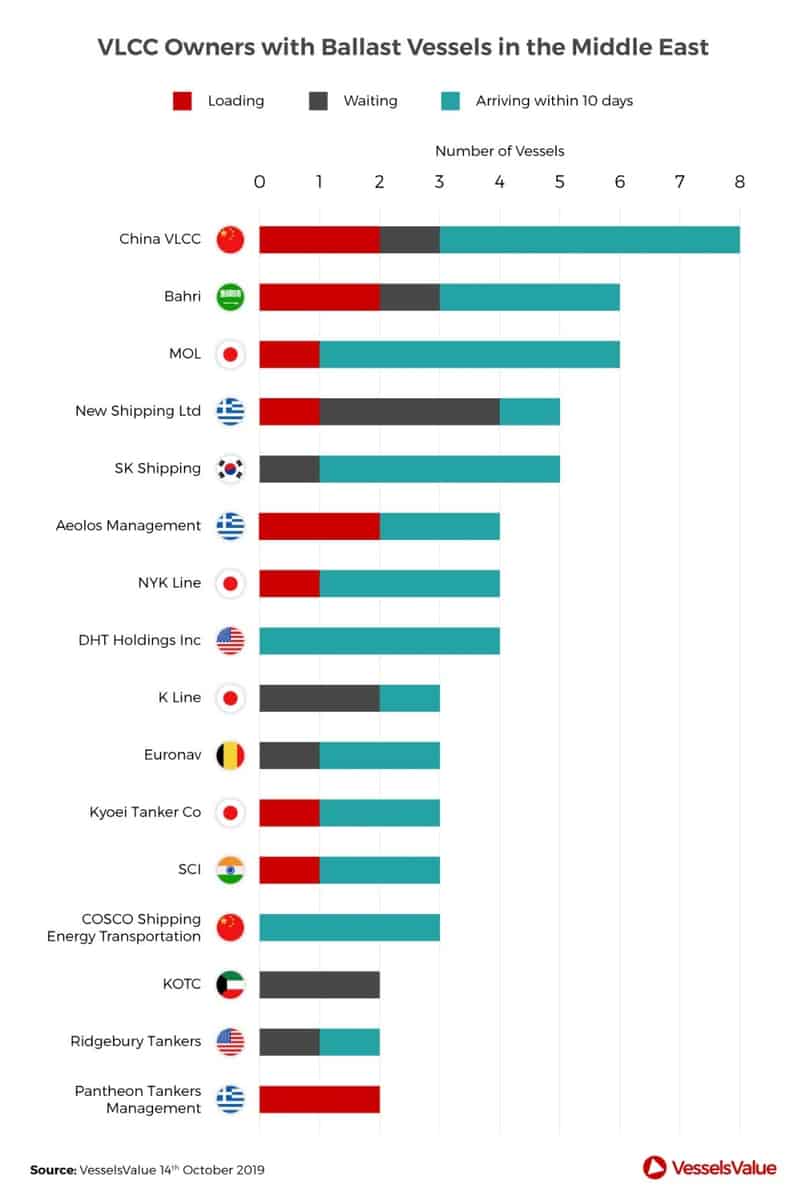

U.K.-based VesselsValue has used vessel-positioning and ownership data to map out exactly which owners have exposure to today’s near-record-level VLCC rates out of the Middle East.

Excluding ships that are already loading, it counts 50 VLCCs either waiting for cargoes in the Middle East or arriving within 10 days, led by China VLCC (one waiting, five arriving), Japan’s MOL (five arriving) and South Korea’s SK Shipping (one waiting, four arriving). Of the U.S.-listed companies, only two are on VesselsValue’s list: DHT (NYSE: DHT), with four arriving, and Euronav (NYSE: EURN), with one waiting, two arriving.

Caveat 2: Scrubber installations

Many VLCCs are not in position to load cargoes at current spot rates due to IMO 2020, the regulation that requires all vessels not equipped with exhaust-gas scrubbers to burn more expensive 0.5% sulfur fuel starting Jan. 1.

Scrubber installations are particularly popular among owners of larger vessel classes sailing longer voyages, including VLCCs. They are generally done at Asian shipyards and take ships off-hire for about a month per installation. Clarksons Platou Securities previously estimated that there would be 55 VLCC installations between October and January.

According to Morkedal at Clarksons Platou Securities, the current rate surge is prompting some owners to seek delays in scrubber installations. “Based on conversations with industry players, owners are likely to try to walk away from scrubber retrofits or try to move time slots given the strong earnings. Owners are hoping stretched shipyards could be flexible,” he said on Oct. 14, citing the possibility that installations could be pushed back to the second quarter of 2020.

