It has been a year since I wrote “Why I believe a freight recession is imminent.” The article, published on March 31, 2022, stated my case for why I thought the U.S. trucking market was headed for a significant downturn.

The information in the article was based on analysis from SONAR, FreightWaves’ high-frequency freight data and price reporting platform. SONAR is the market’s leading freight market analytics and price reporting system.

At first, there was a great deal of vitriol aimed at the FreightWaves analysis and also disagreement about the health of the freight market. This was most pronounced coming from asset-based truckload carriers that predominantly operate in the contract market. The downturn, they believed, was a spot market phenomenon that wouldn’t impact them.

Others contested the SONAR data and the FreightWaves staff analysis because they were using lagging indicators and government data. These tools have consistently proved to have little value and do not provide actionable insights that participants can use to manage their business — as SONAR does. Sure, they may provide some level of insight about what happened six months ago, but in the freight business, that might as well be a lifetime ago.

The freight market is one of the most volatile markets on the planet. Hot markets can turn ice cold in a flash, particularly after the federal government and central bankers flooded our economy with so much liquidity and then proceeded to institute the fastest monetary tightening cycle in history.

Hindsight is 20/20, and now the debate over the freight market downturn is a thing of the past. The freight recession has come, and carriers, regardless of whether they operate in the contract or spot markets, are having to contend with it.

Executives of both carriers and brokers who we’ve spoken with have said the current freight market is among the most challenging of their careers and this is supported by the same SONAR data that was among the first to signal a sharp downturn.

The last freight recession took place in 2019. It was called a “trucking bloodbath,” as excess capacity flooded into the market in the wake of the ELD mandate. Carriers operating on the edge couldn’t survive, particularly those operating strictly in the spot market. At one point, FreightWaves covered 10-plus bankruptcies per week.

Freight market conditions are a function of the balance of supply and demand and the build-up of excess capacity is the most probable cause of the trucking boom-and-bust cycle.

As we enter the second quarter of 2023, it appears that the freight market may be worse than the freight recession of 2019, as tender rejections are on the verge of dropping below 3% (now 3.05%). The low in 2019 was 3.86%.

A second trucking bloodbath?

A second “trucking bloodbath” — something that we predicted in March 2022 — was slow to come. Truckload carriers had built strong balance sheets during the COVID super-cycle in freight; most were able to withstand 2022’s most challenging conditions.

In March 2023, however, that changed. FreightWaves started to receive alerts from sources about a number of overnight shutdowns or carrier wind-downs that only happen when conditions are suddenly bleak.

FreightWorks Transportation, a North Carolina truckload carrier with 200 trucks, announced it was shutting down on March 6. An executive from the carrier suggested that a large, long-term shipper suddenly pulled freight from the company and gave it to another carrier. This set off a series of cascading events that forced it to wind down its operations.

On March 22, FreightWaves reported that Flagship Transport, a Miami-based carrier with 455 trucks under contract, suddenly stopped paying its bills, abruptly shuttered and stopped answering calls from drivers. This sudden shutdown is sadly all too common in the trucking industry.

On March 24, FreightWaves reported that another Miami-based trucking company, Soler & Soler Hauling with 42 drivers, filed for bankruptcy. The company had a CDL training school but was also plagued with a number of safety violations.

Often, carriers living on the edge are the most vulnerable in market climates like the one that our industry is facing. A sharp downturn does clean up some of the carriers with questionable operations, which are usually obvious when their safety records are reviewed.

What about contract rates?

With tender rejections so low, spot rates are unlikely to trend up. What does this mean for trucking contract rates?

Because trucking capacity between contract and spot is fungible, the spread tells us what we need to know about the direction of contract rates.

Contract rates and spot rates should trade within a tight range. Spot rates “pull on contract rates.”

If spot rates are much higher than contract rates for a few months, they will “pull up” contract rates. If spot rates are much lower than contract rates for a period of time, they will pull down contract rates.

Removing fuel surcharges entirely from both indices, the pre-COVID spread was in a range of -$0.33 to -$0.50/mile. In other words, before the pandemic, it was $0.33 to $0.50/mile cheaper to move a truckload of freight in the spot market rather than by contract.

Today, that spread is -$0.86/mile. As long as this spread is so wide, shippers will continue to look to the spot market for capacity solutions and carriers will seek to replace any spot loads with contract rates, even if they have to bid contract rates at a cheaper rate than they have bid historically.

