Oatly (Swedish oat milk company) shares continue to struggle. Oatly’s American depository receipts declined 21% Monday and closed at $9.36, down 45% from the $17 IPO price. Investors’ primary concern centered around a slowing revenue growth rate; the company now expects revenue this year to be “more than $635 million,” which is 8% below the earlier guidance of $690 million and implies 4% quarter-over-quarter revenue growth in the 4Q21. Despite the revenue shortfall for the year relative to previous expectations, Oatly’s revenue continues to grow very fast; its third quarter revenue grew 49% y/y and its revenue grew 55% for the first nine months of 2021.

Slowing sales of plant-based food alternatives was a trend also evident last week in the results of both Beyond Meat as well as the plant-protein segment of Maple Leaf Foods. The difference between Oatly and those two plant-based meat companies is that Oatly’s guidance cut appeared to be primarily driven by supply chain constraints that limited product availability rather than a demand slowdown. I believe the company makes a strong case that oat milk is an expanding product category that is clearly taking share from soy milk and almond milk, the dominant milk alternative in the U.S. In addition, with plant-based daily alternatives having only a market share of 9%-11% in the company’s key Western markets, there is plenty of room for category growth.

Like most other CPG companies, Oatly’s cost are rising sharply — the company expects its cost of goods sold to increase 5%-6% next year. As Oatly continues to expand production and boost its advertising spend, its losses continue to increase — the company’s net loss for the first nine months of 2021 was $132.6 million versus a net loss of $23.4 million in the first nine months of 2020. But, for now, the company’s losses appear to be part of its strategy since scaling up production capacity, increasing market penetration and growing revenue are the company’s primary objectives currently.

It’s a good time to be one of the major meat processors. The major meat processors’ profit margins have been expanding and Tyson’s fiscal 4Q was no exception. On Monday, Tyson reported its fiscal 4Q adjusted earnings per share were up 35% y/y on 11.8% y/y revenue growth and a sharp increase in operating margin from 8.4% to 14.9%.

What stood out to me was that the company’s 11.8% y/y revenue growth in its fiscal fourth quarter came on a 10.7% volume decline and a massive 22.5% average price increase. Pork and beef prices had the steepest average price increases of 38% and 32.7%, respectively. Those same segments (beef and pork) also had the steepest volume declines of 17.7% and 15.4%, respectively. Looking ahead to fiscal 2022, Tyson expects its volume to grow by 2%-3% from 2021, which should outpace the overall meat industry, with the largest source of that growth coming from its chicken segment, which has been constrained much of this year.

I expect the Biden administration to use Tyson’s latest results to support its argument that the meat processing industry is too highly concentrated to be truly competitive. Lately the administration seems to be looking for ways to deflect blame for the surging inflation rates, which are at multi-decade highs, and meat prices are the largest component of overall grocery inflation.

As reported by Just Food, Kellogg has filed a lawsuit against striking workers, alleging that its working staff has been intimidated by employees on the picket line. Last week, talks between Kellogg and the striking BCTGM (Bakery, Confectionary, Tobacco Workers and Grain Millers’ International Union) broke down after the union rejected the company’s “last, best and final offer.” Kellogg said that no further negotiations are scheduled. It sounds like we will continue to see picket signs that satirize Tony the Tiger.

The truckload spot market has been eerily calm prior to the traditional peak season. Truckload spot rates have been slowly declining (in the 1%-4% range) since Labor Day for dry van, refrigerated and flatbed loads. Following the renegotiation of contract rates to significantly higher levels, carriers have been more compliant. As a result, there have been fewer loads falling through routing guides onto the spot market and spot rates have fallen some. Nevertheless, shippers should keep in mind that spot rates rose sharply leading up to each of the holidays earlier this year and should expect additional spot rate spikes in the days leading up to Thanksgiving and Christmas.

FreightWaves explains why air cargo is a relative bargain. In short, for all the reduced transcontinental flights, the capacity crunch in air cargo has been less severe than the capacity crunch on the ocean. Pre-pandemic, the average price to move air cargo was 13-15x higher than ocean, but now it is only 3x-5x higher.

