TreeHouse Foods gains share despite lingering supply chain issues

TreeHouse manufactures food products for retailers’ private label brands, such as those owned by Walmart, Aldi and Trader Joe’s. I like to look at TreeHouse’s results each quarter to gauge share changes between the national brand and private label.

According to TreeHouse and leveraging IRI’s point-of-sale report, the national brands that compete in its categories posted a 5.0% unit volume decline in the fourth quarter versus a 0.1% increase in private label unit volume. The company’s own brands outperformed its private label peers by posting a 3.4% y/y increase in unit volume in the third quarter.

It’s not surprising that private label food brands are taking share, but the company’s 3.4% unit volume increase came on massive 24.6% average price increases versus the year-ago period. What also stood out was the company would have gained more share if not for the lingering supply chain constraints, including ongoing labor and material availability issues, that are impacting about half of its segments. Management described those issues as costing them a point or two in volume in half the company’s segments and expects those problems to be fully resolved by the end of the year.

TreeHouse’s management also added its 2 cents’ worth to the consumer packaged goods topic of the hour — whether retail prices will start falling amid lower commodity prices. According to management, only about half of its inputs are reflected in the visible prices of commodities that have come down of late, which, they add, still remain at historically high prices. The company’s non-tradeable input costs, such as packaging, remain inflationary, largely offsetting the impact of falling commodity prices. As a result, the company still plans to raise prices but intends to be “more surgical in nature.” That is similar to the recent comment from Unilever’s outgoing CEO who said we are likely past peak inflation but not past peak prices.

Kroger-Albertsons looking for buyers of 250-300 store locations

The potential divestiture of 250-300 locations would be toward the high end of the 100-375 range of locations that Kroger anticipated at the time of the merger. The divestiture ceiling for the consolidation is 650 stores.

According to reports, the divested grocery locations could get folded into Stop & Shop, Giant Food, Food Lion and Hannaford supermarkets. Metro areas with overlapping Kroger and Albertsons stores include the Pacific Northwest, Southern California, Phoenix and Chicago.

The companies have said they expect the transaction to close in early 2024, but a number of equity analysts believe the deal could take an additional year in light of the regulatory process, which includes necessary approval from the Federal Trade Commission. In early December, Kroger received a second request for information from the FTC, suggesting the potentially anticompetitive aspects of the deal are being looked at closely.

From CPG companies’ perspective, the negative implications of this deal are clear. For many, it will increase their customer concentration, creating a second customer that represents more than 10% of revenue (CPGs often disclose Walmart as their largest customer, representing about 20% of sales). The other concern for CPGs is the possibility that the combined grocery giant will use the deal as a launching point for expanding their private label penetration. Kroger’s management has said it and Albertsons have largely non-overlapping private label strengths.

Potential positives of the merger from the CPGs’ perspective include the potential for them to leverage the enhanced retail data that the combined grocer will have on over 100 households — or most that shop at traditional grocers. In addition, CPGs may see increased efficiencies in the logistics of dealing with a smaller number of large grocers.