Eventually, this gap between spot and contract rates should converge within a historical range. This is RFP award season and shippers are going to place contracted freight with carriers that bid closer to the spot rates they are currently paying.

Truckload carriers should prepare for a brutal bid season. Shippers are going to claw back most of the contract rate gains they paid during the pandemic.

Truckload volumes match 2018 levels, a good year for trucking. But that isn’t a good thing.

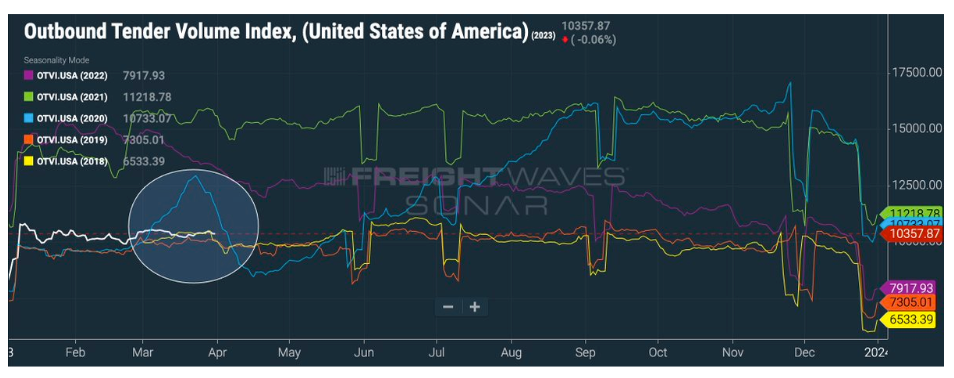

Trucking tender volumes are currently running at 2018 levels.

Tender volumes (OTVI.USA) track the number of truckloads electronically offered by shippers to carriers in the contract market. The white line in the chart below represents 2023, while the yellow line represents 2018. Orange represents 2019.

2018 was a good year for trucking, but with so much capacity added over the past five years, a reset to those levels is not cause for celebration.

According to the Federal Motor Carrier Safety Administration, the number of trucks in the for-hire market is up 29% since early 2018. It will take time to bleed off excess capacity.

No one really knows what direction the U.S. economy will head during the next three quarters of 2023, but there is plenty of reason to expect that the “Great Purge” in trucking will continue for the foreseeable future.

All of the data presented in this article are available on FreightWaves SONAR platform. Interested in learning more about how SONAR’s high-frequency supply chain data can give you an advantage over your competitors and help you to make informed decisions about freight pricing and capacity risk management?

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post • Chicago, IL Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now

gregory bonilla

GM Craig, great assessment on the freight market. Yes, you did post, and I’d read it as well, your article back last year about your prediction on upcoming freight recession. readers has pay attention to, even though they are out there in middle of battle field , doing loads. pay attention to the bottomline advices here , when you said, “Truckload carriers should prepare for a brutal bid season. Shippers are going to claw back most of the contract rate gains they paid during the pandemic.” Everything else is just details on top of details.

Rodolfo Bueno

En otras palabras nos espera mas de lo Mismo y llo pienzo que el govierno es el que desestabiliza el ritmo para hacer reacomodos ejemplo las pandemias fabricadas los subsidios alas farmaseuticas y de paso las energias renobables ect ect todas en favor de los enviroambientales

Kamil Witkowski

Hey Craig,

That is a great article and definitely a good analysis. As a smaller carrier owner things have been really rough on the spot market. Most smaller fleets rely on the spot market for 99% of their moves. Its hard to fight the market with almost a year of hardship and if not Diesel being up, its supply chain issues, this is why so many give up on owning fleets. Its hard to be steady and bring good work flow. No one can afford anything in life including plans for the future because the trucking industry is so unpredictable.

Alan M Przybyla

Great reporting. Spot on with your analysis.

David Eberle

Great analysis. So tough for trucking companies and in particular – small guys. I mean insurance costs – up; tires equipment – up, driver wages – way up – and now rates are way way down. Can’t make it. Drivers can go to OTR trucking companies or over to dedicated / private fleets. Those last jobs may be more stable. And they have better benefits. Carriers were making dollars on FSC – with low empty miles, but an over-supply of equipment and lower amount of loads – and dropping fuel prices – that avenue is coming up short as well. I am not sure where the bottom will go down too…. but I agree with the thought process on your end.

Pedue

Therefore, there is NO driver shortage.

Kevin Wills

I’d expect acquisitions of trucking companies and brokerages to be prevalent this year in order to gain market share.

Askar Aituov

Thank you for this analysis! It’s awesome!