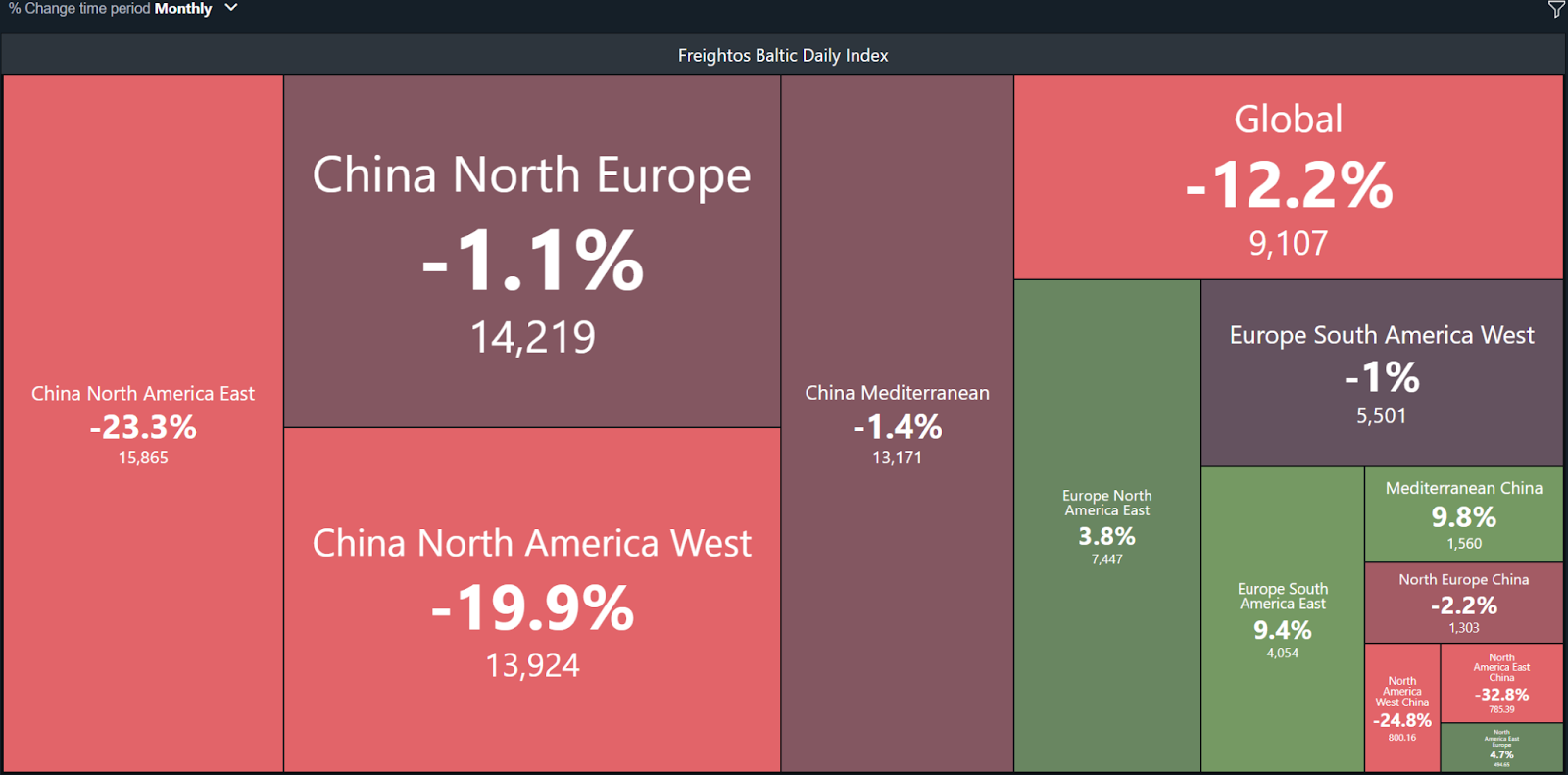

While the Freightos Baltic Daily Index shows that daily ocean rates are ~20% lower month-over-month from China to North America, they remain sharply higher year-over-year, leading to a narrower rate spread compared to air cargo.

To sign up for The Stockout, a free newsletter focused on CPG supply chains, please click here.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now