Earlier this week, in the last edition of The Stockout CPG-focused newsletter, I focused on reefer since the many CPG companies that require temperature controls are facing an even tighter freight market than those that do not. Today, I am shifting gears to discuss shipping dry goods and, specifically, intermodal insights from the latest datasets added to SONAR. Many consumer products are major intermodal customers and consumer products companies represented 31% of Hub Group’s revenue in 2020. An example of an CPG company utilizing domestic intermodal is General Mills moving boxes of cereal; that’s ideal for intermodal because it is often consumed a long distance from where it is produced, is less time sensitive and does not need to be refrigerated. For CPG companies, intermodal can serve the dual purpose of saving freight costs and lowering their supply chains’ carbon footprint.

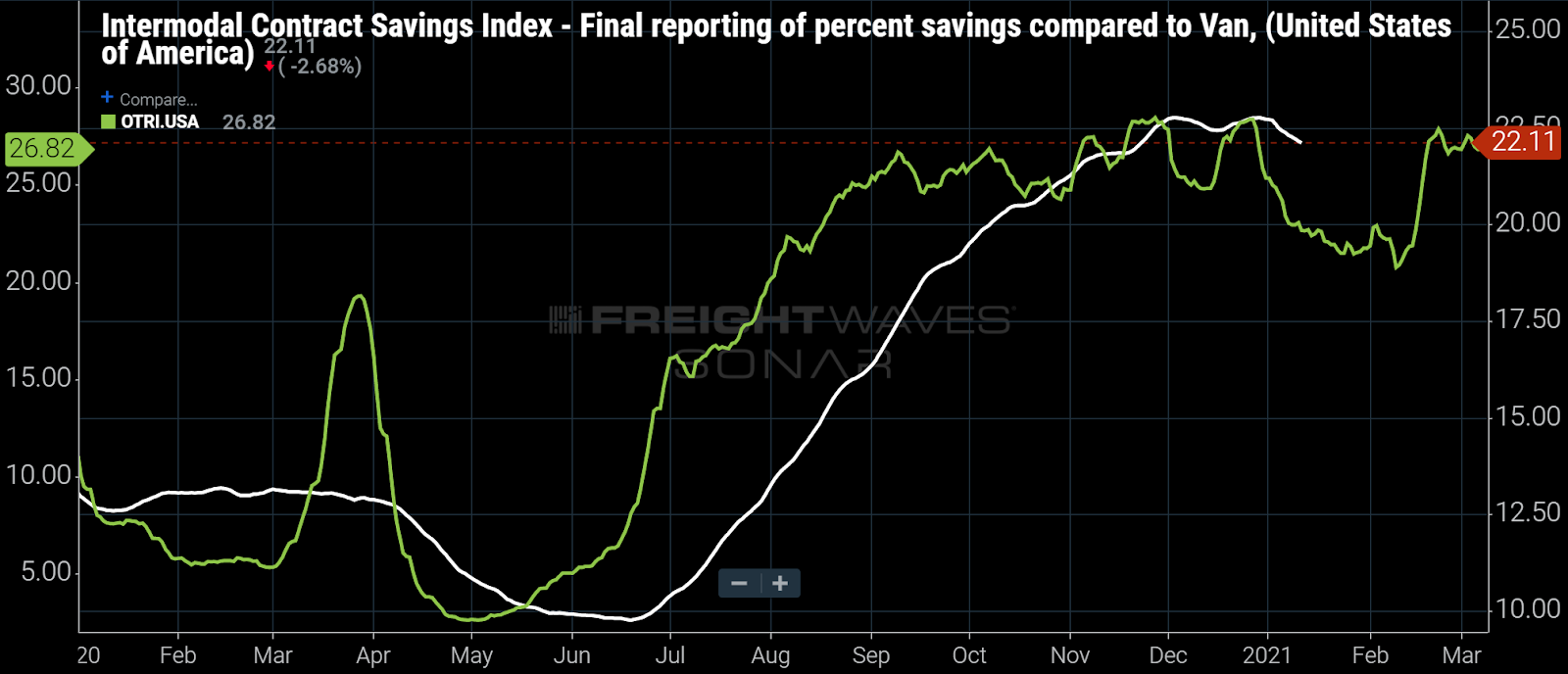

Intermodal shippers save more versus truckload when truckload markets are tight.

(Chart: FreightWaves SONAR. The white line shows the Intermodal Contract Savings Index, or the percent difference between truckload and intermodal contract rates, including fuel surcharges, on identical lanes. The green line shows the SONAR nationwide outbound tender rejection index).

Intermodal provides shippers with greater savings versus truckload in tight freight markets.

