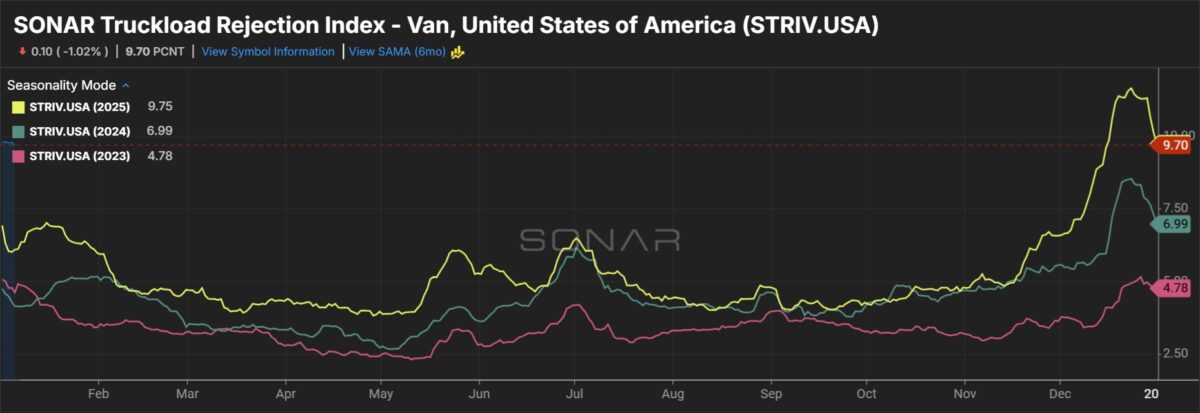

Transportation capacity plummeted in December while rates continued to rise, according to a monthly survey of supply chain managers. The drop in available capacity appears more pronounced than in prior holiday shopping seasons.

The Logistics Managers’ Index – a diffusion index in which a reading above 50 indicates expansion while one below 50 signals contraction – displayed a reading of 36.9 for transportation capacity in December. That was 13.1 percentage points below November and the lowest level recorded since October 2021. It was also the first contraction in the capacity dataset since March 2022 – the onset of the freight recession.

The Tuesday report acknowledged the impact English-language crackdowns have had, but said “the proliferation of holiday season deliveries” likely had a larger impact on capacity in December.

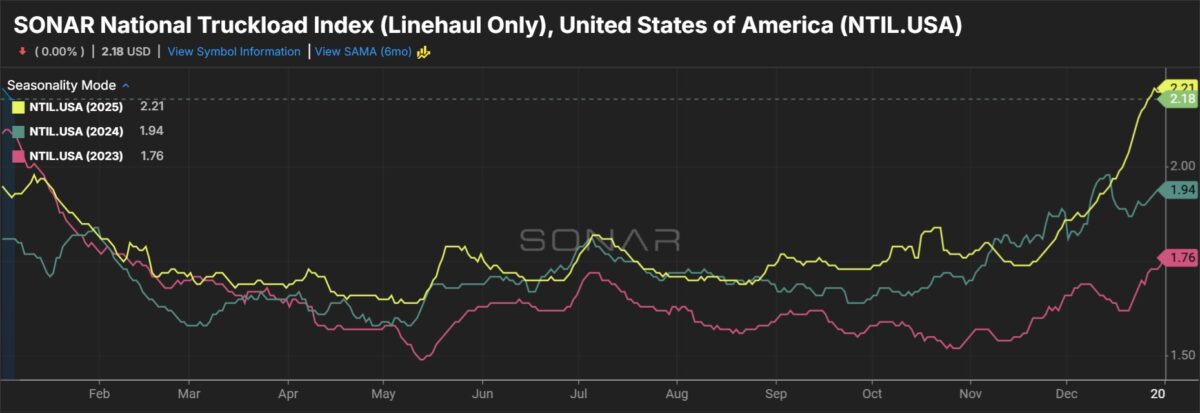

Transportation utilization (58.2) was up 6.7 points in the month. Transportation pricing (66.7) was up 1.8 points to the highest level since January 2025 (70.4).

Transportation utilization slightly contracted at downstream companies (retailers) to 47.6 but expanded upstream at manufacturers and wholesalers to 62.1.

“This is likely due to retailers having largely replenished their holiday inventories from October to early December and then more or less ‘standing pat’ (with an exception for last-mile delivery),” the report said.

Transportation pricing was nearly 30 points higher than capacity, “suggesting that December’s freight market was the strongest in over three years.”

The one-year-forward forecasts for capacity, utilization and pricing are 40.5, 70.3 and 76.8, respectively, which would represent “a significant shift in transportation markets.”

“The key to this prediction will be consumer demand holding steady despite potential price increases,” the report said. “Consumer demand was stronger than anticipated throughout 2025, so there is a chance that this – and the associate turnaround in the freight market – could prove to be true.”

Inventories see record drop

The overall LMI stood at 54.2 in December, 1.4 points lower than in November and the lowest reading since April 2024. The LMI has been below the all-time average of 61.4 for 10 straight months. However, a steep drop in inventories and tougher comparisons after two full years of expansion were the catalysts behind the slowdown.

Inventory levels (35.1) entered “extreme contraction” in the month, down 17.4 points from November and 14.9 points lower than December 2024. The declines were more pronounced in the first 18 days of the month (28.2) than in the last two weeks (42.9).

Inventory costs (62.9) remained inflationary, but at a pace that was 8.1 points slower than in November. Inventory cost growth accelerated from the first half of the month, jumping 17.1 points during the last two weeks as final-mile delivery options were more widely employed. The report also said inventory costs were up throughout 2025 due to tariffs.

The one-year-forward forecast for inventories is inflationary at 59, with inventory costs expected to continue to rise faster at 72.1.

Downstream retailers are planning to keep inventories flat, registering a forward outlook of 50, as they try to “improve cashflow and avoid tariff-related costs for as long as possible.” Upstream wholesalers expect expansion in merchandise levels (63), however, may look to more quickly push inventories downstream if higher holding costs persist. (The report noted that some small upstream firms have taken on high-interest loans and may not have the ability to hold inventories as long as they have in the past.)

“Overall, we view the report as a positive for freight fundamentals given the spot rate strength appears supported by solid demand during peak season in December,” said Brian Ossenbeck, JP Morgan (NYSE: JPM) analyst, in a Tuesday note to clients. He said the massive inventory drawdown by both upstream and downstream companies, indicates “both segments expect to rebuild inventories over the next 12 months from historically lean starting points.”

He noted that past inflections in the LMI inventory data have signaled future re-stocking and de-stocking cycles.

Warehousing prices rise even as utilization sags

Lower inventories weighed on warehousing metrics in the month.

Warehousing capacity (61.2) increased 6.4 points from November as warehouse utilization (42.9) fell 4.7 points to a new low for the nine-year-old dataset.

“The softness in the warehousing market is due to a combination of retailers and wholesalers emptying out inventory backlogs as well as the ongoing slowdown in manufacturing,” the report said.

Warehouse prices (66.2) remained inflationary, up 3.3 points in the month.

“Warehousing Price is the one metric that has never contracted in the history of the LMI. Whether inventories are up or down, the cost of storing them continues to grow.”

Respondents pegged warehouse prices to stay on the rise over the next 12 months, returning a 74.7 forward outlook.

The LMI is a collaboration among Arizona State University, Colorado State University, Florida Atlantic University, Rutgers University and the University of Nevada, Reno, conducted in conjunction with the Council of Supply Chain Management Professionals.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now