Current financial news headlines are full of stories about inflation and the resurgence of inflation in the U.S. economy. At the macro level, signs that there has been a rebirth of some inflation are present. The yield on the 10-year U.S. Treasury has climbed from an ultra-low 2.1% to 2.9% in the last six months (a 38% increase in yield). The value of the U.S. Dollar as measured in terms of the world’s other major currencies has gone down by 15% in the last year, down by 7% in the last 3 months alone. Given the number of smart people investing in these markets, and the amount of money they are investing, it is risky to ignore what the ‘wisdom of crowds’ is trying to tell us. Sidebar – As we have discussed in previous articles, we continue to assert that the more people investing in, and the larger amounts being invested in, the more predictive a market becomes (i.e., wisdom of crowds)

Current transportation news headlines are also full of stories about rate increases that are at or near record high levels. According to the January Cass TL Linehaul Index, based on freight bills actually paid (a real-time reflection of price realized through spot and contract), the price paid for truckload services went up 6.3%. This followed the November and December Cass TL Linehaul Indexes which were up 6.3% and 6.2% respectively. This is an extraordinarily strong pricing indicator especially when two factors are taken into account:

- The Cass TL Linehaul Index is based on a large population of freight bills paid (>600,000) with a level of data granularity that allows the fuel surcharge to be eliminated (i.e., higher fuel prices are not driving the 6.3% increase, base pricing power is).

- There is a large shipper bias to the Cass data, since smaller shippers are less likely to have outsourced the freight bill payment function. Large shippers tend to have contracts in place for most freight movements and tend to have a smaller percentage of freight movements via spot rates (i.e., spot rates are so strong, that the underlying amount of increase in contract rate of 2% to 3% was overwhelmed by spot rates, the average was still drawn higher).

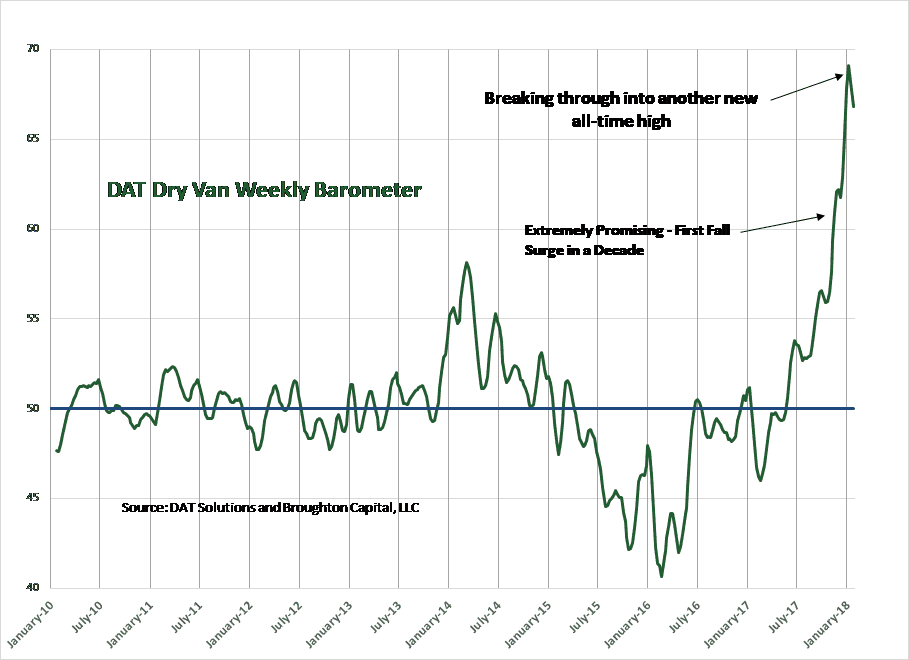

The DAT Trucking Barometers and pricing (both spot and contract) provide data that confirms the statistics provided by Cass. In all three modes (Dry Van, Reefer, and Flatbed), the Barometers are at all-time highs and spot pricing has surged above contract pricing. Especially since this is happening at what is normally a seasonally weak period for trucking freight (i.e., February is usually the weakest freight month of the year), we have a growing level of confidence that the contract rebidding season will be extraordinarily productive for truckers this year.

(Story continues below charts)

The January Cass Intermodal Index told a similar story of strong pricing (up 5.0% YOY) hitting an all-time high of 141.4, and dragging the three-month moving average up to 4.3%. With demand and pricing continuing to remain strong in truckload and the price of diesel above $3 a gallon, we expect this strength to continue.

Will this pricing strength last? The current trends in transportation are showing signs of real inflation. We expect improved operating profit margins in trucking, followed by outsized top line and bottom line growth. That said, just as has been true in previous cycles, the industry will eventually add enough capacity to kill its own pricing power, but for the foreseeable future we expect truckers to have an extraordinary level of pricing leverage. Qualified drivers continue to be in short supply and ELD’s are making capacity tighter and qualified drivers more expensive. Demand drivers are strong, getting stronger, and appear poised to stay strong for the foreseeable future. Until the industry figures out how to grow capacity faster than demand is growing capacity will stay tight and pricing will stay strong. Stay tuned…