The chart above plots the latest data series added to SONAR (the Intermodal Contract Savings Index) against one of our marquee data series (the Outbound Tender Rejection Index). Those indices measure different things and come to us from very different data sources, but clearly move together. And the tender rejection rate appears to lead the Intermodal Contract Savings Index.

I believe the main reason why those data series move together is that truckload contract rates are more volatile than intermodal contract rates. So, when domestic freight markets are tight, such as when carriers are rejecting 27% of tendered loads, as they are now, truckload contract rates rise more than intermodal contract rates, and the typical 10%-15% savings normally associated with utilizing intermodal can expand above that range — the chart above shows a 22% savings. Conversely, when freight markets are loose, truckload contracts typically fall further than the relatively stable intermodal contract rates — in those cases, shippers’ savings associated with intermodal may fall below the historical 10%-15% range, as they did briefly in the middle of last year.

The tender rejection rates contained in SONAR provide a leading indicator for truckload spot rates, which rise and fall as a result of the degree of carrier compliance with existing contracts. In turn, truckload spot rates are a leading indicator for changes in contract rates, which are typically priced on an annual basis throughout the year. Therefore, when freight market conditions tighten or loosen, it should perhaps be time for consumer products companies to reevaluate which goods should move via rail intermodal because the economics may be changing.

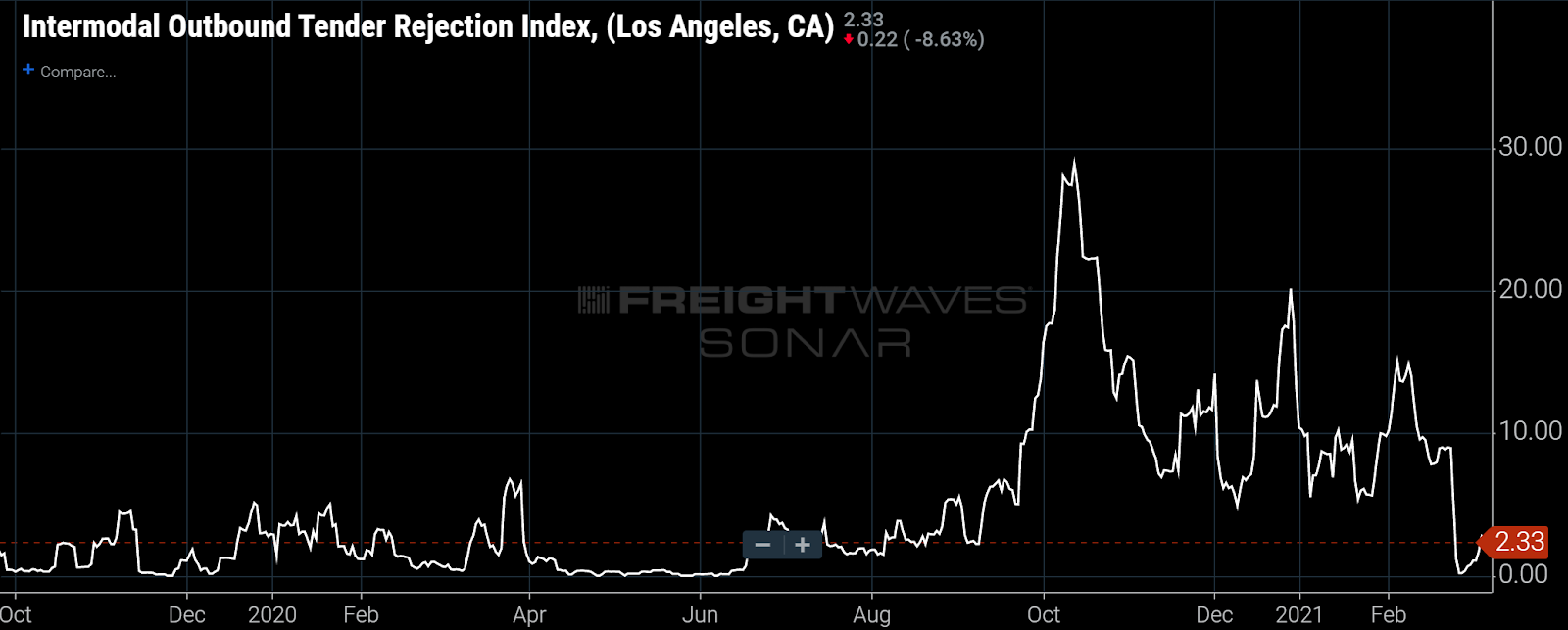

Intermodal tender rejections are typically fairly rare, but they cropped up in greater numbers starting last fall amid congestion on the West Coast.

(Chart: FreightWaves SONAR. The white line shows the tender rejection percentage on intermodal loads outbound from Los Angeles).

