Before getting into CPG news, here are two near-term events for your calendar:

On Friday, The Stockout show is focused on the railroad industry and features a true industry expert (not referring to myself). I will be interviewing Tony Hatch, an independent railroad consultant and longtime senior transportation analyst on Wall Street. He is fresh from hosting his annual RailTrends conference, which I consider to be the premier railroad industry conference.

I am excited to hear his thoughts on the CP-KCS merger, the potential changes to railroad regulation amid a larger and more aggressive Surface Transportation Board, the activist investor pressure on Canadian railway CN, the potential for intermodal volume growth, and the industry’s outlook as it balances delivering near-term results and longer-term growth.

I invite you to watch live on Friday at 3 p.m. ET at tv.www.freightwaves.com. A replay will be uploaded to FreightWaves.com and podcasting services shortly thereafter.

On Monday, at 2 p.m. ET, I host the next quarterly The Stockout webinar. Here’s the link to register. In addition to a rundown of the latest CPG industry themes, I’ll provide a data-driven outlook on various transportation modes (dry van and reefer truckload, intermodal, ocean/air). I will be joined by Jason Meklir, VP of enterprise sales at Flock Freight, who will describe how CPG companies can improve the efficiency of their transportation spend. I encourage webinar participants to ask questions so we can have a lively discussion like we had in last quarter’s webinar.

Kellogg and bakery union reach tentative agreement. Kellogg Co. and The Bakery, Confectionary, Tobacco Workers and Grain Millers International Union (BCTGM) reached a tentative agreement on a five-year labor agreement covering 1,400 employees. BCTGM members went on strike on Oct. 5 at four Kellogg cereal locations. The company and union were in disagreement over placing workers in a two-tiered system that differentiated between longtime “legacy” workers and “transitional” workers who have less tenure and represent about 30% of its workforce.

If the agreement is ratified, in addition to a raise, all employees with at least four years of service will qualify for legacy wages and benefits. In response to the work stoppage, Kellogg had deployed management employees to temporarily fill some positions, hired permanent replacements and also imported cereal produced in its international facilities.

Nine companies, including a few major CPG companies and grocers, received an order from the Federal Trade Commission to turn over supply chain data. The companies are Amazon, Associated Wholesale Grocers, C&S Wholesale Grocers, Kraft Heinz, Kroger, McLane, Procter & Gamble, Tyson Foods and Walmart. It’s not surprising to me that Tyson was among the companies ordered to turn over documents, since the Biden administration has been blaming the company for inflation in meat prices. Those companies have 45 days to respond with documents related to their supply chain strategies, pricing and suppliers. The stated purpose of the order was for the FTC to understand the causes behind this year’s supply chain disruptions, but the skeptic in me believes the administration is looking for ammunition to blame inflation on large corporations.

The coffee price surge could be long-lasting, according to a CNBC article. Prices could remain elevated after hitting a recent 10-year high and up 85% year-over-year. Poor growing conditions in Brazil, political instability in Ethiopia and rising COVID cases in Vietnam are all contributing to the highest prices since coffee exceeded $3 a pound in 2011. On recent analyst calls when the J.M. Smucker Co. discussed rising coffee prices, the owner of the Folgers brand was confident it could pass on coffee cost increases to consumers, citing a lack of elasticity in the category. That makes sense to me. I doubt I will cut back on coffee just because prices are 85% higher than last year — if they were up 850% I might.

Consumer product website Thingtesting.com highlights large CPG companies that are using sales techniques more commonly associated with their startup competitors. Large CPG companies are launching and acquiring stylish brands, using more direct-to-consumer marketing and even designing products with YouTube unboxing videos in mind. The large CPG companies’ objective is to maintain market share amid an onslaught of younger and cooler brands. In many cases, the large CPG companies are going out of their way to avoid highlighting their ownership of the newly established brands.

Subscription boxes are being used more heavily for testing new products and rewarding ardent fans. This Food Dive article highlights how a popcorn company tested products through subscription boxes while Coca-Cola has an insiders club where consumers can pay to receive new and limited-edition products before they are available to the public.

