Truckload carrier Heartland Express reported only a slight increase in operating income for the fourth quarter despite making acquisitions that doubled the size of the company.

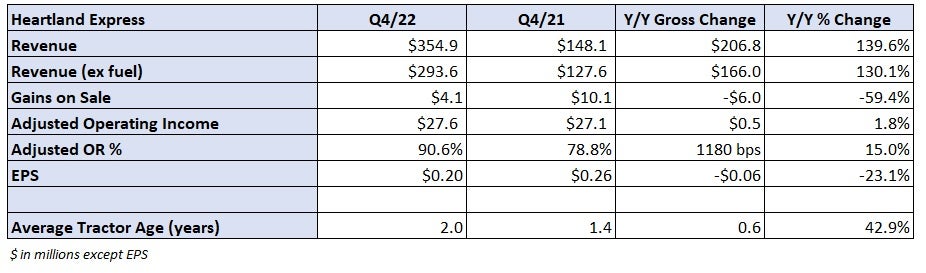

Compared to the year-ago quarter Heartland’s (NASDAQ: HTLD) consolidated revenue increased 140% with adjusted operating income moving just 2% higher. The company missed earnings expectations on Friday, reporting earnings per share of 20 cents compared to the consensus estimate of 29 cents. The number was 6 cents lower year over year (y/y).

Gains on sale were down by $6 million y/y, which resulted in a 6 cent headwind, and a noncash amortization expense resulted in a 1 cent drag to results.

“While we are excited by the recent and significant growth in our organization, we are also mindful that in the periods immediately following acquisitions we face additional operating headwinds,” CEO Mike Gerdin stated in a news release.

He pointed to headwinds tied to “the revaluation of [acquired] equipment,” which pushed depreciation expense higher on an absolute basis (down 320 basis points as a percentage of revenue). Also, a lack of immediate cost synergies and honoring the contracts of the acquired fleets were cited as placing a temporary drag on fixed costs.

The fourth-quarter result included a full-quarter contribution from Contract Freighters Inc. (CFI), which was acquired in late August. That company was generating $575 million in annual revenue at the time. Results from Smith Transport, a $200 million fleet acquired by Heartland in May, also boosted y/y revenue growth.

Heartland reported a consolidated adjusted operating ratio of 90.6% in the period, 1,180 bps worse y/y. The company’s previous operations ran at a much better level than CFI and Smith, which have operated at 98.1% and 93.5%, respectively, on Heartland’s watch.

“Given the scale of the two most recent acquisitions relative to the consolidated company, this had a meaningful negative impact on our legacy operating results during the fourth quarter of 2022, the first full quarter of CFI operating results, and we expect that to continue in early 2023,” Gerdin continued.

The company does not provide operating metrics for utilization and pricing in its quarterly reports.

“Throughout 2022, freight demand moved from a position of strength early in the year and then declined significantly as the year progressed to much lower levels of freight demand than was experienced in the prior year,” Gerdin said.

Debt and finance leases totaled $413 million at the end of the year. The company’s cash balance declined $108 million to $50 million. The changes were the result of financing the acquisitions. Heartland reduced debt by $75 million between September and December. It plans to return to a debt-free balance sheet in the future.

Shares of HTLD were down 4.1% at 1:36 p.m. Friday compared to the S&P 500, which was off 0.9%.

More FreightWaves articles by Todd Maiden

- ArcBest’s Q4 light of analysts’ expectations

- Schneider’s 2023 outlook better than expected

- Landstar navigates downturn in Q4, points to summer recovery

Which markets are changing?

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now