In addition to the greater volatility associated with truckload contract rates, as compared to intermodal contract rates, I’ll throw out one other reason why intermodal contracts savings and tender rejections tend to move together: Tight freight markets are often associated with congestion and service issues that can exacerbate the service disadvantage that intermodal has relative to truckload. In other words, shippers that are comparing costs between intermodal and truckload will require a greater savings to move goods via intermodal when they are more concerned about service levels and that is reflected in the rates.

The chart above shows one of the datasets that I use to gauge intermodal network fluidity. Unlike truckload, in which tender rejections are more common, typical intermodal tender rejection rates for intermodal loads are in the low-single digits. Rising intermodal tender rejection rates starting last summer on the West Coast was a sign of network disruption that has persisted ever since.

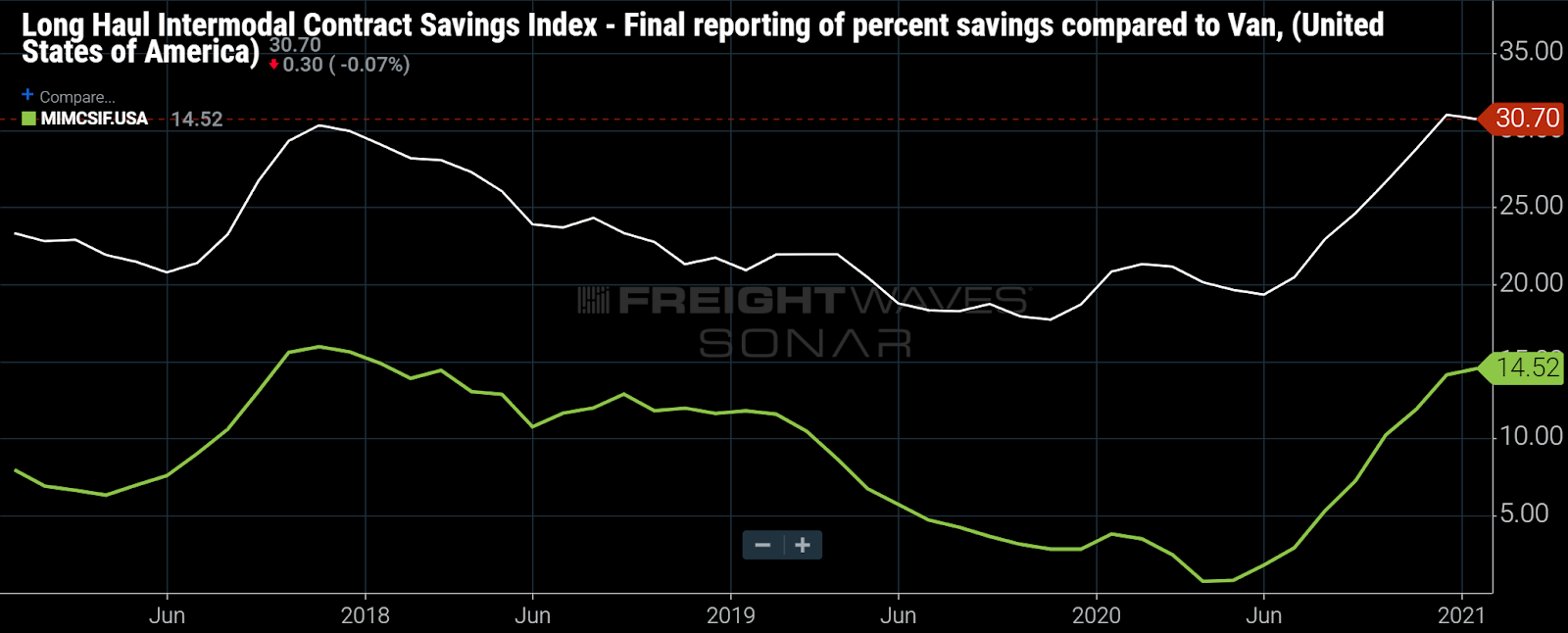

Intermodal provides greater savings to shippers when used over longer lengths of haul.

(Chart: FreightWaves SONAR. The white line shows the intermodal savings percentage, relative to truckload, on lengths of haul greater than 1,200 miles and the green line shows the intermodal savings percentage on hauls between 800 and 1,200 miles.).

In addition to cost savings, intermodal provides an environmental benefit.

Intermodal has always been far more fuel efficient than truckload, and that is a major component of the intermodal cost savings: In addition to being 10%-15% less expensive, the intermodal fuel surcharge is typically about half of the truckload fuel surcharge.