But even if some of that happens, it’s logical to assume it’s already too late for many owners. For those planning installations to meet the IMO 2020 deadline, many ships would likely be already en route to Asia with a cargo for discharge prior to the yard visit. Other VLCCs would already be in the yards in the process of getting scrubbers installed, while others would have had work recently completed and would still be in the Pacific Basin, too far away from loading ports to take advantage of current rates.

Meanwhile, VLCC scrubber installations are frequently cited by analysts as a tailwind for rates, given that this work removes capacity; to the extent those contracts are delayed, it would be less of a tailwind.

Caveat 3: Quarterly timing and rate-spike duration

The timing of the rate spike in relation to quarterly reporting periods is yet another important factor. In July-September, VLCC rates ranged from $15,000-$40,000 per day. Extreme rates have only been seen this month and will not affect third-quarter results.

A significant portion of public VLCC owners’ available “capacity days” are booked before a quarter has even begun. Given the very long sailing duration of a typical VLCC voyage, earnings are often tied to contracts signed in the prior quarter. For example, on Aug. 6, when DHT reported its second-quarter earnings, it said that it had already booked 65% of its available VLCC spot days for the third quarter at an average rate of $21,100 per day.

This “lag effect” was just exemplified in the dry bulk shipping market in the Capesize market (Capesizes are bulkers with capacity of 100,000 deadweight tons or more). Capes enjoyed a major rate run-up during the second quarter because there were not enough vessels available in the Atlantic Basin to serve Brazilian iron-ore exports to China. But reported second-quarter average TCE rates for public Capesize owners didn’t move in synch; TCE rate averages were dragged down by extremely low spot rates in the first quarter.

Fourth-quarter results of public VLCC owners will inevitably face the same lag effect. To what extent depends on how long the current VLCC bonanza lasts and how much capacity was already booked at lower rates before the quarter began.

How long rates will stay this lofty will hinge on how lasting the geopolitical drivers – the COSCO sanctions, the Saudi oil facility attacks, the Iran tanker attack – turn out to be. It will also depend on how quickly VLCC owners can reposition their ships to loading ports and compete for cargoes. In the Capesize segment, once owners brought more ships back into the Atlantic, which took about 45 days, rates sank back to normal.

Caveat 4: Higher fuel costs

The reported TCE rate that’s stealing all the headlines is not the contractual rate and it’s not the equivalent of earnings. In a spot deal, the shipper pays in dollars per ton of cargo and the ship owner or operator covers the cost of fuel, port and other voyages expenses.

To calculate the time-charter-equivalent rate, which is measured in dollars per day, assumptions are made on vessel speed and fuel consumption; voyage costs are added into the equation and that total is divided by the assumed voyage duration measured in days. The cost of fuel – and the type of fuel that’s burned – is very important to the TCE rate calculation and to earnings.

Morkedal estimated that of the $308,000 per day VLCC spot rate assessment as of Friday, Oct. 11, around $8,000 was fuel and other voyage costs, equating to $15 million in EBITDA from such a voyage, assuming 50 days there and back.

But what if fuel costs were much higher? There are several reasons to believe this could happen.

First, fuel consumption rises exponentially with speed. Given the spot rates on offer at loading ports, it’s reasonable to assume that owners on the backhaul run after dropping off spot cargos could speed up considerably to position themselves for future spot upside.

Second, for vessels to comply with IMO 2020, they cannot just switch to buying more expensive compliant fuel on Jan. 1. They must burn all their noncompliant 3.5% sulfur fuel first, clean the tanks, then load 0.5% sulfur fuel. For ships with longer voyage lengths, like VLCCs, owners are believed to be switching to compliant fuel this month. Thus, if VLCCs in Asia are “stepping on the gas” to get back to the Middle East, they may already be burning more expensive 0.5% fuel.

Third, if analysts like Morkedal are correct and VLCC owners are indeed pushing back scrubber installations until the second quarter of 2020, that means they will be spending at least one more quarter than previously planned consuming much more expensive low-sulfur fuel.

If spot rates stay where they are today for an extended period, that extra IMO 2020 fuel cost will be a drop in the bucket and all of the other caveats will fade. But in ocean shipping, rates driven up rapidly by unexpected geopolitical events have a habit of falling back, sometimes just as quickly. More FreightWaves/American Shipper articles by Greg Miller

Freight Fraud Symposium

Double brokering. AI deepfakes. Identity theft. Freight fraud is an existential threat to the industry. Get ahead of it.

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

Future of Rail Symposium

Reshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

Double brokering. AI deepfakes. Identity theft. Freight fraud is an existential threat to the industry. Get ahead of it.

Rock & Roll Hall of Fame • Cleveland, OH Register NowPast the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post Office • Chicago, IL Register NowReshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now