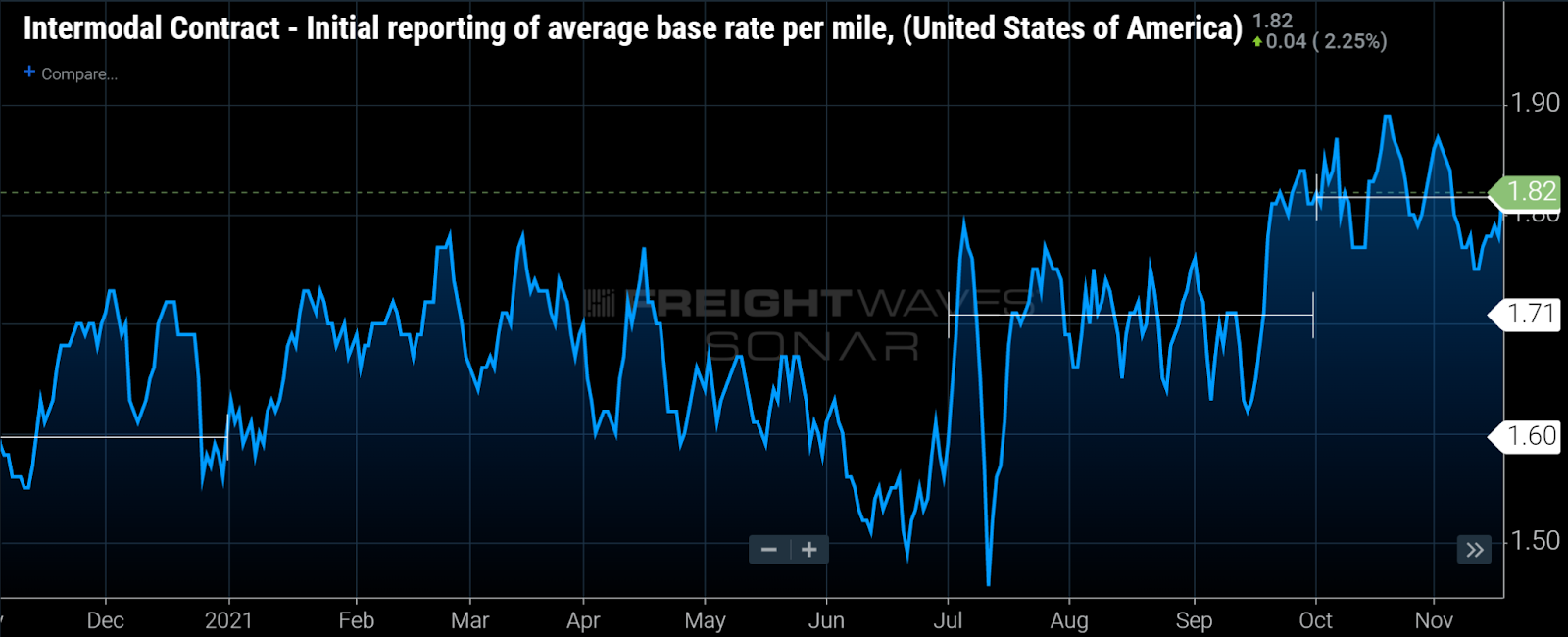

Finally, here’s a SONAR chart that I find interesting. Intermodal contract rates took another 6% step up quarter-over-quarter to an average base rate (i.e., does not include fuel surcharges) of $1.82 a mile so far in the fourth quarter of 2021 (recognizing that there is nearly one month remaining) from $1.71 a mile in the third quarter 2021. Relative to the fourth quarter of 2020, SONAR intermodal contract rates are 14% higher, reflecting the double-digit rate increases in intermodal contract rates that took hold as they were repriced earlier this year.

To sign up for The Stockout, a free newsletter focused on CPG supply chains, please click here.

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

Future of Rail Symposium

Reshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post • Chicago, IL Register NowReshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

The Signal at Chattanooga Choo Choo • Chattanooga TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now