What’s changed is companies’ intense focus on environmental, social and governance (ESG) criteria as investor relations presentations now have almost as much ESG information as that on the companies’ operations and financials. CPG companies are particularly concerned about this since so many consumers are now voting for companies perceived to be environmentally friendly with their wallets. One interesting take on both the relative costs of truckload and intermodal came from J.B. Hunt’s VP of investor relations, who recently speculated that intermodal may be given more room for pricing growth if shippers that move goods via truckload are required to buy costly carbon tax credits.

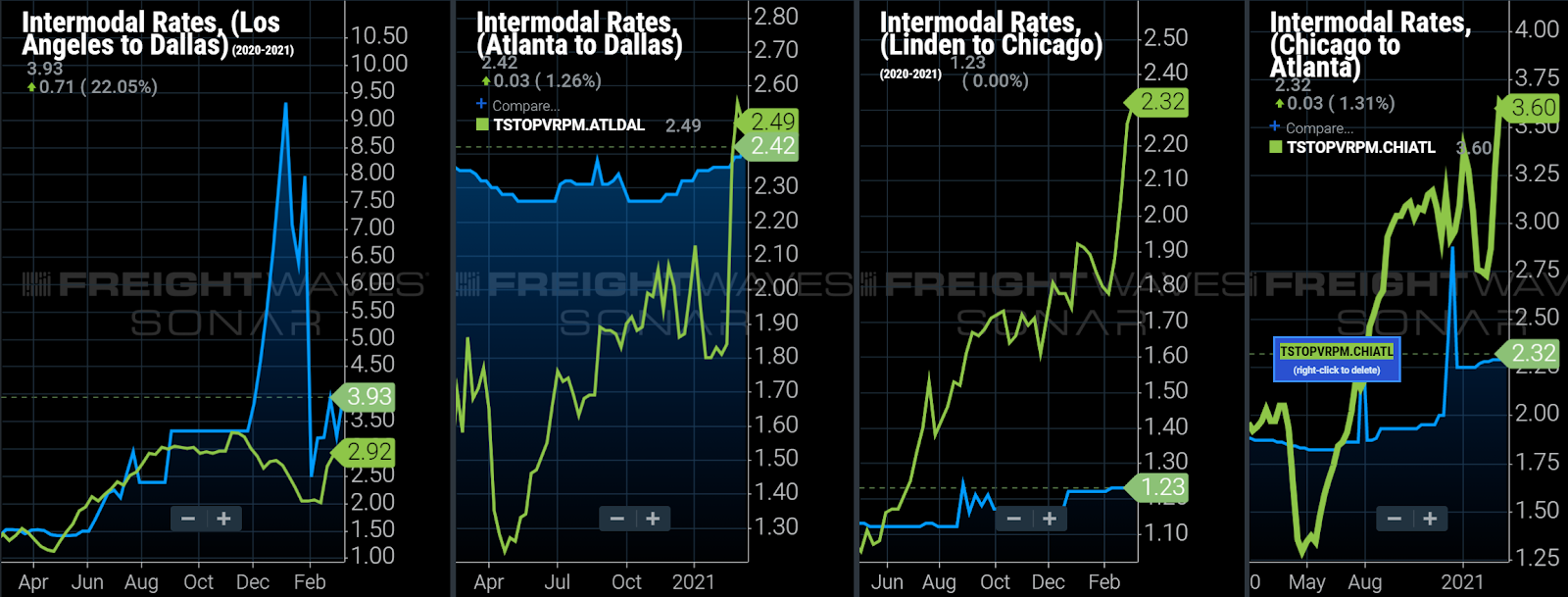

Two lanes where truckload makes sense and two where intermodal make sense.

(Chart: FreightWaves SONAR. For the four above lanes, the green lines show truckload spot rates from Truckstop.com and the blue lines show domestic intermodal spot rates to move 53-foot containers. Both datasets include fuel surcharges.)

Amid severe lane imbalances, the relative economics of rail intermodal is mixed by lane.

In the charts above, truckload spot rates are in green and intermodal spot rates are in blue. The charts show that the relative rates vary widely by lane and are in constant flux. Most intermodal volume moves under contract rather than spot (which is part of why we rolled out the Intermodal Contract Savings Index shown in the first chart, which is based on contract rates), but these comparisons give shippers a daily indication of relative capacity in major intermodal lanes. SONAR spot rate data show: 1) It is not currently economically viable for shippers to move spot loads from LA to Dallas; 2) Atlanta to Dallas is roughly at parity (which is, of course, not worth the service hit associated with intermodal); and 3) shippers are able to realize significant savings from Linden, New Jersey, to Chicago and from Chicago to Atlanta.

Is that data consistent with your experience in the field? Is using rail intermodal in your ESG plans? Let me know at mbaudendistel@www.freightwaves.com.

For information on SONAR or to request a demo, please click here.

If you would like to receive this newsletter, please join us here: https://web.www.freightwaves.com/thestockout

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post • Chicago, IL Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now