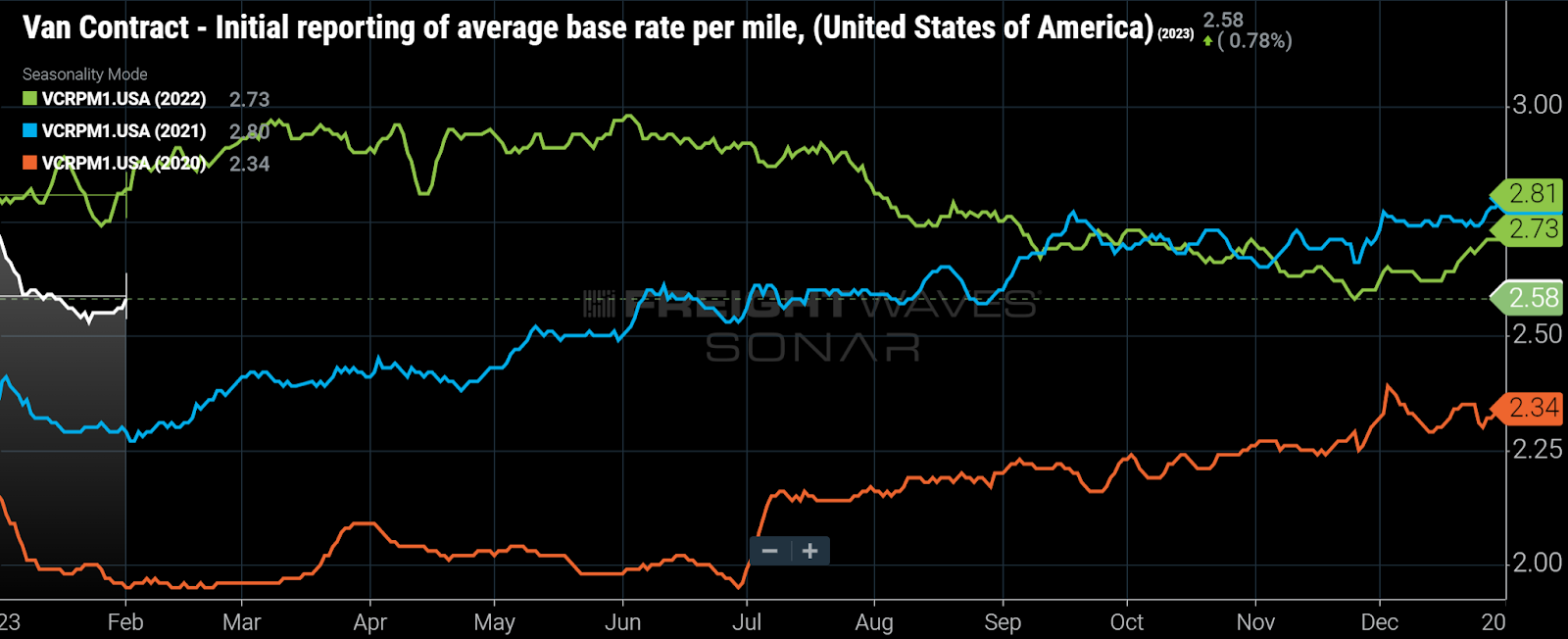

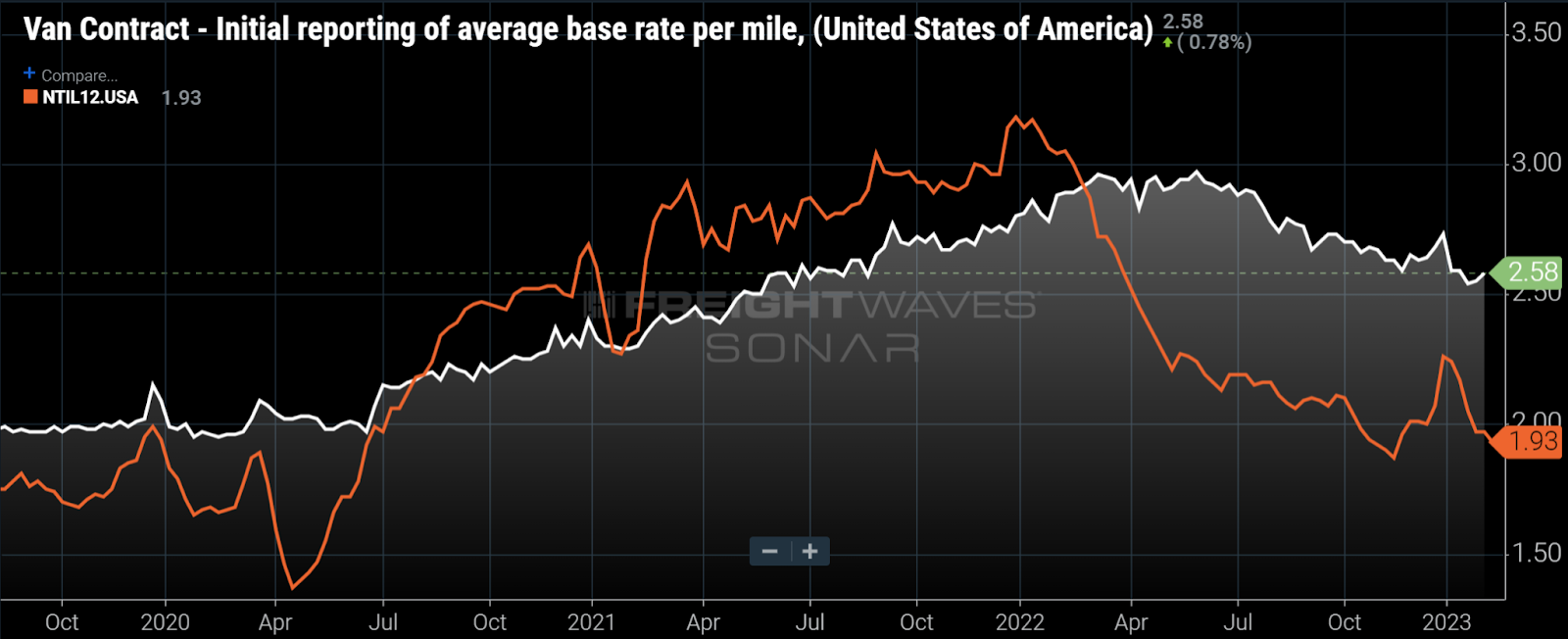

Contract freight rates fall with further declines likely

Shippers that heavily use dry van truckload should monitor the above national chart, as well as the lane-by-lane breakdowns available in FreightWaves SONAR via the Market Dashboard and Supply Chain Intelligence apps. The chart above shows the average dry van linehaul contract rate (excluding fuel) is down 7.8% year to date through the end of January, compared to the year earlier. Currently, the average rate is at its lowest level since August 2021.

Meanwhile, comparing average dry van contract rates to average spot rates shows that contract rates are about $0.65 per mile above spot rates when fuel is treated similarly (i.e., the spot rate index is adjusted to remove the impact of fuel, using $1.20 per mile as a baseline). That comparison, as well as a currently depressed dry van national tender rejection rate of 3.24%, suggests contract rates have further to fall in the near term.

To subscribe to The Stockout, FreightWaves’ CPG supply chain newsletter, click here.

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

Future of Rail Symposium

Reshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post • Chicago, IL Register NowReshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

The Signal at Chattanooga Choo Choo • Chattanooga TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now